আরও দেখুন

29.09.2025 04:02 AM

29.09.2025 04:02 AM

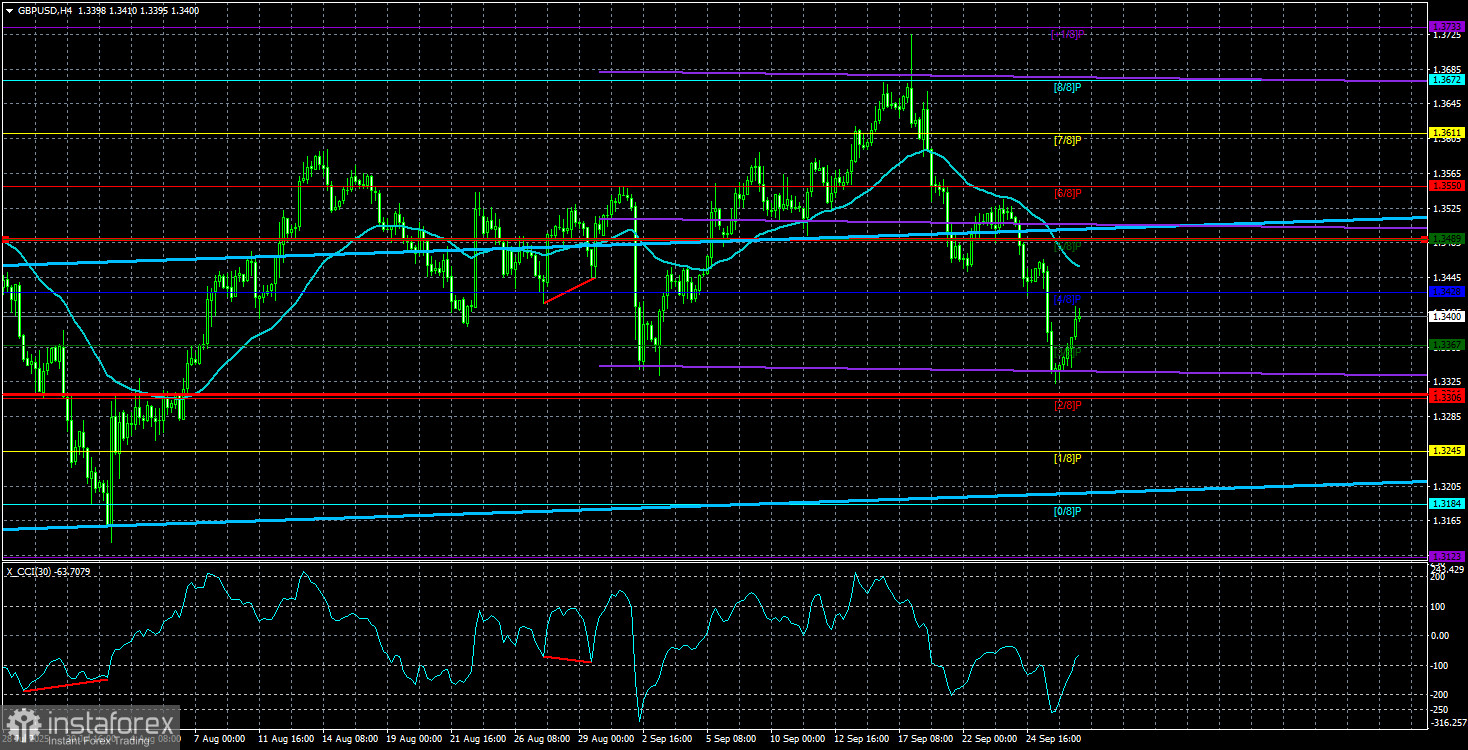

Over the past two weeks, the GBP/USD pair has lost significant value. It cannot be said that the decline in the British pound was unjustified, but at the same time, it cannot be called "fully logical" either. Simply put, the market used almost all recent news against the pound. However, due to this decline, the technical picture has changed only on the lower timeframes. On the higher ones, we are still dealing with the long-term upward trend of 2025.

This week, the U.S. dollar will try to defend its hard-won positions. Yet the overall picture again looks unfavorable for the greenback. Donald Trump introduced new tariffs on pharmaceuticals, trucks, and furniture, signaling a continuation of the trade war and a new escalation of global trade tensions. This alone is already a significant factor for the market to end the "dollar buying spree" of the last two weeks.

Additionally, key U.S. data on the labor market, unemployment, and business activity will be released. Recall that these reports, alongside inflation figures, currently define the course of monetary policy. Paradoxically, the worse the U.S. labor market performs, the better for the dollar. A fifth consecutive month of weak NonFarm Payrolls will significantly raise the likelihood of two more Fed rate cuts before year-end—an outcome considered favorable for the dollar. Still, even in that case, we would not expect a sustained "dollar trend."

The U.S. currency may strengthen by another 100–200 points, but it should be understood that we are most likely only at the very early stage of a "counter-dollar trend." The dollar had been rising for 16–17 years since 2007. With Trump's return to office, the global trend may have shifted, and the dollar could now be in decline for the next 8–10 years. Therefore, an additional 100–200–300 points of appreciation will not change its long-term outlook.

We should also note the upcoming U.S. unemployment and ISM reports. The American economy posted strong GDP growth in the second quarter, but the labor market is weakening, unemployment is rising, inflation is climbing, job openings are falling, and business activity in the manufacturing sector is declining. As we can see, the only positive news is the GDP growth. Therefore, if the next batch of U.S. macroeconomic data again comes in weak, the dollar may resume its decline regardless of the high odds of two more Fed rate cuts.

By the way, according to the U.S. Bureau of Labor Statistics, September's Nonfarm Payrolls are forecast to add only "39,000" new jobs. Recall that a normal level for this indicator is 150–200,000, with an acceptable minimum of around 100,000. Thus, the report could show another discouraging result for the fifth straight month. From a technical perspective, a consolidation above the moving average is required to anticipate a new upward leg. The CCI indicator is already signaling a likely rise.

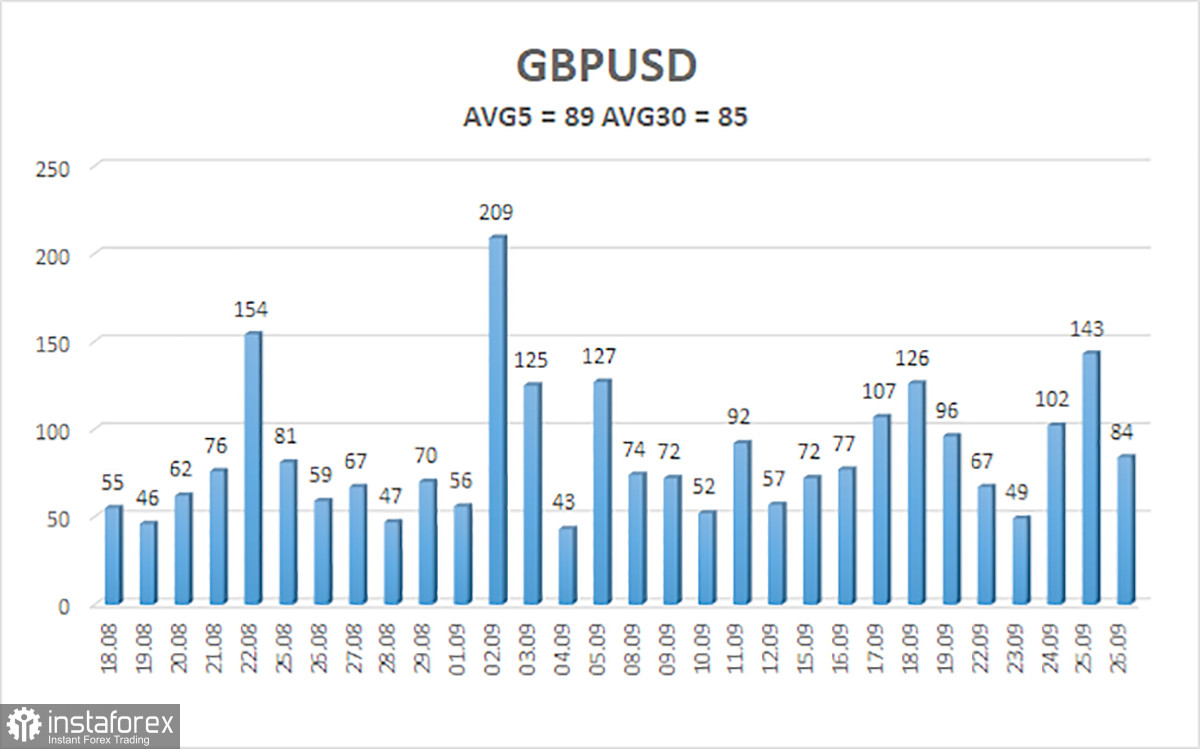

The average volatility of GBP/USD over the last five trading days is 89 pips, which is considered "normal" for this pair. On Monday, September 29, we therefore expect movement within the 1.3311–1.3489 range. The longer-term linear regression channel is pointing upward, clearly indicating a bullish trend. The CCI has once again entered oversold territory, which again warns of a possible resumption of the uptrend.

S1 – 1.3367

S2 – 1.3306

S3 – 1.3245

R1 – 1.3428

R2 – 1.3489

R3 – 1.3550

The GBP/USD pair is once again in correction, but its long-term outlook remains unchanged. Trump's policies will continue to pressure the dollar, so no sustained appreciation is expected. Accordingly, long positions targeting 1.3672 and 1.3733 remain much more relevant if the price holds above the moving average. Meanwhile, if the price trades below the moving average, small shorts toward 1.3311 and 1.3306 can be considered on technical grounds. From time to time, the U.S. currency exhibits corrections (as it does now), but for a sustained trend reversal, it would require concrete signs of an end to the trade war or other major positive factors.