আরও দেখুন

15.07.2025 12:48 AM

15.07.2025 12:48 AM

Last Friday, the U.S. Treasury Department announced the first budget surplus since 2017. Many in the market may have interpreted this as great news for the dollar, but I see little reason for optimism. The first budget surplus in eight years, in my opinion, is hardly cause for celebration. Indeed, revenue from import tariffs played a role. Revenues increased, but what other economic changes can we point to?

The U.S. trade balance remains in deficit despite tariffs and duties. Imports to the U.S. fell by 70 billion dollars in April–May, or about 20%. This is clearly a temporary phenomenon — imports will recover, though they are unlikely to return to pre-Trump or pre–trade war levels. The drop in imports is mainly due to the president's tariffs, while exports should, in theory, grow due to the weaker dollar. But in practice, the changes may be marginal.

Let me remind you that many consumers around the world are deliberately avoiding U.S. products because of Donald Trump's policies. Governments across the globe are facing unfair tariffs, which hardly encourage them to cooperate with Washington. Even if governments don't directly obstruct U.S. exports, consumers can't be forced to buy American goods if they don't want to. In my view, achieving a positive trade balance will be extremely difficult, even with tariffs.

At the same time, the U.S. national debt continues to rise and has reached a staggering $36 trillion. In June alone, the U.S. government spent $84 billion to service the debt. The vast majority of economists expect this debt to continue growing, and as confidence in the U.S. government declines and the country's credit rating is downgraded, Treasury yields will continue to rise. This, in turn, means higher debt servicing costs.

Additionally, Trump's "One Big Beautiful Law" calls for increased spending on defense and immigration enforcement. The U.S. budget has posted a surplus just once in 96 months, while national debt keeps growing, and expenditures are expected to rise. No trade deals are being signed, and Trump continues to raise tariffs, which will further reduce U.S. imports.

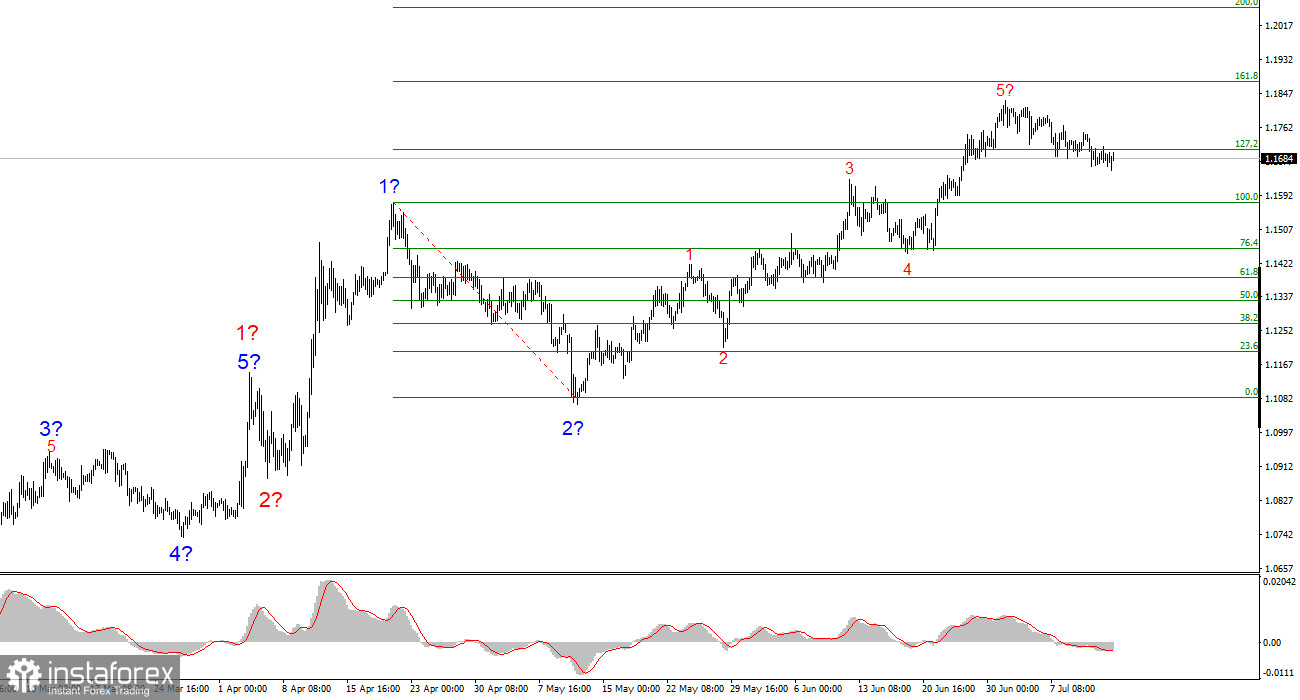

Based on my analysis, EUR/USD continues building a bullish trend leg. The wave structure remains entirely dependent on the news background, particularly Trump's decisions and U.S. foreign policy, and there has been no positive shift. The trend leg may extend up to the 1.25 area. Therefore, I continue to consider buying with targets near 1.1875, which corresponds to the 161.8% Fibonacci level, and potentially higher. In the short term, a corrective wave set is expected to form, so I plan to enter new long positions after that correction is complete.

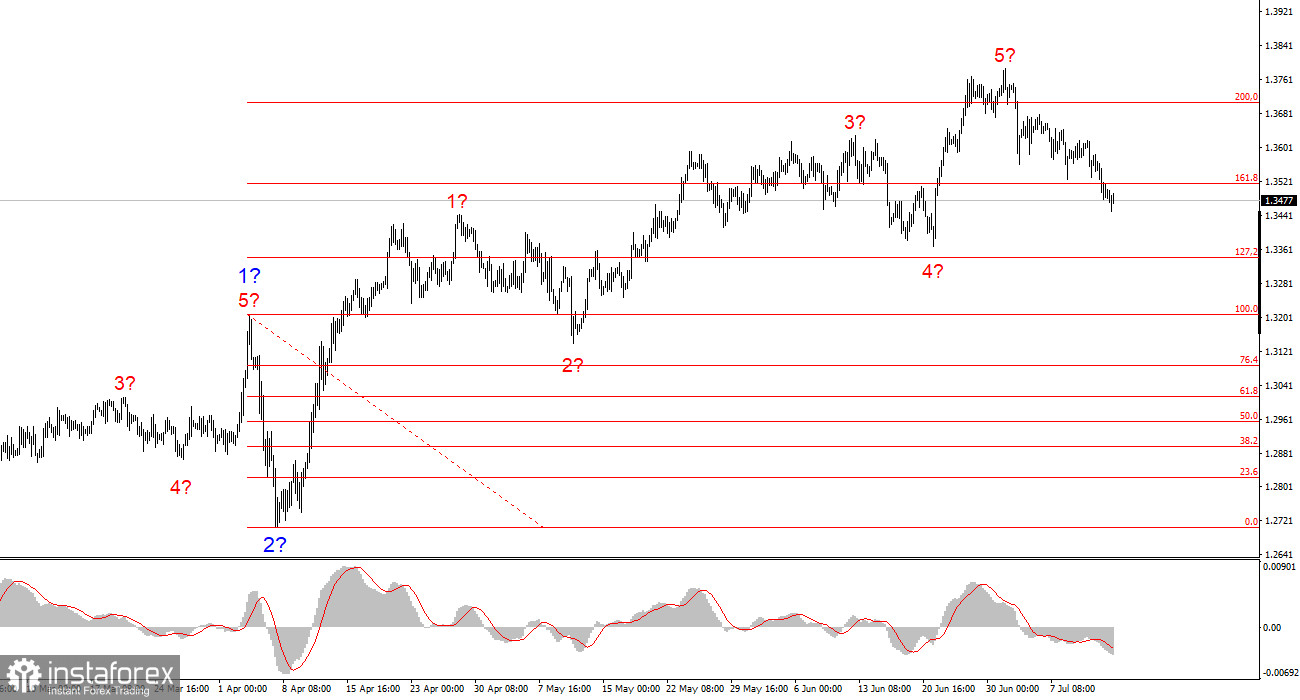

The wave structure for GBP/USD remains unchanged. We are dealing with a bullish impulse wave leg. With Donald Trump in office, the markets could still face a large number of shocks and reversals that may significantly impact wave structures — but for now, the main scenario remains intact. The targets for the upward leg are currently located around 1.4017, which corresponds to the 261.8% Fibonacci level of the presumed global wave 2. A corrective wave set has already started to form. By classic wave theory, it should consist of three waves.