यह भी देखें

05.11.2025 12:48 AM

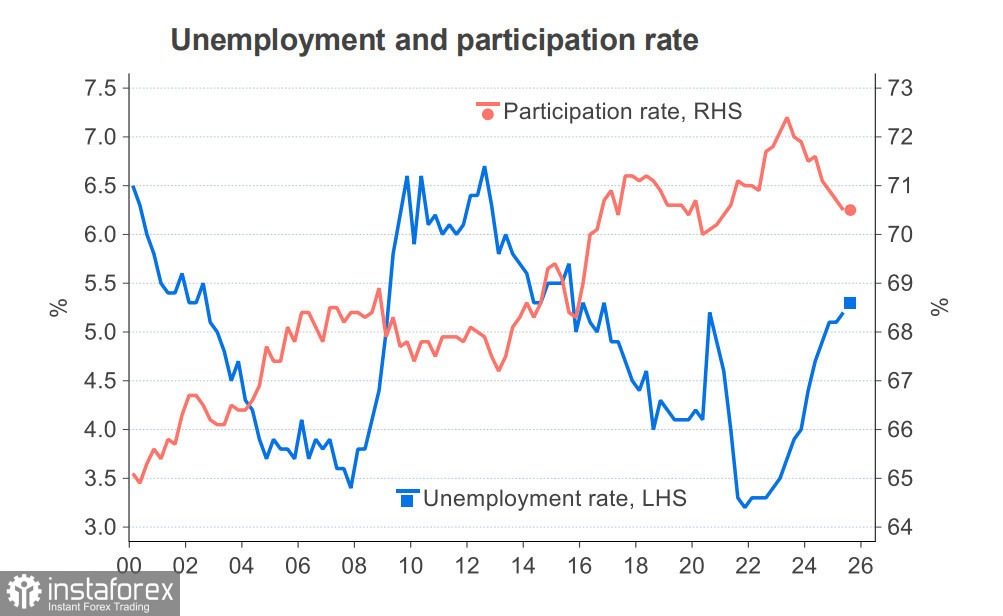

05.11.2025 12:48 AMThe main event for the Kiwi this week will be the third-quarter labor market report. The report is expected to be weak, with unemployment rising from 5.2% to 5.3% if the participation rate remains stable. The dynamics of the average wage will be of particular interest, with a forecasted quarter-on-quarter growth of 0.4%, corresponding to a decline in the annual wage growth rate from 2.3% to 2.1%. If the report is close to forecasts, it will align with the Reserve Bank of New Zealand's expectations and increase pressure on the Kiwi amid the threat of a faster rate cut.

The latest data on the state of the New Zealand economy looks mixed. Consumer confidence has slightly decreased, while ANZ's business confidence index has risen sharply, reaching its highest level since February.

The Kiwi is declining, mainly due to external factors. There was some hope that the RBA would provide a bit of support for the AUD and NZD by refraining from cutting rates on Tuesday morning, but even this expected decision triggered sell-offs. Commodity currencies are being actively sold, despite the fact that the meeting between Trump and Xi allowed some easing of trade tensions.

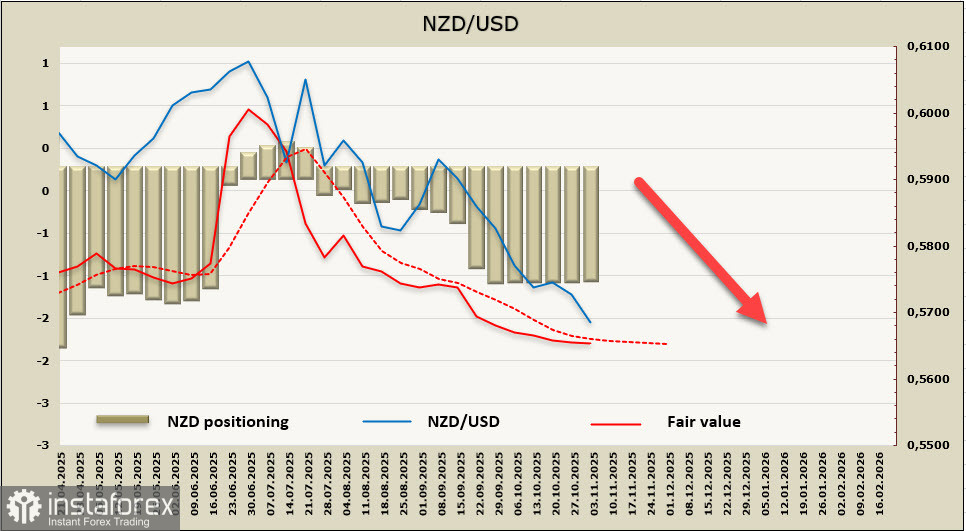

Currently, the RBNZ rate forecast is for a 25 basis point cut at the meeting on November 26, lowering the rate to 2.25%, and these expectations are already fully priced in, but the threat of a 50 basis point cut exerts strong pressure on the Kiwi. It appears that investors are not expecting anything positive from the labor market report, especially since the RBNZ cut rates by 50 basis points in October, indicating a willingness to take such drastic measures. Given this array of factors, the likelihood of escalating pressure on the Kiwi is only increasing.

An additional source of tension is the ongoing US government shutdown, poised to become the longest in history. In any case, risk appetite is diminishing under the current conditions, which does not favor growth in demand for commodity currencies.

The calculated price remains below the long-term average, with no signs of growth, but the downward momentum has also become less pronounced.

After a brief correction, the Kiwi has resumed its decline as we expected and has already reached a six-month low. Concerns that the RBNZ may cut rates by 50 basis points in November, along with the Fed's more hawkish forecasts, provide no reason to anticipate a resumption of growth. There are no significant supports up to the April low at 0.5481, and it is expected that the decline will continue, especially if the labor market report appears weak.