Lihat juga

03.07.2025 01:17 PM

03.07.2025 01:17 PM

Wall Street keeps churning out record after record. On Wednesday, the S&P 500, driven by IT giants, once again set a fresh all-time high. The catalyst was not only another surge of interest in Apple, Nvidia, and Tesla — the beneficiaries of the tech rally — but also an unexpected twist in trade relations between Washington and Hanoi. The US agreed to introduce a 20% tariff on part of Vietnam's imports. And contrary to expectations, this announcement did not spark tension but instead triggered a wave of optimism in the markets.

Perhaps in the eyes of investors, the agreement signaled that America is once again dictating the terms. After a sharp decline in April, markets reacted enthusiastically to the partial rollback of the harshest tariffs — "Liberation Day" became a symbol of reversal. But only briefly. On July 9, the deadline for implementing new, higher tariffs will expire. Against this backdrop, the Nasdaq climbed nearly 0.8%, and the US dollar strengthened against all major currencies, including the yen.

If jobs data comes in weak, it will add fuel to the fire. In such a scenario, the US Federal Reserve could resort to rate cuts in the near term — exactly what the US. president has been pressing for. Donald Trump has also repeatedly demanded that Republicans in Congress pass his Big Beautiful Bill by Independence Day, July 4. The document has already cleared the Senate and moved to the House of Representatives.

If adopted, the US budget deficit will increase by $4 trillion, and government debt will climb to 125% or even 130% of GDP, the highest level since the end of World War II. If inflation remains persistently high, the Fed will be unable to slash rates aggressively, forcing the White House to choose: cut spending or admit default. The paradox is that the primary beneficiaries of this new fiscal architecture will not be those who need it most.

So, the Big Beautiful Bill has returned to the lower chamber of Congress. It is now up to the House of Representatives to decide whether Donald Trump will secure his political trophy by Independence Day. However, in the realities of American politics, such "gifts" are never easily delivered. The only chance to fulfill the White House's wishes lies in passing the Senate version of the bill without changes, debates, or amendments. But even within the Republican Party, there is no consensus on this matter. Recall that the bill initially passed the House by a margin of just one vote.

If there are not enough votes for a "blind" approval of the Senate version, Republicans will be forced down a longer path — to open discussions and begin introducing amendments. This would effectively open Pandora's box: any even minor revision would automatically send the document back to the Senate for reconsideration. In this case, the scenario of swift passage collapses. It is obvious that in its current form, the document is a compromise and politically overloaded. Now the question is whether Republican leadership in the House will manage to maintain the fragile balance of interests...

The tariff policy of the Trump administration is also behaving "off script." As Pantheon Macroeconomics senior economist Oliver Allen notes, WARN notices and Challenger reports point to mounting pressure, and weak hiring makes it even worse. In his view, it is precisely the tariff shock that is gradually spreading across the entire economy, limiting businesses' planning horizon. And indeed: if even Ford is forced to halt plants due to a shortage of Chinese magnets, what kind of supply chain resilience can we talk about?

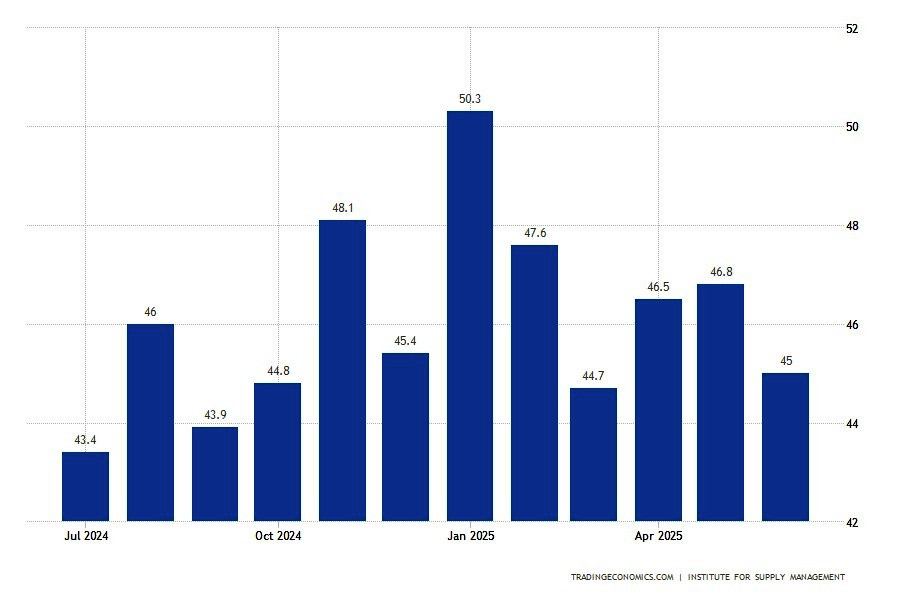

US manufacturing has been seriously caught in the gears of tariffs. The ISM Manufacturing PMI remained below the 50-point threshold, coming in at 49.0 in June versus 48.5 a month earlier. On paper, that looks like growth, but in reality, it is already the fourth consecutive month of contraction. Traditionally, such a level signals a decline in business activity. The figure fits neatly with the troubling dynamics in adjacent sectors:

The large-scale import tariffs were intended to protect the domestic market but in practice have played a cruel trick on the U.S. economy. Businesses, fearing future price increases, accelerated purchases in advance. As a result, an artificial surge in demand took place — followed predictably by a downturn. Deliveries slowed, and customs bottlenecks became the new normal. And now, extended logistics timelines are being interpreted by the market not as a sign of healthy demand, but as the result of supply chain distortion.

Supporting this view is a slowdown in the new orders sub-index — 46.4 in June after 47.6 in May. This marks five consecutive months of contraction. Production so far is holding up only thanks to the processing of accumulated backlogs (unfulfilled orders). But sooner or later, this resource will also be exhausted. The import component in the PMI, though it recovered to 47.4 after May's 39.9, remains far from comfortable levels.

The statistics are stubborn: current figures point to a clear cooling in the industrial sector. And this is already the second downward wave in the past three months. It appears that US manufacturing is suffocating under the burden of tariffs. Before the system adapts, it may take more than one quarter. In the meantime, the only option is to closely monitor how political decisions transform into economic consequences. By the way, the employment sub-index in business activity indices is often seen as a leading indicator for nonfarm payrolls, the official employment report.

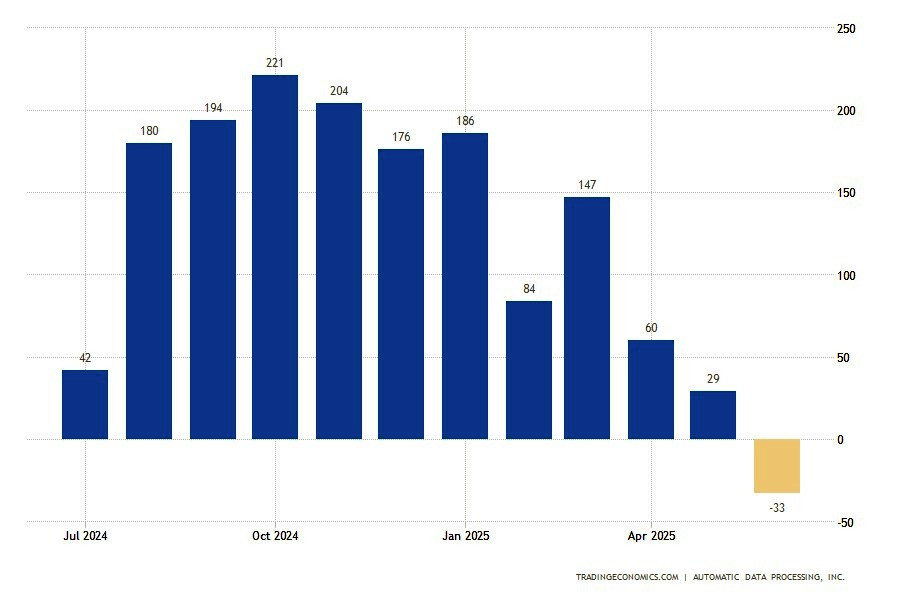

And the current dynamics are clearly sending signals that are far from bullish. The ADP data released the day before only reinforce these concerns. The private sector recorded its first decline in jobs since March 2023. While a gain of 95,000 was forecast, June's ADP reading fell to minus 33,000. The steepest drops were seen in:

"Though layoffs continue to be rare, a hesitancy to hire and a reluctance to replace departing workers led to job losses last month," ADP Chief Economist Nela Richardson noted. Her words sound like a diagnosis of the market: hiring is stalling, and employers are no longer in a hurry to fill openings.

Against this backdrop, the June ISM Services PMI is another potential trigger. In May, the indicator already fell below the key threshold to 49.9 points. If the index remains in negative territory again in June, it will serve as yet another argument in favor of an overall economic slowdown. Markets are hoping for at least a rebound to 51.6, as was seen in April, but another reading below 50 will spark serious concerns.

Overall, the picture is worrisome: manufacturing is cooling, services are faltering, hiring is losing momentum, and wages are losing steam. This week could prove pivotal for market sentiment.

There are also some positive reports. But they are, as the saying goes, yesterday's news and can serve only as indirect indicators. Despite grim signals from the hiring front, the US labor market unexpectedly gave bulls a reason for optimism. In May, the number of job openings (JOLTS) jumped by 374,000. The figure significantly exceeded the consensus forecast of 7.3 million and climbed to 7.769 million, marking the highest level since November 2024.

At first glance, the impressive surge can be interpreted as evidence of resilient demand for labor. But is that really the case? The largest contribution came from the accommodation and food services industry (+314,000), which points to a seasonal factor and, possibly, preparations for the tourism peak. The financial and insurance sector added 91,000 positions. Yet, alongside this increase in demand, there are also worrying signs:

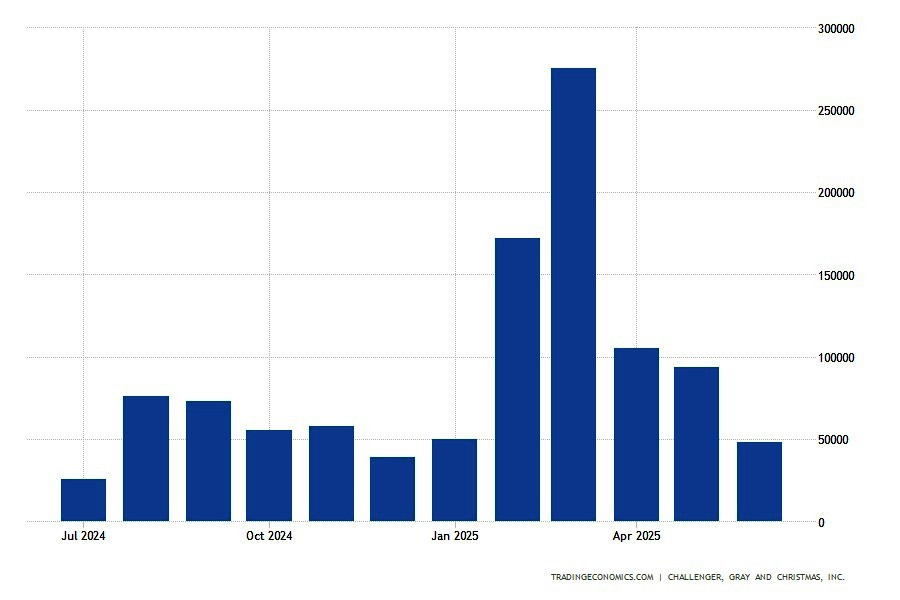

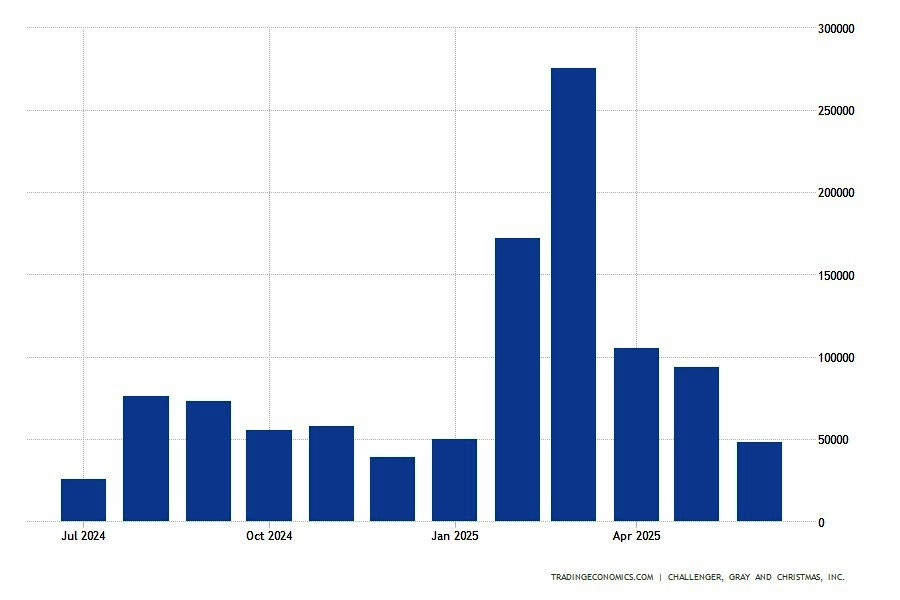

As for layoffs, they slowed sharply in June. According to Challenger, Gray & Christmas, the month saw announcements of 47,999 job cuts — the lowest figure since the start of the year. For comparison, in May this figure stood at 93,816. Such "calm" looks suspiciously serene against the backdrop of an already established trend. Since the beginning of 2025, companies have announced more than 744,000 cuts, setting a kind of five-year negative record. The public sector has been hit particularly hard. Nearly 289,000 jobs have been lost there.

Retail deserves special attention — a sector where almost 80,000 positions have been eliminated since the start of the year. The reasons are the same:

Ironically, retail was once considered the litmus test of economic health, and now it is the front line bearing the brunt of layoffs. Quarterly figures show an even starker contrast: in Q2, 247,256 layoffs were announced — the highest since 2020.

This is no longer just statistics but a potential turning point in the long-term trend. So in the final analysis, it is an illusion of revival against a backdrop of profound structural shifts. Yes, there are more job openings. At the same time, accumulated losses are growing, which have yet to fully appear in the macro data. Perhaps the labor market is the last bastion before the onset of the cooling phase.

Weekly unemployment claims data are confidently pointing to cracks emerging in the foundation. The four-week moving average of claims has reached the highest levels since August 2023. Meanwhile, the number of continuing claims climbed to 1.97 million — the highest reading in more than three years. Overall, the figures are not yet catastrophic. Especially considering that initial claims last week actually fell by 10,000 (to 236,000). Nevertheless, the indicator already stands significantly above this year's average.

And this is already a symptom — not yet a disease, but a weakening of immunity. Particularly concerning is the rise in long-term claims: up 37,000 in a week (nearly 2 million). This means it is becoming increasingly difficult for the unemployed to find new work. And even despite the symbolic reduction in claims from government employees, the situation in this segment also remains unstable, especially after the large-scale layoffs linked to DOGE. The official unemployment rate is still holding at 4.2%, but the Fed's forecasts have already been revised upward: to 4.5% by the end of 2025.

Until now, the head of the US Federal Reserve assessed the labor market as quite resilient. But when indicators start flashing yellow, it takes only one weak report for the light to turn red. And what Jerome Powell calls a "healthy" unemployment rate may soon cross into unacceptable territory. He acknowledges that uncertainty remains elevated — even if it has eased somewhat compared with the peak in April. However, what was previously perceived as "solid employment" now requires reappraisal.

Especially against the backdrop of rising claims and cooling consumer demand. As Brent Schutte of Northwestern Mutual stated bluntly, the labor market will be at the center of attention over the next few weeks. And this is not just a forecast but a warning. Because if the pace of softening persists, the Fed risks ending up in a position where it has to react not to inflation but to a slowdown in employment. And although the central bank chief insists that the Fed is "prepared for any scenario" regarding tariffs, markets may view such vagueness as a source of nervousness.

This kind of "flexibility," according to critics, has already repeatedly brought the US Federal Reserve into decision-making paralysis. ECB President Christine Lagarde, as well as the heads of the central banks of the UK, South Korea, and Japan, were quick to assure that they would have done "exactly the same" in Powell's place. Yet the solidarity of Powell's peers means nothing to traders trying to find at least a hint of a stable trajectory in monetary policy rhetoric.

At the same time, Trump's appointees on the FOMC (Christopher Waller and Michelle Bowman) are increasingly lobbying for a rate cut as early as July. Bowman has entirely shifted her rhetoric from hawkish to more dovish, citing slowing inflation. And Waller, from the Board of Governors, is unofficially tipped as Powell's potential successor. So his statements about the need to cut rates soon — especially against the backdrop of signs of hiring slowdown — may be less an economic analysis and more a political maneuver.

But for now, the question is different: will Jerome Powell be able to maintain balance? Or will the shadow of political pressure once again loom over US monetary policy? Inflation, contrary to expectations, has not yet spun out of control, and it is precisely this that has emboldened Donald Trump to intensify his attacks on the Fed chair.

More and more often, AI is stepping onto the labor market arena to compete with humans. Its products are slowly but steadily reshaping the employment landscape. And not always in favor of workers. Fiverr, a freelance platform, warns that not only line employees are under threat, but entire classes of professions: from lawyers and analysts to designers and project managers. According to Fiverr CEO Micha Kaufman, it doesn't matter if you are a programmer, designer, data analyst, or finance professional, "AI is coming for your jobs."

Amazon CEO Andy Jassy openly calls artificial intelligence "the most transformative technology of our lifetime" and promises it will change not only the customer experience but also the structure of employment within the company itself.

Dario Amodei of Anthropic believes that within five years, AI could wipe out up to 50% of all entry-level white-collar jobs and push unemployment up by 20%. "We, as the producers of this technology, have a duty and an obligation to be honest about what is coming," he noted. And all this is happening in a country where operating cash flow (OCF) is generated extremely unevenly.

Just 13 companies — led by Alphabet, Microsoft, Amazon, Meta, and Apple — accounted for half of the OCF growth over the past five years. In other words, the entire US economy is balancing on the shoulders of a dozen corporations. While the rest are forced to maneuver between tariffs, deficits, and rising costs. The labor market has already felt this pressure — and the next in line could be the consumer.

The previous NFP report showed that the US labor market is relatively resilient. In May, the US economy added 139,000 jobs, exceeding the consensus forecast of 130,000. However, revisions to data for prior months significantly undermined the overall picture:

This dragged the three-month average gain down from 155,000 to 135,000. For the first time since August 2022, the number of weekly claims has consistently exceeded 240,000, while continuing claims have reached nearly 2 million, the highest level in three years. The elevated level of continuing jobless claims, weakening labor force participation metrics, and the declining share of consumers who consider jobs "plentiful" only reinforce expectations of deterioration ahead.

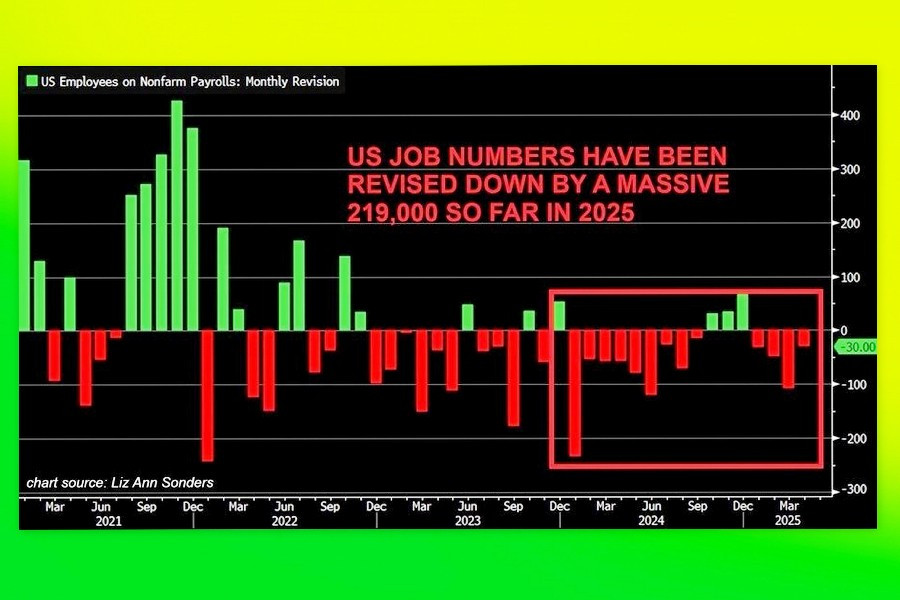

A particular cause for concern is the fact that in 22 of the past 28 months, employment data have been revised downward (see chart). According to the Quarterly Census of Employment and Wages, which relies on data from government unemployment programs, job growth rates from April 2024 through December 2024 were overstated. This increases the likelihood of a major benchmark revision as early as August. Economists estimate the cumulative adjustment could total between 800,000 and 1.125 million jobs for the year.

This would reduce the average monthly gain from the current 150,000 to 65,000–95,000. Referring to the consequences of tariff policy, William English, former senior Federal Reserve economist and professor at Yale School of Management, said that the situation was unprecedented and that such economic experiments had never been conducted before. He added that they were outside the bounds of modern US economic experience. Indeed, the impact of trade tariffs, public sector cutbacks, weak business confidence, and automation has so far only been partially reflected in official statistics.

Experts expect that June will see the creation of 110,000 to 129,000 jobs. At the same time, key attention will be focused not only on the number of new positions but also on the labor force participation rate. If unemployment remains low but the labor pool itself shrinks, this will point to structural weakening. The Fed will not be able to ignore such a signal.

This NFP release is postponed to Thursday, July 4, due to the Independence Day holiday. This makes it even more eventful, as it coincides with a series of other macro reports:

Markets are also eagerly awaiting the inflation report scheduled for July 15. Taken together with June's NFP, this data will determine whether the Federal Reserve moves to cut rates in the near term or opts to pause once again.