Vea también

14.07.2025 12:42 AM

14.07.2025 12:42 AM

In my reviews, I've regularly noted that the decline in demand for the U.S. dollar is not just a matter of price depreciation. We're talking about a currency that for many years was considered the global standard. While the dollar remains the world's primary medium of exchange, its position has significantly weakened in 2025.

I won't repeat the obvious reasons why the dollar is falling. Instead, I'll focus on what this could lead to. The demand for the U.S. dollar is dropping not only in the foreign exchange market, where few expect it to strengthen, but also, therefore, few are buying it. The demand is falling globally. This is partly because the currency itself is depreciating. And partly because Donald Trump's policies are turning it from a safe-haven currency into a risk asset. Now let's ask ourselves: what kind of currency would everyone prefer to deal with? One that is risky and depreciating, or one that is safe and stable? The answer is obvious.

Goldman Sachs made a similar statement recently: the dollar is starting to show signs of becoming a risk currency. Bank economists note that the pressure on the dollar comes not so much from Trump's tariffs, but from the economic and political uncertainty surrounding the U.S., the instability of the American government's course, and the shift of investor assets away from the U.S. The last point is particularly interesting in light of new highs on the stock market. That is, American companies' shares are in demand, but international investors are trying to keep their distance. What does that suggest? It means the U.S. stock market is growing due to domestic demand, from Americans themselves, many of whom are buying domestic stocks because they don't have access to foreign securities, or don't want to deal with them.

In the U.S., investing is much more widespread than in many countries, so even a farmer named John in Texas might own several dozen Apple shares. It is precisely these "farmers" who are creating the demand, while foreign investors prefer to redirect their capital elsewhere.

In general, the outlook for the dollar is, at best, uncertain. The U.S. stock market may continue to grow on the back of domestic demand, but U.S. bonds—on the contrary—are struggling, even due to low internal confidence in the Trump administration. Trump may become the starting point for the global de-dollarization process, and if that process begins, not even Trump will be able to stop it. What can the U.S. president do—raise tariffs ten more times?

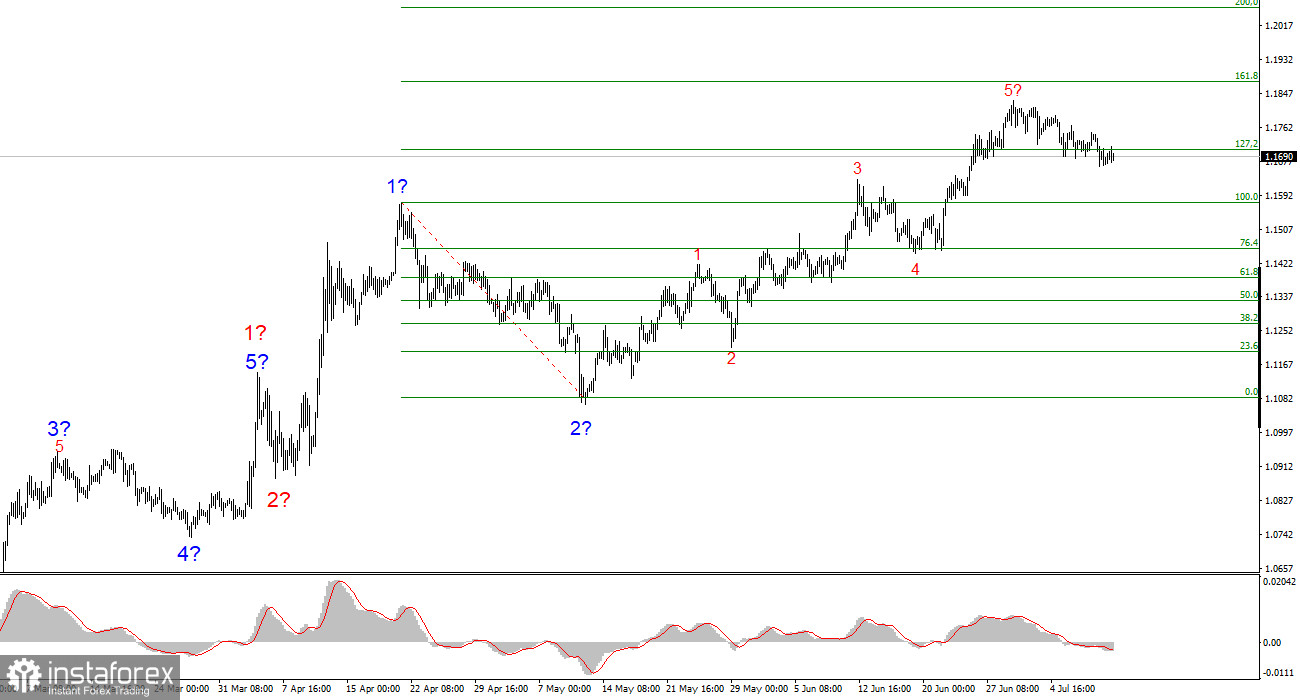

Based on the analysis of EUR/USD, I conclude that the instrument continues to form an upward section of the trend. The wave structure still entirely depends on the news background related to Trump's decisions and U.S. foreign policy, and there are still no positive changes. The targets of this trend section may extend as far as the 1.25 level. Therefore, I continue to consider buying with targets near 1.1875, which corresponds to the 161.8% Fibonacci level. A corrective wave set is expected in the near future, so new euro purchases should be made after this corrective structure is completed.

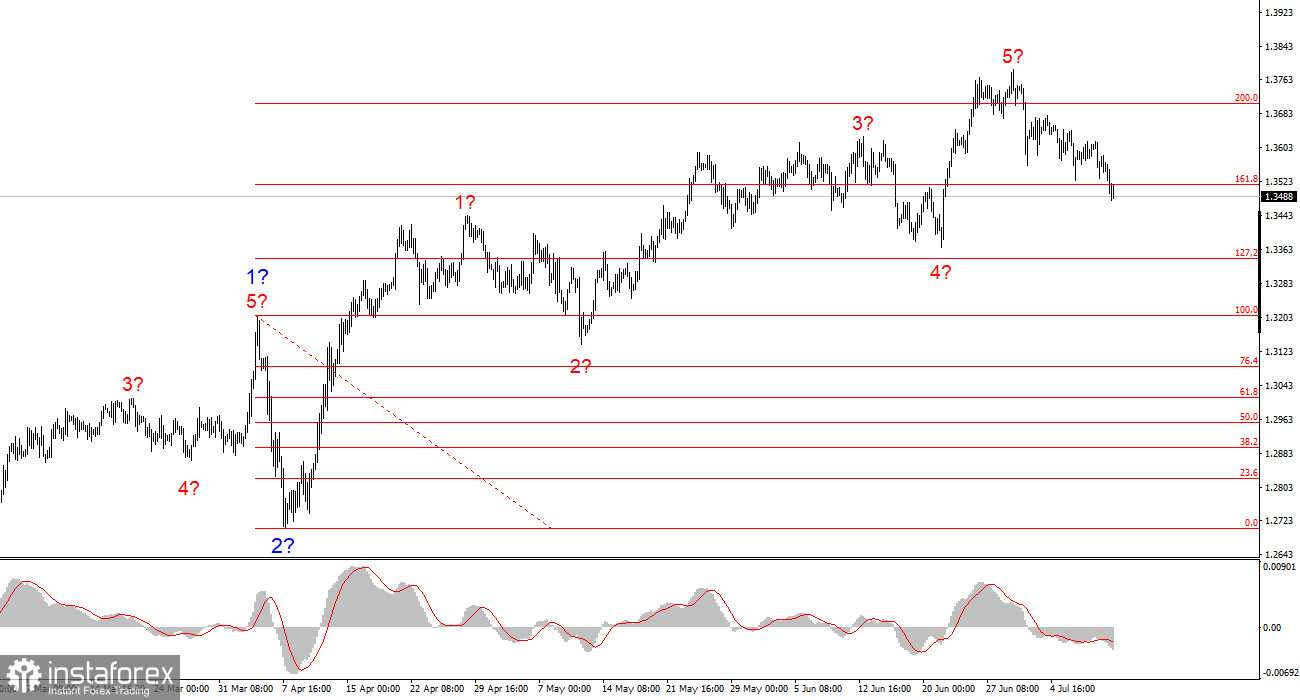

The wave structure of the GBP/USD instrument remains unchanged. We are dealing with an upward, impulsive section of the trend. Donald Trump, the markets may face many more shocks and reversals, which could seriously affect the wave picture, but at the moment, the main scenario remains intact. The targets of the upward trend section are now located near 1.4017, which corresponds to the 261.8% Fibonacci level of the presumed global wave 2. It is assumed that a corrective wave set has begun. Classically, it should consist of three waves.