See also

31.07.2025 01:21 PM

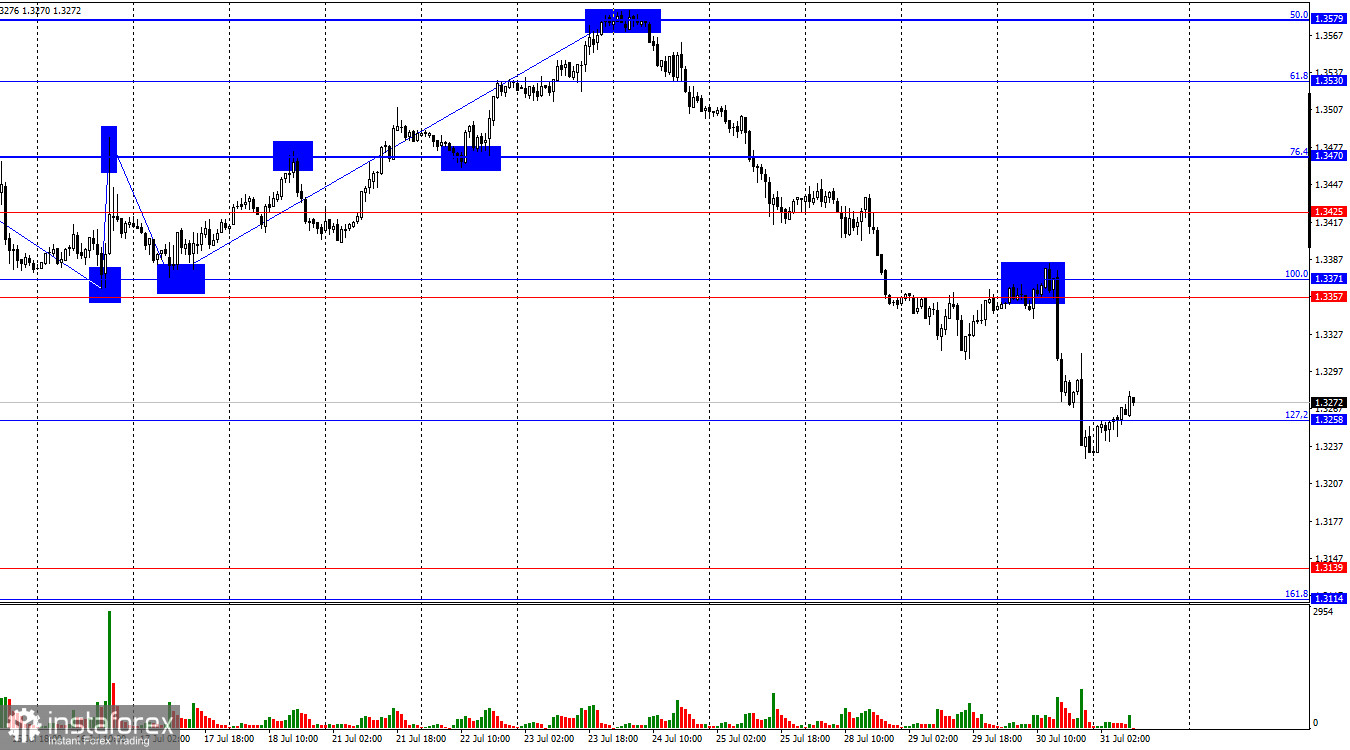

31.07.2025 01:21 PMOn the hourly chart, GBP/USD rebounded on Wednesday from the resistance zone of 1.3357–1.3371, reversed in favor of the U.S. dollar, and fell below the 127.2% Fibonacci retracement level at 1.3258. A new consolidation below this level today would allow traders to anticipate a further decline toward the next support zone at 1.3114–1.3139. If the pair consolidates above 1.3258, we could expect a slight recovery of the British pound toward 1.3357.

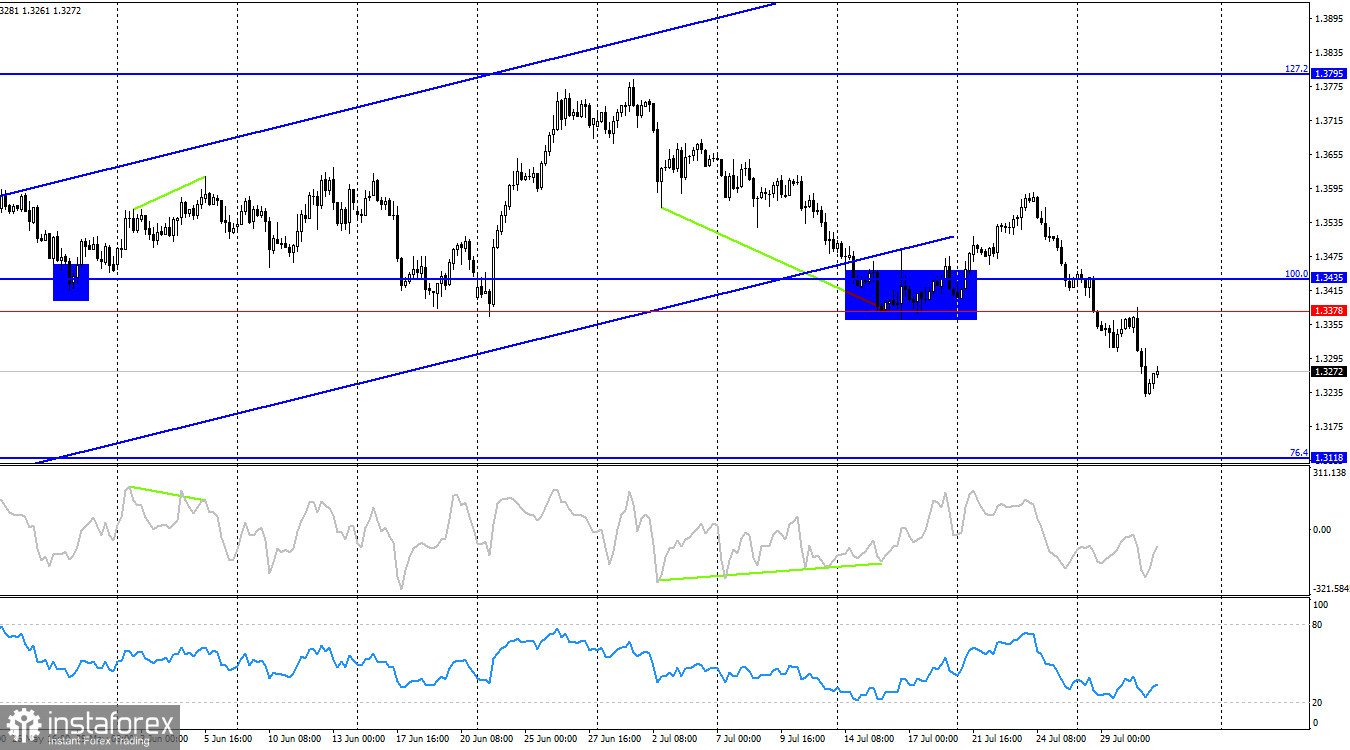

The wave structure briefly shifted in favor of the bulls but quickly reversed. The latest upward wave broke above the peaks of the two previous waves, but the most recent downward wave has now broken all previous lows. Thus, the trend can once again be considered "bearish." However, the information background has played a major role in supporting the bears. If sentiment shifts against them in the near term, we could see an equally strong upward wave, and the trend may once again turn "bullish." The situation remains ambiguous and largely depends on this week's news flow.

On Wednesday, the news backdrop was ideal for the dollar. First, disappointing reports from the eurozone weighed on the euro. Then, U.S. GDP data surprised to the upside, supporting the greenback. In the evening, Jerome Powell signaled that traders should not count on two rate cuts this year. Thus, the dollar has been supported by a consistent stream of positive news since the beginning of the week. Earlier in the week, the U.S. and EU signed a trade agreement that most experts described as highly favorable to the U.S. and burdensome for Europe. Additionally, President Trump has continued ramping up tariffs this week, raising duties on imports from India and, more recently, on goods from Brazil and South Korea. With August 1 approaching, tariffs are expected to rise further, affecting imports of copper, pharmaceuticals, and semiconductors. Trump continues to reshape global trade to serve U.S. interests.

On the 4-hour chart, the pair has completed another reversal in favor of the dollar and is generally continuing its downward movement. A consolidation below the 1.3378–1.3435 support zone opens the way toward the next 76.4% Fibonacci retracement level at 1.3118. No emerging divergences are currently observed on any indicators. A consolidation above the 1.3378–1.3435 zone would shift the trading bias back upward.

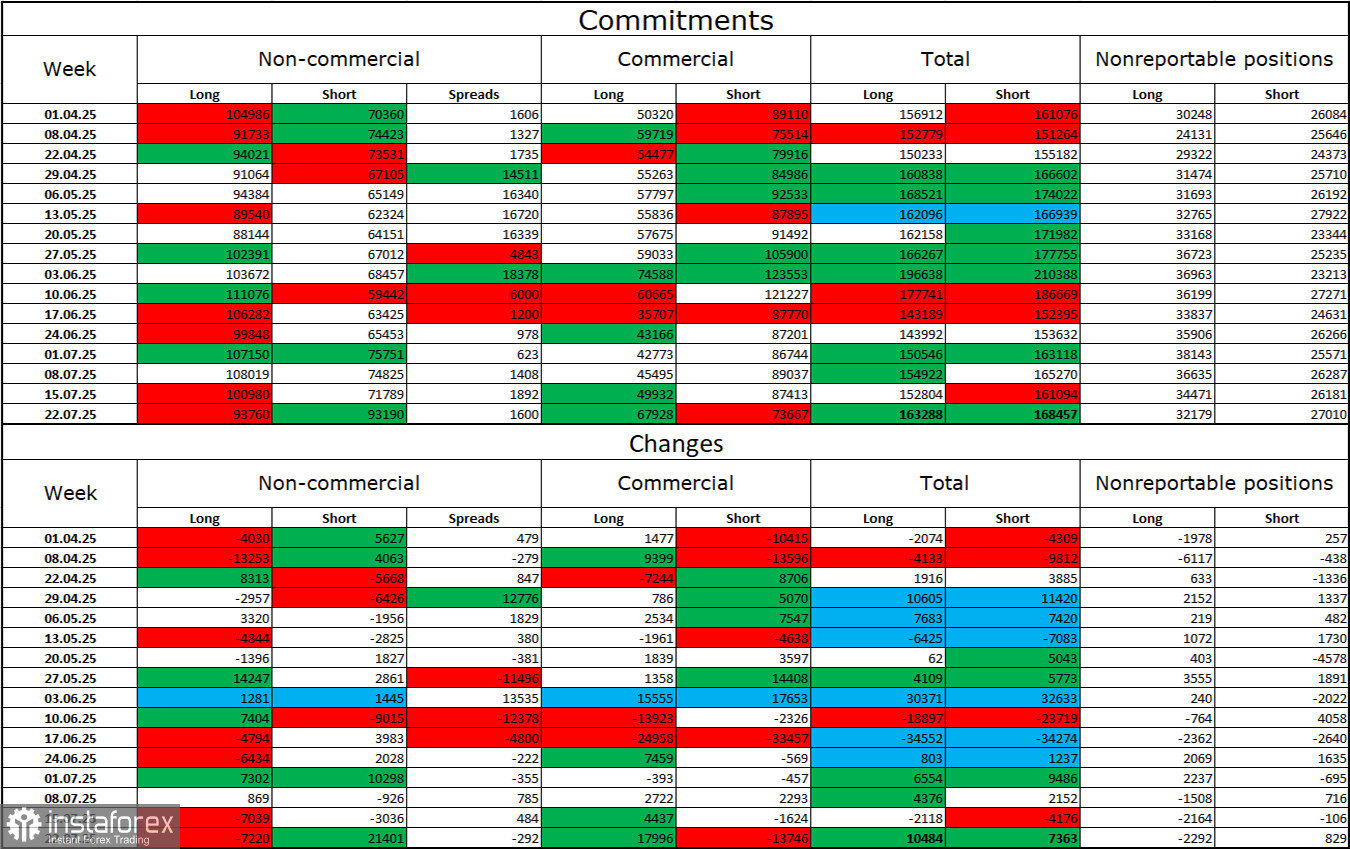

Commitments of Traders (COT) Report:

Sentiment among non-commercial traders has turned noticeably less bullish over the last reporting week. The number of long positions held by speculators decreased by 7,220, while short positions increased by 21,401. Bears have begun to retreat sharply, likely due to the growing appeal of the U.S. dollar amid recent major trade agreements by Washington. The gap between long and short positions is now virtually zero: 93,000 vs. 93,000.

In my view, the British pound still faces downward potential. The information background for the U.S. dollar was overwhelmingly negative during the first six months of the year, but it is gradually improving. Trade tensions are easing, major deals are being signed, and the U.S. economy is set to recover in the second quarter, supported by tariffs and increased investment.

U.S. and UK economic calendar:

Thursday's calendar includes three noteworthy, though not critical, releases. Their impact on trader sentiment later in the day is expected to be limited.

GBP/USD Forecast and Trader Recommendations:

Selling the pair was possible after a close below 1.3425 on the hourly chart, and again after a close below the 1.3378–1.3435 support zone on the 4-hour chart. The target of 1.3258 was reached yesterday. At this point, I would be cautious about further selling. However, I also do not see clear buy signals yet.

Fibonacci levels are drawn from 1.3371 to 1.3787 on the hourly chart and from 1.3431 to 1.2104 on the 4-hour chart.