আরও দেখুন

14.05.2025 12:18 AM

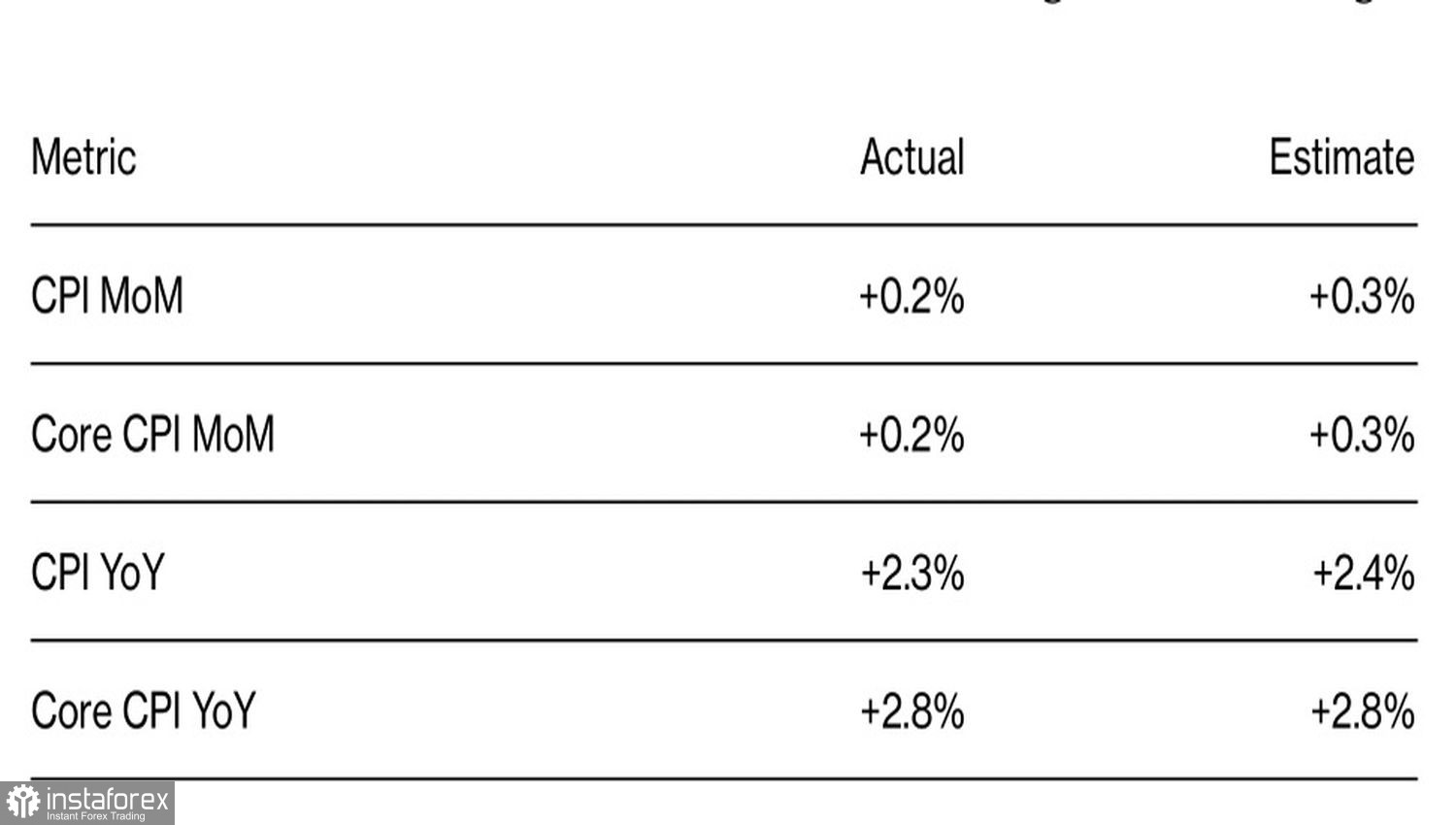

14.05.2025 12:18 AMMan proposes, God disposes. After the White House imposed strict tariffs on America's Independence Day, there was much discussion about rising inflation and a slowing U.S. economy. However, instead of that, April's consumer prices rose a modest 0.2% month-over-month and 2.3% year-over-year. Both figures fell short of forecasts, and their downward trajectory pushes the Federal Reserve toward cutting the federal funds rate, especially given that the labor market remains strong.

In his way, Donald Trump is right. When everything falls—from oil and gasoline prices to CPI and Treasury yields—the central bank should consider restarting the monetary easing cycle. Yet the Federal Reserve remains silent, counting on inflation to eventually pick up on its own. Tariffs are too high. Even the significant tariff reduction against China only brought the average rate down to 12%, compared to 2.4% back in 2024.

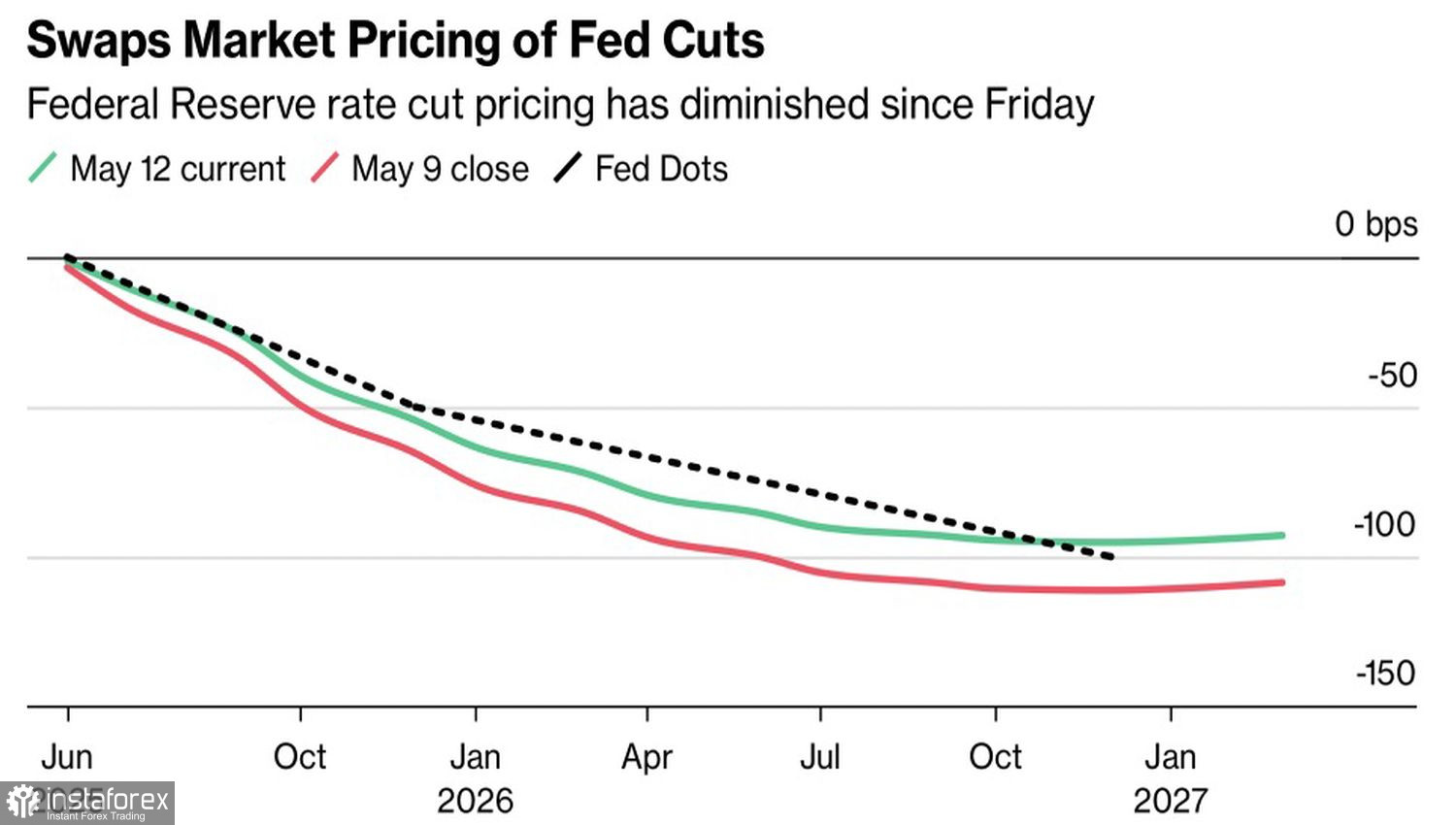

The Fed should act preemptively, but haste makes waste. The worst-case scenario for the central bank is cutting the federal funds rate only to see inflation spiral out of control. Unsurprisingly, the futures market has pushed back expectations of renewed monetary easing from July to September. Derivatives now price in a 56 basis-point cut, down from 75 bps before the U.S.–China trade deal.

Interestingly, the projected rate cuts for the European Central Bank were revised downward following the 90-day postponement of mutual tariffs between Washington and Beijing. Investors now anticipate a 50-bps deposit rate cut instead of 60 bps.

The situation could change if the U.S. begins trade negotiations with the European Union. Donald Trump has called Europe "worse than China," claiming it treated the United States very unfairly. Now, the White House holds all the cards to punish the EU for such behavior. Brussels, in turn, has prepared a €95 billion retaliation package should the talks fail.

One of the most dangerous scenarios for the U.S. may be coordinated actions between Europe and China. However, as the saying goes, "charity begins at home." Beijing achieved its goal of lessening its constraints and is unlikely to step up for Brussels, especially since its earlier calls for joint action with the EU went unanswered. In other words, "Sort out your own problems."

The euro now hopes the market euphoria over the U.S.–China trade de-escalation has run its course. The good news has already been priced into U.S. stock indices and the dollar, and we'll see if that's the case.

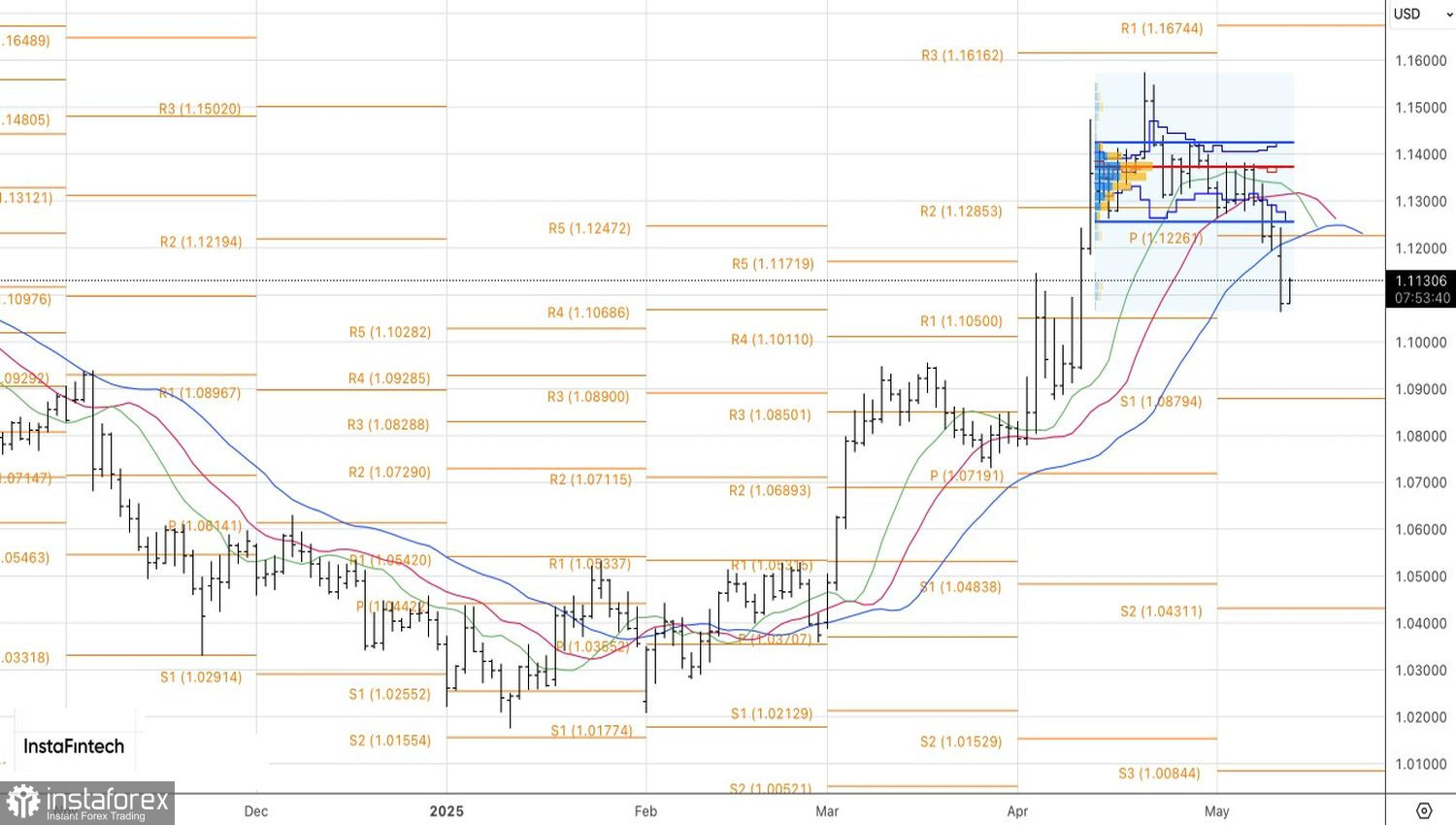

Technically, on the daily chart of EUR/USD, there's a counterattack from the bulls following their rout the previous day. Buyers are finding the strength to push the major currency pair higher. However, as long as it trades below the pivot level of 1.123, the mood remains bearish. This keeps the door open for periodically adding to shorts initiated from 1.128.