Vea también

12.11.2025 12:47 AM

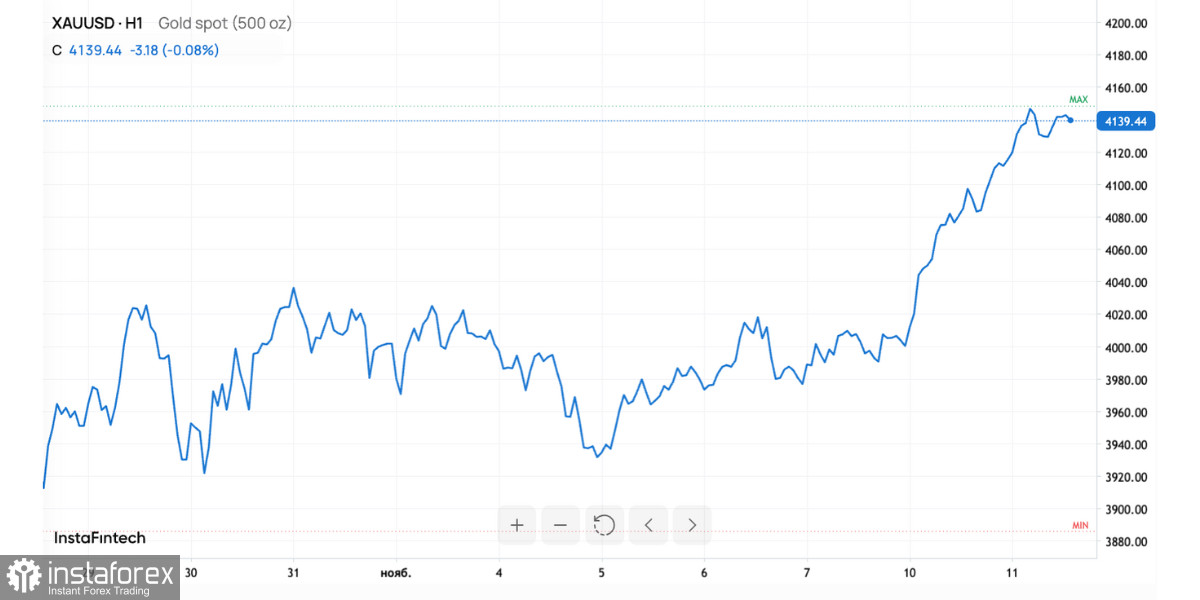

12.11.2025 12:47 AMThe global gold market is showing strength once again. At the beginning of November, the price of the precious metal surged nearly 3%, settling above $4,100 per ounce and reaching a two-week high. The reason is simple: investors are increasingly discussing the Federal Reserve's imminent rate cuts. In light of weak U.S. economic data, gold has become a primary safe haven for those seeking stability in a turbulent economy.

The increase in gold prices in November is not a flash of random optimism, but rather a reflection of fundamental processes in the global economy. Recent U.S. statistics have come in worse than expected. In October, the number of jobs decreased, particularly in the public sector and retail. Simultaneously, consumer sentiment dropped, and households became more cautious in their assessments of income and future expenditures.

Such data signals to the markets that the U.S. economy is losing momentum, which means the Fed may not only pause its tightening cycle but could also move toward rate cuts as early as December. Currently, the probability of this event is estimated at approximately 64%, rising to 77% by January. This provides a favorable backdrop for gold. When the yields on dollar-denominated assets fall, investors search for alternatives, and the metal, which does not offer coupons or dividends, becomes the natural choice.

An important aspect is investor sentiment. After several months of volatility in the stock market, gold is seen as a safe haven. The longer political and economic uncertainty persists, the higher the demand for "hard value."

The closure of the U.S. federal government, now in its 40th day, has intensified this sense of instability. Even news of a possible agreement in the Senate did not change sentiments. For now, with the flow of economic data limited, market participants are relying more on expectations than on facts. These expectations are working in favor of gold.

The rise of the metal is accompanied by increases in other precious assets. Silver has risen by 4.5% to $50.46 per ounce, platinum by 2.4%, and palladium by 3.1%. This indicates a broad reassessment of the precious metals sector as investors shift to more defensive asset classes.

If the momentum continues, gold could test $4,200–$4,300 per ounce by the end of the year, and growth toward $5,000 is not ruled out in the first quarter of next year. Everything will depend on how quickly and decisively the Fed moves toward rate cuts.

However, there is a second side to this story. If the U.S. economy shows signs of recovery and the dollar strengthens, the rise in gold may slow. Meanwhile, geopolitical risks, bond market instability, and potential budget crises in Washington continue to support interest in the metal.

Gold is reclaiming its status as the primary beneficiary of market uncertainty. Weak U.S. data, expectations for rate cuts, and political conflicts within the country have created ideal conditions for growth.

Investors are increasingly betting that the era of expensive money is coming to an end, and gold continues to affirm its status as a universal protective instrument. It is not just rising—it reflects the mood of the times: exhaustion with risk, fear of the future, and the desire to preserve real value in a world where confidence is dwindling.