Vea también

14.08.2025 12:39 AM

14.08.2025 12:39 AM

The tensions surrounding the Federal Reserve are not subsiding. For several consecutive months, Donald Trump has tried in every possible way to achieve Jerome Powell's dismissal, but without success. Powell is determined to serve out his term and continues to prioritize inflation above all else. This was still the case just a week ago — until updated three-month U.S. labor market data was released. It turned out that far fewer jobs had been created than economists expected, and significantly fewer than the May and June reports had indicated. Since then, talk has persisted about a rate cut in September and at least one more before the end of the year.

U.S. Treasury Secretary Scott Bessent, who could become the next Fed Chair, expressed the view that the Fed should cut rates by 50 basis points next month. Bessent based this conclusion on the same Nonfarm Payrolls report. He noted that if the May and June data had initially been accurate, the Fed would have decided to cut rates in June and July. Therefore, in September, it will have to make up for lost time. Failing to do so could prove costly for the U.S. economy.

Bessent also believes that economists have drawn incorrect conclusions about the impact of trade tariffs on inflation. All recent reports have shown only a very modest increase in the Consumer Price Index, which still allows the FOMC to ease policy.

I believe the Treasury Secretary has no more influence over Powell and the FOMC than Trump does, but it must be acknowledged that Bessent's point has merit. The Fed is indeed behind on policy easing, given the latest labor market data. I believe the Fed will cut rates at all three meetings in 2025. However, it is worth not ruling out a 50-basis-point cut in September. In my opinion, such a scenario would only accelerate the U.S. dollar's decline. The next Fed meeting is still some time away, and for now, market attention is focused on the upcoming talks in Alaska on August 15.

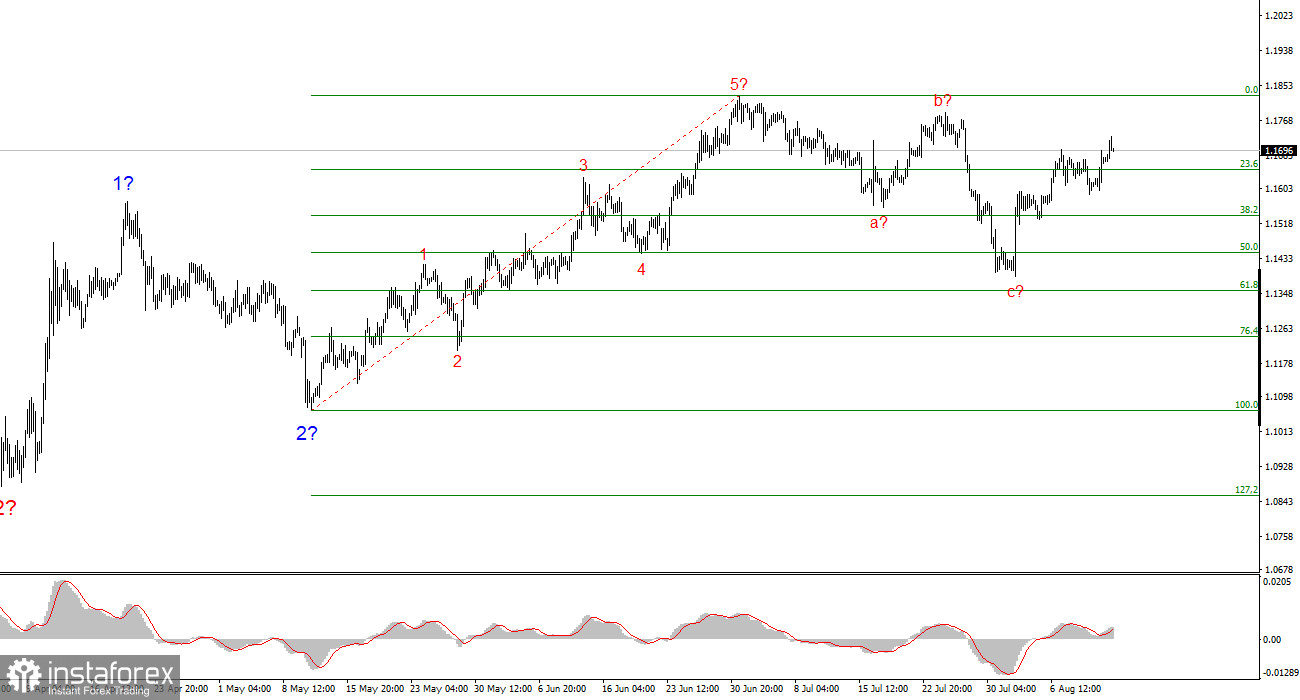

Based on the EUR/USD analysis, I conclude that the instrument continues building an upward trend segment. The wave count still depends entirely on the news background related to Trump's decisions and U.S. foreign policy. The targets for this trend segment may extend as far as the 1.25 area. Therefore, I continue to consider buying, with targets near 1.1875 (equivalent to the 161.8% Fibonacci level) and higher. I assume that wave 4 construction has been completed. Accordingly, now is a good time to buy.

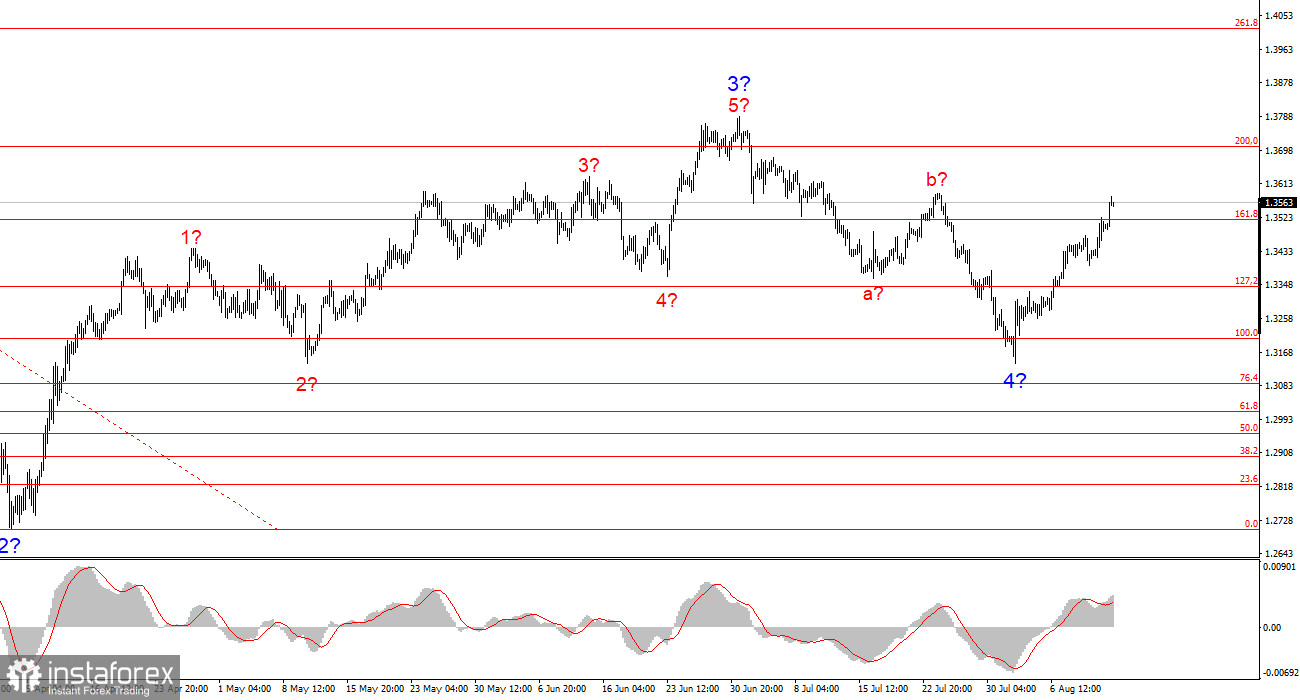

The wave count for GBP/USD remains unchanged. We are dealing with an upward, impulsive trend segment. Under Trump, markets could face many more shocks and reversals that could significantly affect the wave pattern, but at the moment, the working scenario remains intact. The targets for the upward trend segment are now located near 1.4017. At present, I assume that the downward wave 4 construction has been completed. Therefore, I recommend buying with a target of 1.4017.