Veja também

08.09.2025 03:47 AM

08.09.2025 03:47 AM

On Friday, the GBP/USD pair also posted a strong gain, fully recovering from Tuesday's decline "for unknown reasons." The reason, of course, became clear the next day: the market was reacting to rising UK bond yields, which had been increasing for more than just a day. On Tuesday, we noted that the dollar's sharp fall seemed like ordinary market-maker manipulation—first dumping the pound, then buying it up at bargain prices. And most likely, this was not accidental. We continue to expect a new round of prolonged dollar weakness.

On the 4-hour chart, price has returned for a third time to the 1.3550 level and has failed once again to break above it. On Monday, even a new downward corrective move may start, which still cannot be considered finished. Nevertheless, even if a new pullback begins, our outlook is still upward. It's important to understand that the global, structural fundamental backdrop is still not on the dollar's side. As time goes on, traders receive new data that pushes them towards more dollar selling.

Macro statistics from the past four months have shown there's been no "shock" from tariffs in the US economy. Instead of a shock and a sharp collapse, we've seen a steady and systematic deterioration of the data. So this is a natural, logical reaction of the economy to the new White House policy.

That said, the numbers themselves aren't worth getting hung up on. Since Donald Trump fired Bureau of Statistics director Erica MacAnterfer, it's almost certain that someone new will be brought in. As with the Federal Reserve, this will be someone loyal not just to Trump's policies, but his direct instructions. Soon, we might see a sharp improvement in US macro indicators—but will anyone trust them? After all, Trump merely needs to hide the real numbers and present only the positives. Which average American will bother to check the real ISM Manufacturing Index?

Sure, businesses, banks, and firms will discuss negative trends, but they lack access to the full national statistics. Their criticism can be easily silenced by arguing that problems are isolated to certain companies, not the US overall.

From our perspective, even if macro data starts to look better in the coming months, it won't save the dollar—because the market now fears data falsification. Beyond this, Trump is still pressuring the Fed, and soon the central bank's policy could become dovish for a long time. To keep the economy growing at double digits, the Bureau of Statistics can simply adjust all other data. Admittedly, this is just a hunch, but that hunch is looking more plausible by the day.

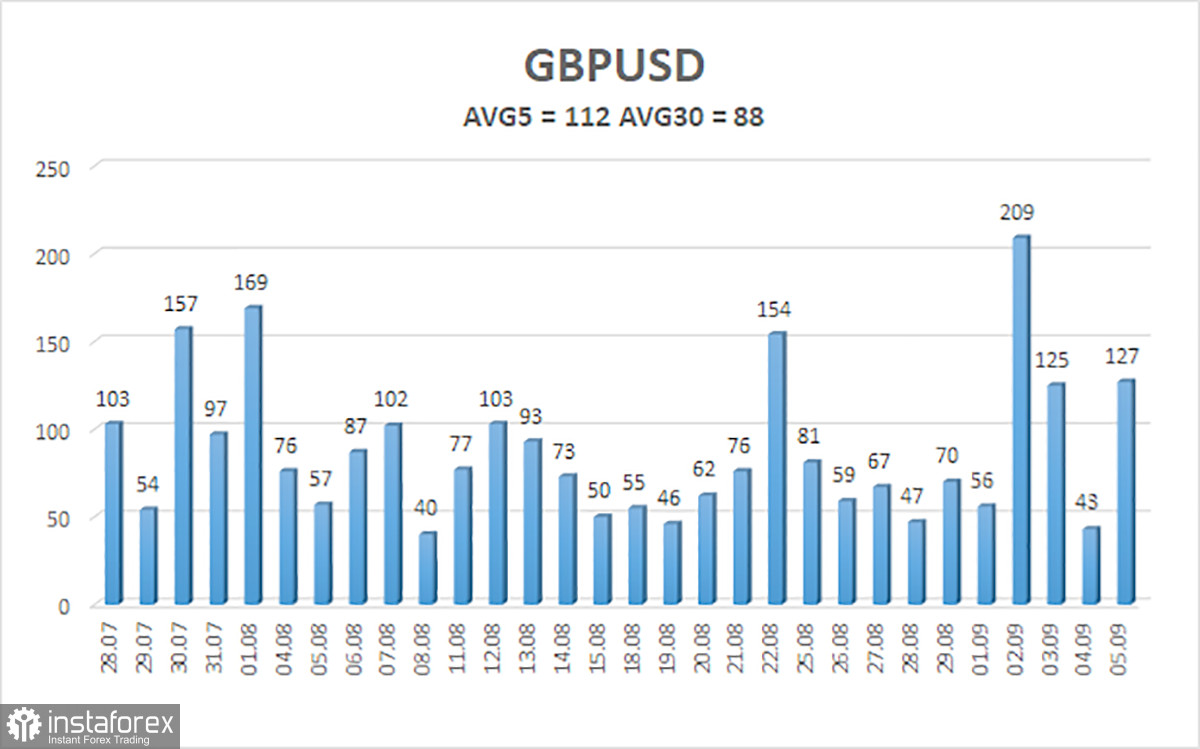

The average volatility of GBP/USD over the last five trading days is 112 pips—"high" for this pair. On Monday, September 8, we expect movement within the 1.3393–1.3617 range. The upper channel of linear regression remains upward sloping, indicating a clear uptrend. The CCI indicator dipped into oversold territory again, warning of renewed bullish momentum.

S1 – 1.3489

S2 – 1.3428

S3 – 1.3367

R1 – 1.3550

R2 – 1.3611

R3 – 1.3672

The GBP/USD pair is once again aiming to resume its uptrend. In the medium term, Trump's policies are likely to continue weighing on the dollar, so we do not expect dollar strength. Thus, as long as the price is above the moving average, long positions targeting 1.3611 and 1.3672 are much more relevant. If the price is below the MA, small short positions can be considered on a purely technical basis. From time to time, the dollar posts corrections, but for a confirmed uptrend to emerge, we need real signs of an end to the World Trade War or other major positive factors.