See also

20.04.2026 09:34 AM

20.04.2026 09:34 AMDon't count your chickens before they hatch. The US equity market is celebrating an end to the Middle East war that looks poised to resume. American forces seized an Iranian tanker in the Strait of Hormuz, despite Tehran's public insistence that the world's main oil artery is open to commercial traffic. The White House takes a different view: the US president has threatened to bomb every bridge and every power plant if a peace agreement is not signed. Did the S&P 500 have reason to celebrate?

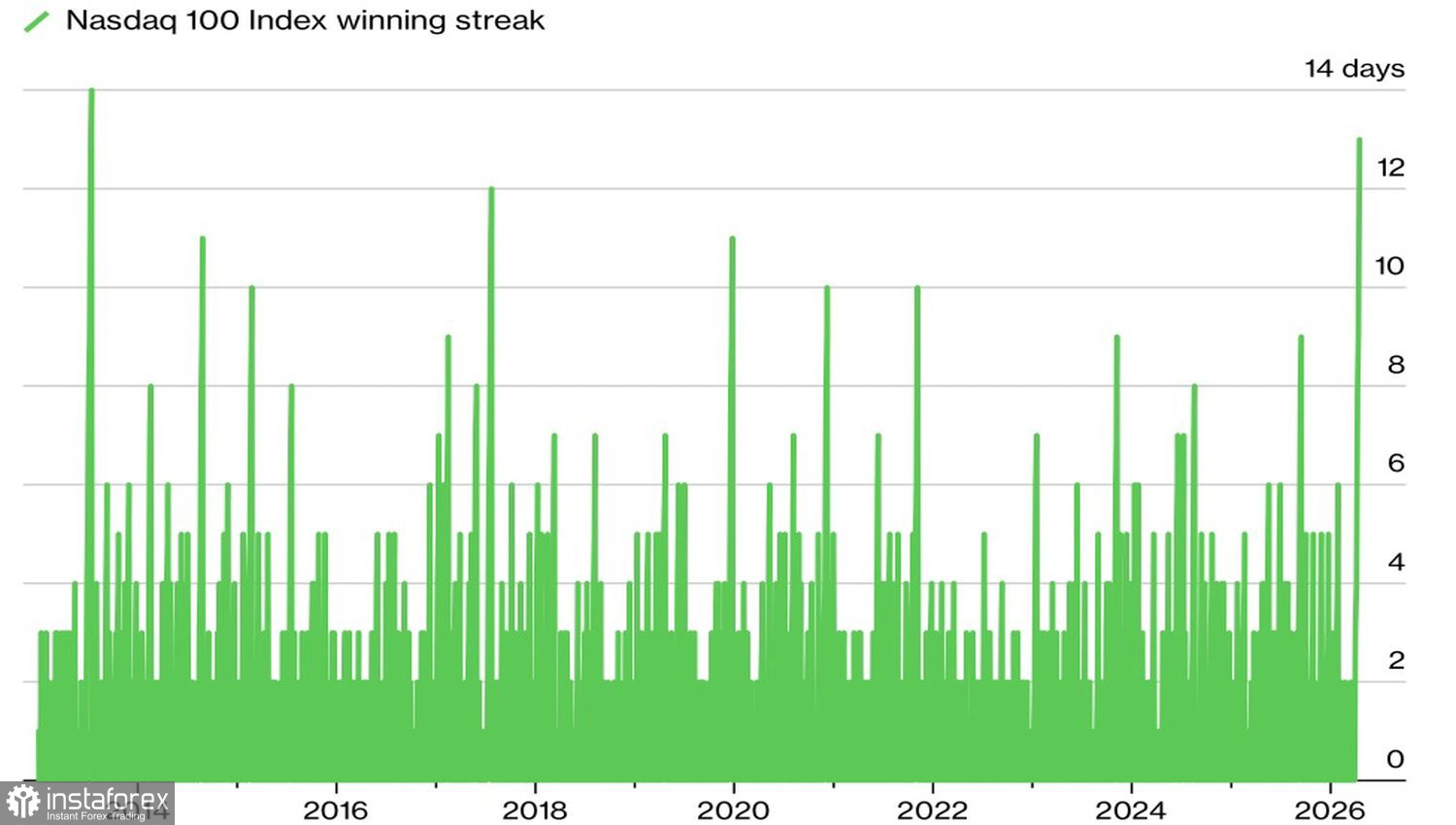

Nasdaq 100 winning streaks

Oil is significantly higher than before the conflict. Treasury yields are higher too. Financial conditions are tighter, yet the broad index has posted record highs for three consecutive days, and the Nasdaq 100 has recorded a 13-day winning streak, the longest such run since 2013. Paradoxical? Bulls argue markets have simply acclimated to this environment. In reality, the rally is driven by FOMO — Fear of Missing Out — which is inherently risky.

Expectations of strong Q1 corporate reports and depressed fundamental valuations — what could be better for buying the S&P 500? At the October peak, the broad index's forward P/E was 23; it has since fallen to 20. The decline in P/E has been even more pronounced for tech names.

Dynamics of tech forward P/E

Typically, falling P/Es are a warning sign — they occur in times of recessions when Wall Street downgrades earnings prospects, and stocks are sold on worries about corporate earnings. By contrast, a rally in price/earnings reflects optimism: earnings expectations rise, stocks become more attractive, buying pushes prices higher.

This time, the P/E contraction reflects a combination of lower prices and upgraded earnings forecasts — mainly for oil & gas issuers and tech corporations. Those groups have been on a roller coaster: the Magnificent Seven fell by about 17% to their March trough and then rebounded by roughly 20%. Microsoft is a case in point: the stock plunged by about 34% from its October peak and later jumped by 19%.

Goldman Sachs argues that for the S&P 500 rally to continue central banks will need to return to the stances they held when the conflict began. In late February, they were still discussing policy easing.

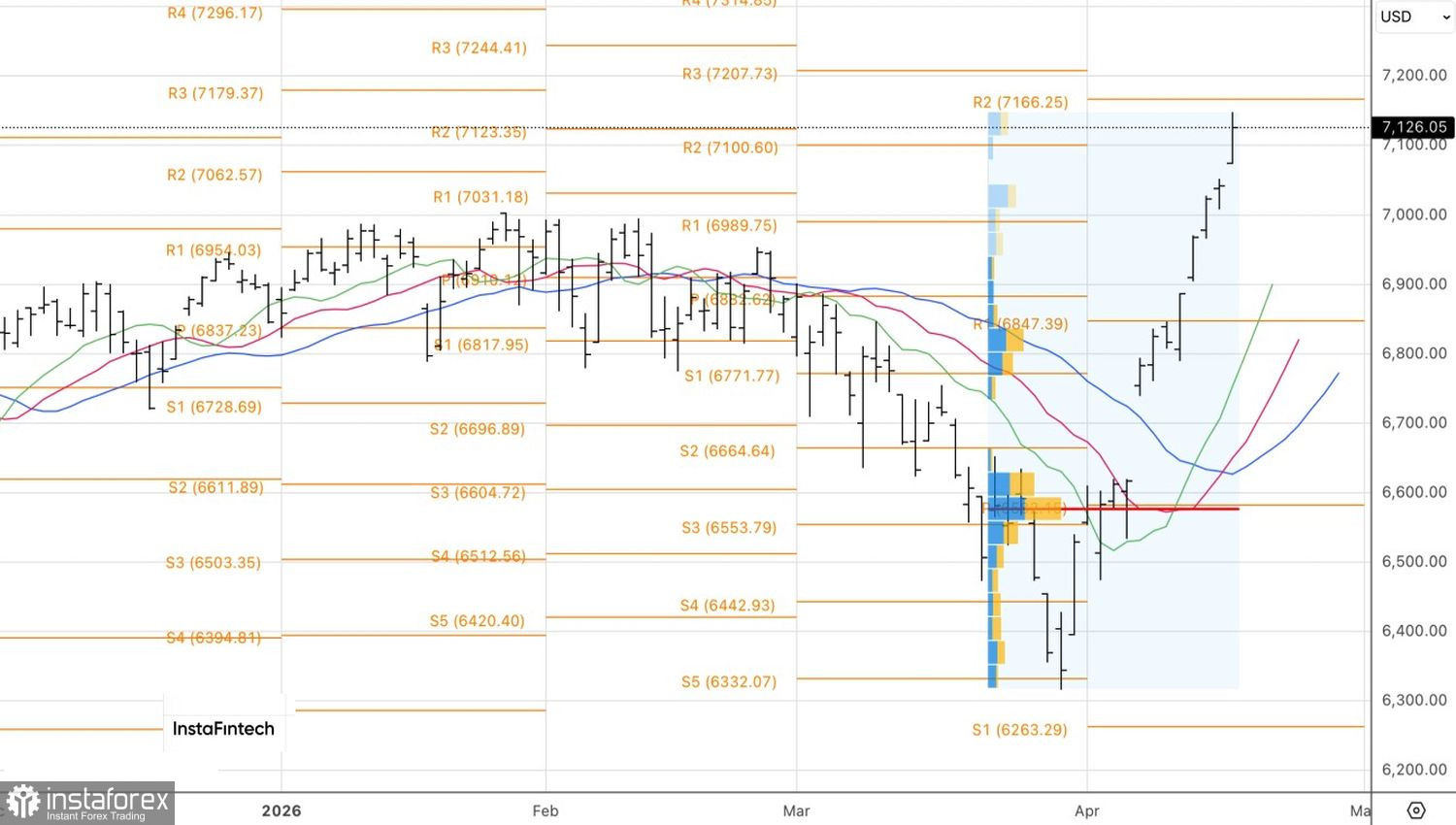

Technically, the daily chart shows that the S&P 500 has hit the first of two previously stated long targets at 7,100 and 7,180, allowing partial profit-taking on longs. Failure by bulls to hold above 7,100 would signal weakness and invite short-term selling.

You have already liked this post today

*The market analysis posted here is meant to increase your awareness, but not to give instructions to make a trade.