See also

25.08.2025 01:03 AM

25.08.2025 01:03 AM

What attention will be paid to the European Union and the euro currency following Jerome Powell's Friday speech? Even though Powell's rhetoric was quite predictable, it had the effect of a bombshell on the market. Markets, which had been speculating since the beginning of 2025 about when the Federal Reserve would move to monetary easing, had been waiting for clear hints from Powell. And at the end of August 2025, they finally got them.

Based on this, next week will once again be devoted to the dollar, as has been practically every other week this year. The dollar remains the only actual driver of the market at the moment. And market participants have no shortage of reasons to trade the dollar. There's no need to bring up once again Donald Trump's trade war or protectionist policies—these topics have dominated the headlines for months.

The fact that the FOMC Chair now allows for the resumption of the monetary easing cycle can be interpreted in different ways. Powell merely acknowledged the possibility of a rate cut in September, while emphasizing that inflation remains the central bank's primary focus. As a result, he sowed new doubts in the market, even though the market itself reacted to his speech in a very straightforward manner. For example, the probability of a rate cut in September, according to the CME FedWatch tool, actually fell instead of rising and now stands at 75%. I would not be surprised if the likelihood of a new round of easing on September 17 declines further in the coming weeks.

And what about the euro and the European Union? On Sunday evening, European Central Bank President Christine Lagarde is scheduled to speak. On Monday, the German business climate index will be released. On Wednesday, German consumer confidence data will follow. And on Friday, retail sales, unemployment, and inflation figures from Germany will be published. In other words, all of next week's news will be related only to Germany—a single country within the European alliance. Put simply, I do not believe that this economic data will significantly affect market sentiment.

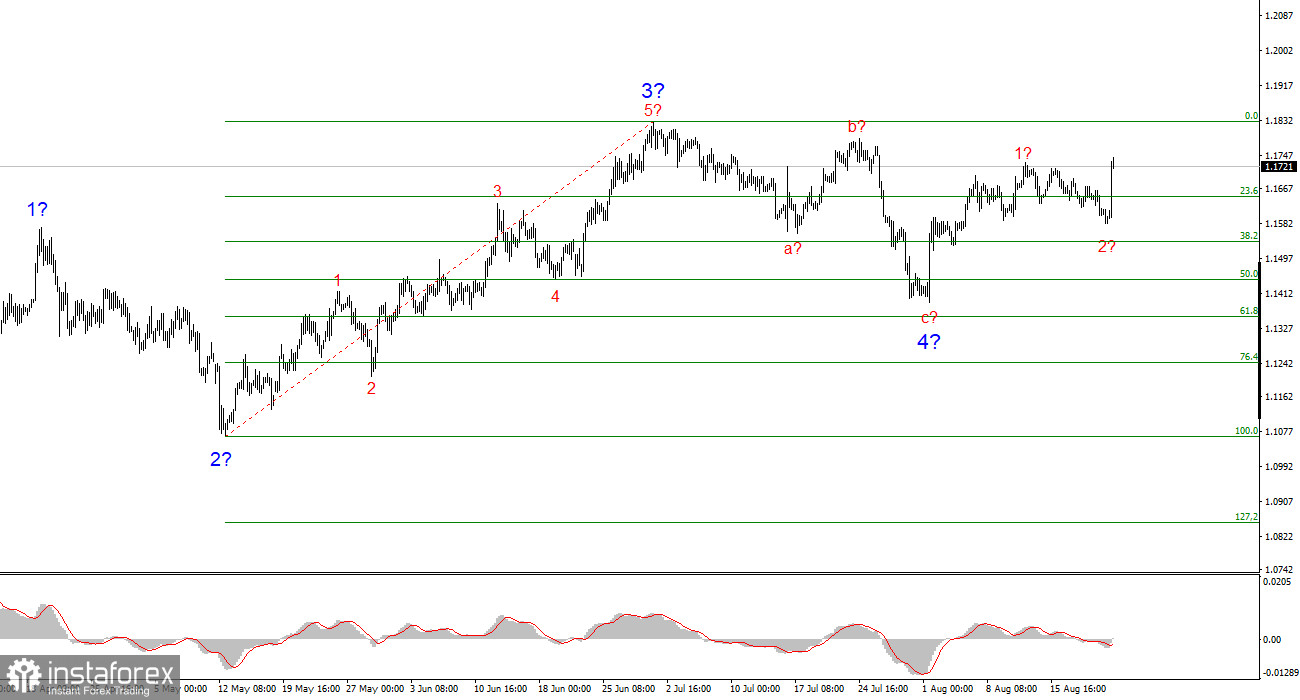

Based on the analysis of EUR/USD, I conclude that the instrument continues building a bullish trend segment. The wave structure remains entirely dependent on the news background tied to Trump's decisions and U.S. foreign policy. Targets for the trend segment may extend up to the 1.25 area. Accordingly, I continue to consider long positions with targets around 1.1875, which corresponds to the 161.8% Fibonacci level, and higher. I assume that wave 4 has been completed. Thus, it is still a good time to buy.

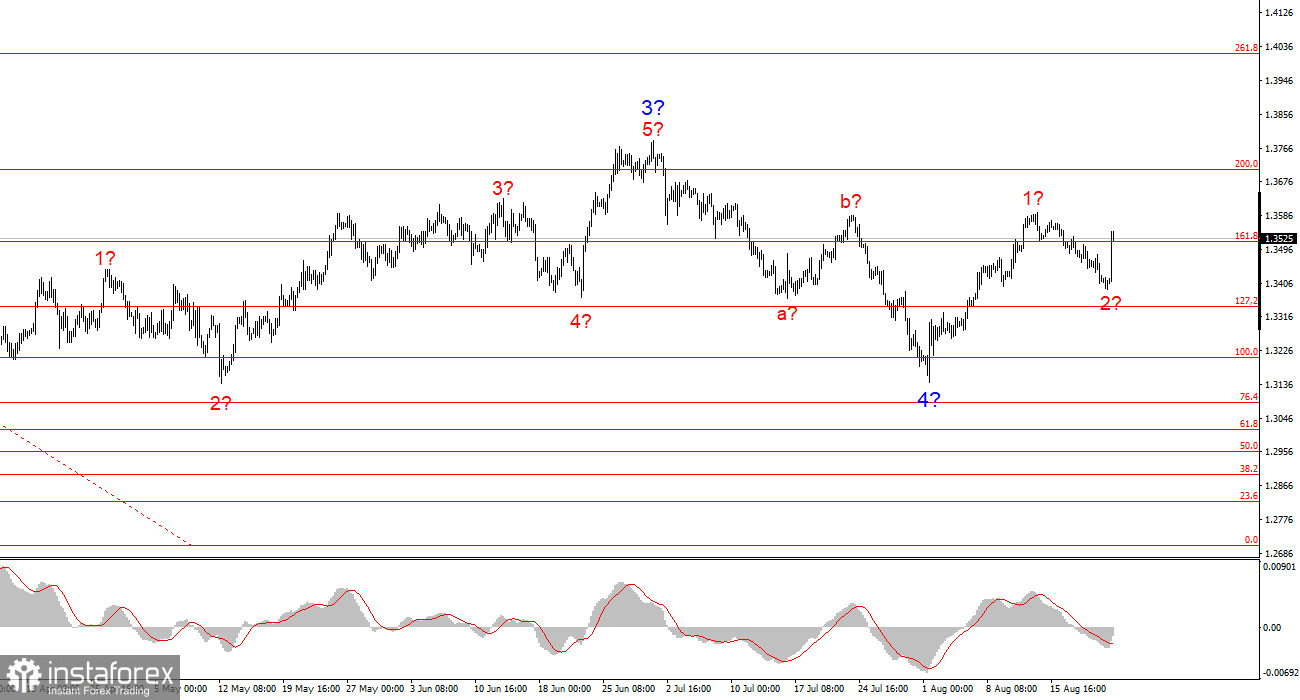

The wave structure for GBP/USD remains unchanged. We are dealing with an upward, impulsive trend segment. Under Trump, markets may face many more shocks and reversals, which could significantly affect the wave picture, but for now, the working scenario remains intact. Targets for the upward trend segment are now around 1.4017. At this time, I assume that the downward wave 4 has been completed. Wave 2 of 5 may also be near completion. Therefore, I recommend buying with a target of 1.4017.