আরও দেখুন

13.05.2026 11:33 AM

13.05.2026 11:33 AMSince the previous report, there have been no significant domestic events in New Zealand that could materially affect the market. The Reserve Bank of New Zealand (RBNZ) published its Financial Stability Report and commented on the likely path of future inflation. However, neither event had a noticeable impact on market sentiment.

Prices for dairy products, one of New Zealand's key export items, so far show no signs of rising. The market treats the threat of a food crisis following an energy shock (due to the expected decline in global fertilizer production) as hypothetical. At present, this does not have a material effect on prices.

ANZ believes that the war in the Middle East had virtually no impact on New Zealand's economy in Q1, so the quarterly GDP data could even beat expectations — a positive factor supporting the kiwi at the moment. At the same time, GDP forecasts for Q2 and Q3 have been reduced by 0.5% as private consumption, investment and services exports are expected to decline. Accordingly, annual GDP is now expected to be 1.7% rather than 2.1%. Note that this does not yet imply a recession.

The next RBNZ meeting is on May 26; the market currently prices in roughly a 30% probability of a rate hike. Accordingly, there is upside potential for the kiwi if the market raises the likelihood of that event.

This week will bring more information: April PMI indices will be released and will show how New Zealand's economy is adjusting to geopolitical changes. Forecasts are negative; most commentators expect a slowdown in economic activity and in price growth. Inflation forecasts are currently sharply negative — in April the RBNZ identified three indicators it watches to assess medium-term inflationary forces: wage inflation, core inflation and medium- to long-term inflation expectations. In Q1, these indicators did not look threatening and were close to forecast; for Q2, the RBNZ raised expectations from 2.37% to 2.53%, which is still moderate, but risks are clearly shifting toward higher values.

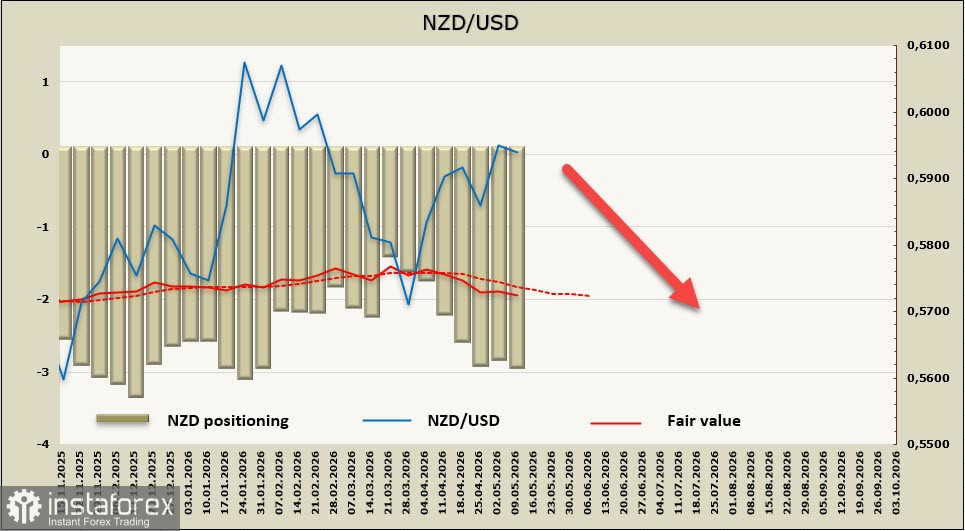

The net short position on the New Zealand dollar (NZD) increased by USD 114 million in the reporting week, reaching -USD 2.84 billion. This is a significant bias against the kiwi. Short positions have been rising for seven consecutive weeks despite NZD/USD having strengthened amid hopes for a resolution of the conflict in the Middle East. Long-term investors appear to be positioning for a more pessimistic scenario. The implied price remains below the long-term average.

Markets are starting to realize that a quick resolution of the current situation is unlikely and that the crisis will develop further. We believe a local peak at 0.5986 has already been formed. Bearish positions are strengthening, and they will look for an opportunity to break below the nearest resistance level at 0.5913.

We expect NZD/USD to fall below that level, which would change the medium-term technical picture to bearish. The next downside target is the 0.5860–0.5880 range.

The recent rise in the kiwi back to pre-conflict levels has been driven mainly by a weaker US dollar and improved global risk appetite, reflected in gains in US stock indices, rather than by local New Zealand factors. In case of renewed escalation in geopolitical tensions, the New Zealand dollar would be vulnerable, coming under significant pressure.