See also

16.07.2025 09:51 AM

16.07.2025 09:51 AMThe U.S. consumer inflation report released yesterday showed that Donald Trump's policy to "make America great again" is, for now, mainly making life in America more expensive.

According to the data, year-over-year inflation rose more than expected, up to 2.7% from 2.4%, beating the forecast of 2.6%. In core terms, the increase was smaller than expected — 2.9% versus 2.8%, while the market had anticipated 3.0%. On a monthly basis, headline inflation in June matched the consensus at 0.3%, but core inflation rose by only 0.2%, below the expected 0.3%.

How did the markets react to this news?

The reaction was fairly muted. On one hand, it's already clear to most that the president's aggressive tariff policy is the primary driver of rising prices for goods and services. Disruptions in supply chains caused by the ongoing tariff reshuffling are already impacting the U.S. consumer market. The first six months of Donald Trump's presidency clearly show that his hardline stance against U.S. trade partners has yet to deliver meaningful results. At the same time, the noise and posturing surrounding his policies reveal the president's lack of confidence in achieving his goals, which only amplifies the negative market effect of his actions.

Today, attention will shift to producer inflation data, which — unlike consumer inflation — is expected to show a decline year-over-year, though an increase month-over-month. However, due to the nature of Western consumer-driven economies, I believe this report will likely have less impact on the markets than the CPI figures did.

What can be expected in the markets today?

I believe market participants are realizing that the Federal Reserve may hesitate to resume rate cuts due to the uptick in inflation. This should support the U.S. dollar against major currencies. Cautious remarks from Dallas Fed President Lorie Logan on this matter indicate that interest rates may remain unchanged for longer than previously expected. In fact, we can already say that the timeline for rate adjustments is shifting from autumn to late this year.

In such an environment, the U.S. dollar is likely to remain supported regardless of other factors. As for the stock market, it will focus on individual company stories. The cryptocurrency market is likely to remain in a state of consolidation, awaiting a fresh wave of news — the same applies to gold and oil prices.

The pair is undergoing an upward correction after reaching the previous target of 1.1595. It will likely resume its decline toward 1.1530 after a pullback to 1.1635, unless it consolidates above that level. A potential sell level could be around 1.1632.

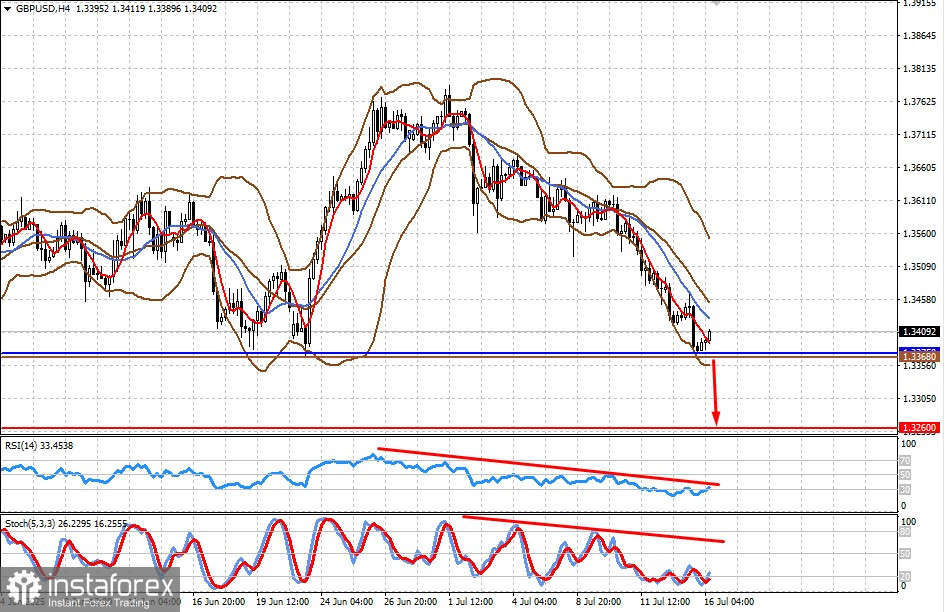

The pair is also correcting upward amid broader U.S. dollar strength. It is likely to reverse downward after a local rebound and drop to 1.3260. A suitable sell level may be 1.3368, provided the price falls below 1.3375.