See also

12.06.2025 10:37 AM

12.06.2025 10:37 AMThe fresh U.S. Consumer Price Index (CPI) data released on Wednesday, although below the consensus forecast, confirmed the persistence of inflationary pressure. This fully justifies the Federal Reserve's reluctance to resume interest rate cuts.

According to the CPI report, U.S. inflation rose year over year from 2.3% to 2.4%, while the forecast was 2.5%. The core inflation rate remained at 2.8%, below the expected 2.9%. On a monthly basis, inflation rose less than forecast.

There are two main reasons. The first is global in nature, tied to the ongoing trade war between the U.S. and China. The recent round of talks in London yielded only one tangible result—an agreement on rare earth metals trade. However, this did not resolve the complex economic stalemate, which largely contributes to another issue in the U.S. economy: persistently high inflation.

The decoupling of trade links between China and the U.S. does not benefit the latter, whose real economy (aside from specialized sectors) has long relied on imported goods. For decades, Americans purchased Chinese-manufactured products—everything from Nike to smartphones and computers—designed in the U.S. but produced mostly in Asia, particularly China. Donald Trump's ill-conceived tariff policies disrupted these economic ties, ultimately fueling price increases on goods now arriving through more expensive, indirect routes.

Since global financial markets are heavily tied to the U.S., they have reacted negatively to this geoeconomic instability and the resulting high inflation. This inflation, in turn, pushes the prospect of further Fed rate cuts into the distant future. That's why we are witnessing market pessimism and decreased demand for stocks, cryptocurrencies, and oil. Meanwhile, gold prices are understandably gaining support as a safe-haven asset. Even the dollar—normally expected to strengthen on a CPI report—remains under pressure due to waning interest in dollar-denominated assets globally.

The negative sentiment seen in European trading will likely carry over into the U.S. session. Although inflation showed only a slight uptick, it is still enough to reduce the likelihood of near-term Fed rate cuts, dampening demand for equities. The crypto market will likely remain under pressure. The U.S. dollar index (ICE) is expected to consolidate around the 98.00 mark. Gold may continue to attract buying interest, potentially moving toward recent highs.

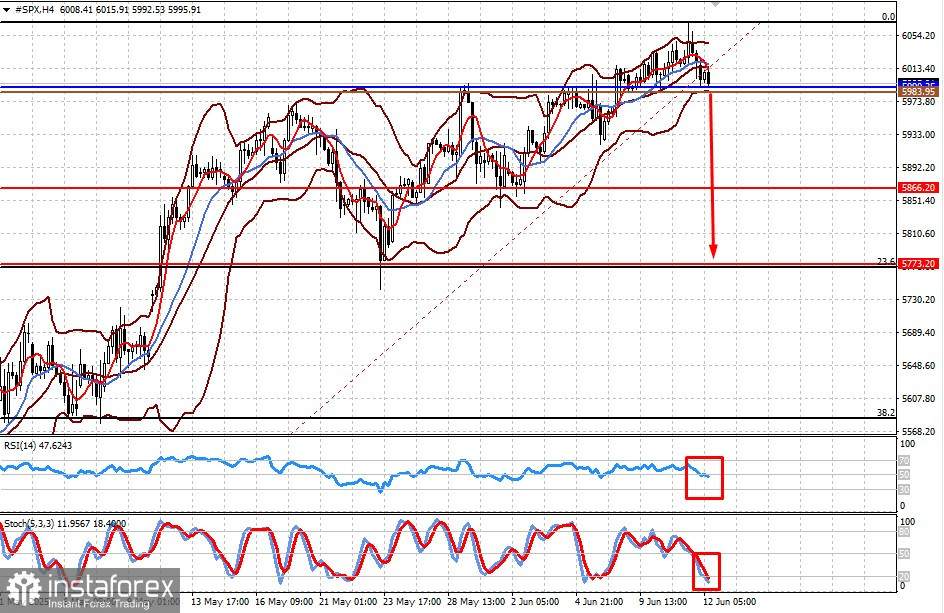

The S&P 500 futures contract shows a local downward reversal, suggesting the possibility of a corrective decline in U.S. equities. Amid broad pessimism, a break below 5990.25 may lead to a fall first to 5866.20 and then to 5773.20, corresponding to a 23% Fibonacci retracement. The level of 5983.95 could be used as a trigger for selling.

Gold prices may see a moderate upside amid overall market negativity. A rise above 3351.00 could intensify the bullish trend, with a target toward 3408.00. The 3355.00 mark could serve as a good entry point for buying.