Veja também

16.07.2025 12:03 AM

16.07.2025 12:03 AM

Over the past few months, Trump has repeatedly criticized the Federal Reserve for its reluctance to cut interest rates. According to the U.S. President, such a high rate (4.5%) is unnecessary, given that inflation in the U.S. is low, while the high cost of borrowing adds several hundred billion dollars to the federal budget annually. However, the Fed—represented by Jerome Powell—has consistently responded that the full effects of tariffs can only be assessed in the fall, and inflation is highly likely to accelerate significantly in 2025, making monetary policy easing impossible, at least during the summer.

And now, for the second consecutive month, the U.S. Consumer Price Index is rising. In May, the increase was only 0.1% year-over-year, but in June, it rose to 0.3%. It's essential to note that inflation responds to tariffs with a significant delay, as American businesses had built up substantial inventories of goods before the onset of the global trade war. For several months, they have been able to sell these goods at old prices. Simply put, prices in the U.S. are rising very slowly because businesses wisely prepared for the new trade reality.

But any stockpile will eventually run out, and soon businesses will have to order goods from abroad at new prices. When that happens, inflation will begin to reflect the actual impact of Donald Trump's trade war. I don't believe that Trump or his many advisers are incapable of interpreting basic economic statistics and truly don't understand why inflation has remained relatively low in recent months. I believe Trump is well aware of the inevitability of rising consumer prices, but he simply isn't interested in that figure.

Since tariffs remain in effect, continue to rise, and expand in scope, demand for many goods is falling. As demand falls, the economy slows. As inflation increases, money loses value. Therefore, Trump needs to stimulate the American economy to mask the effects of the tariffs. To achieve that, low borrowing costs are necessary so that credit flows freely and funds are directed toward developing the economy, industry, and business. However, Powell, as before, refuses to ease policy, thus putting Trump's grand plan at risk of failure.

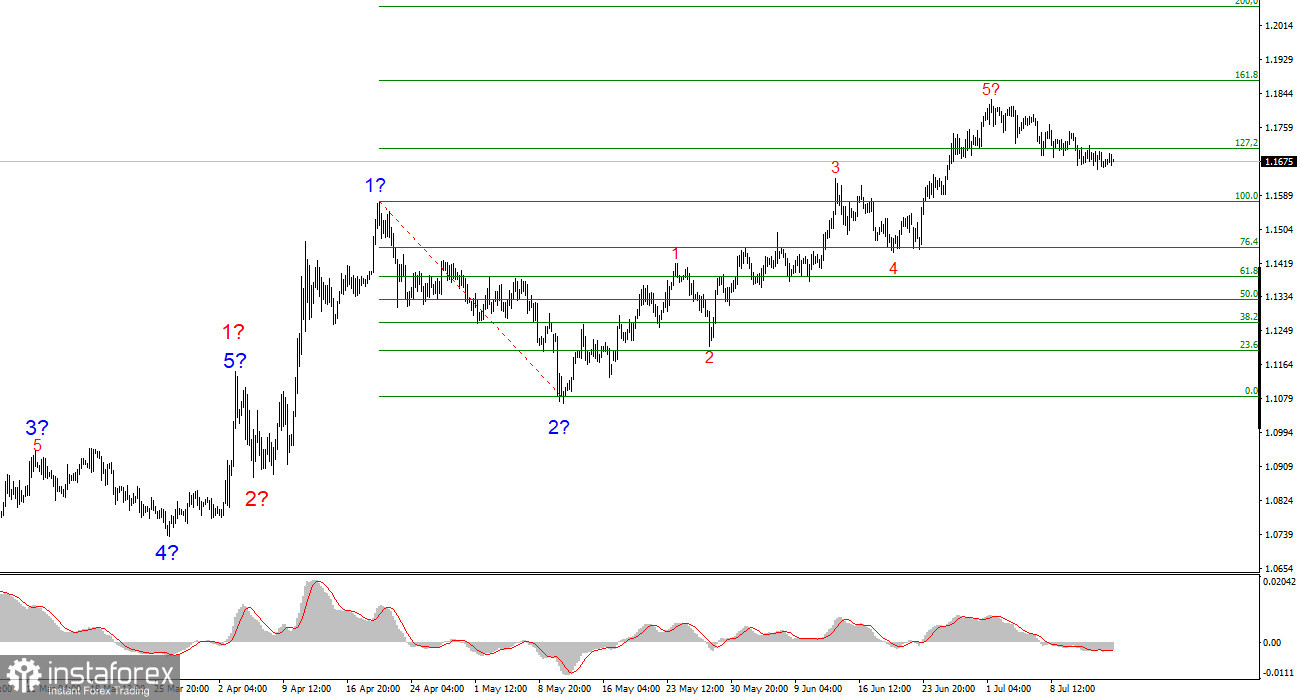

Based on the analysis of EUR/USD, I conclude that the instrument is continuing to build a bullish trend segment. The wave pattern remains entirely dependent on the news backdrop related to Trump's decisions and U.S. foreign policy, with no positive changes yet evident. The targets of this trend segment may extend up to the 1.25 area. Accordingly, I continue to consider buying opportunities with targets around 1.1875, which corresponds to the 161.8% Fibonacci level, and higher. A corrective wave sequence is expected in the near future, so new euro purchases should be considered after the completion of this corrective structure.

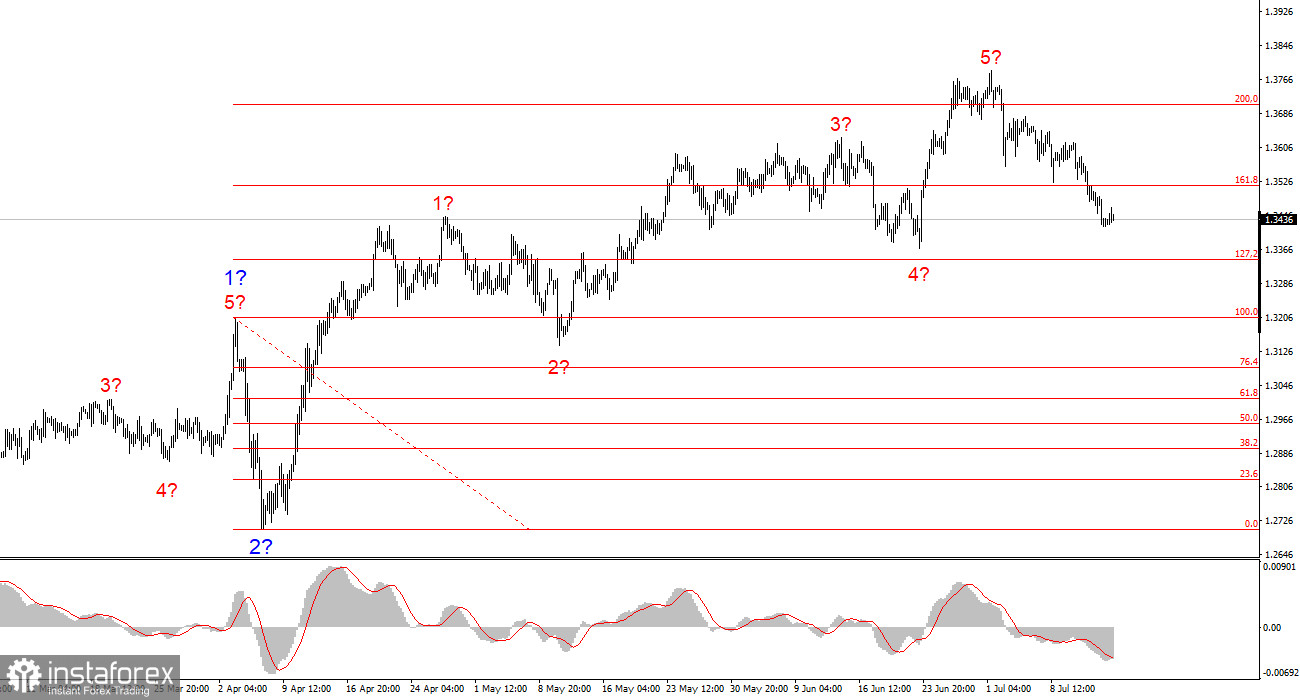

The wave pattern for GBP/USD remains unchanged. We are dealing with a bullish, impulsive trend segment. Under Trump, the markets may face many more shocks and reversals that could significantly affect the wave structure, but for now, the working scenario remains intact. The targets of the bullish segment are now located near 1.4017, which corresponds to the 261.8% Fibonacci level from the presumed global wave 2. A corrective wave sequence is currently underway, which typically consists of three waves.