Veja também

06.11.2025 12:51 AM

06.11.2025 12:51 AM

"Like a bolt from a clear sky," "it never happened, and here we are again." Any of the above headlines would fit Tuesday's event in the UK. Early in the morning, the UK Treasury Director Rachel Reeves announced that the Labour Party would have to abandon its promise not to raise taxes. A brief history: in 2024, after Boris Johnson's resignation, Keir Starmer became Prime Minister, winning elections where the Labour Party came to power. For the first time in over 10 years, the Labour Party found itself in power, having to deal with the consequences of the Conservatives' actions, particularly concerning Brexit, its economic and demographic outcomes, the budget deficit, and the loss of trade ties with the European Union.

One might say that the Labour Party has a serious mission to stabilize the country's situation. However, politics does not work that simply. To come to power, the Labour Party promised the electorate not to raise taxes. In November 2025, it became clear that increasing taxes is effectively the only way to form a budget for 2026 without a deficit, without new borrowings, and without increasing government debt. Therefore, the Labour Party must either increase borrowing and debt, which will put even more pressure on the budget due to high interest rates on government bonds, or make unpopular decisions and "forget" their pre-election promises. What trust can the public have in a government that does not fulfill its promises?

Perhaps the Labour Party can reduce the budget deficit without increasing government debt, but in the next elections, the Conservatives may win, as the ruling party's trust may decline sharply. Keir Starmer understands this, as does the entire current Parliament. Therefore, they strive to avoid this scenario by all means.

Consequently, for several months now, Reeves has been on the verge of resignation. Parliament is pondering whether it is better to dismiss Reeves and find another Chancellor who can figure out where to get the money, or to keep Reeves and risk losing the next elections. Reeves has already faced significant criticism for her budget proposal, yet the situation has not changed in recent months, and she has not come up with anything better.

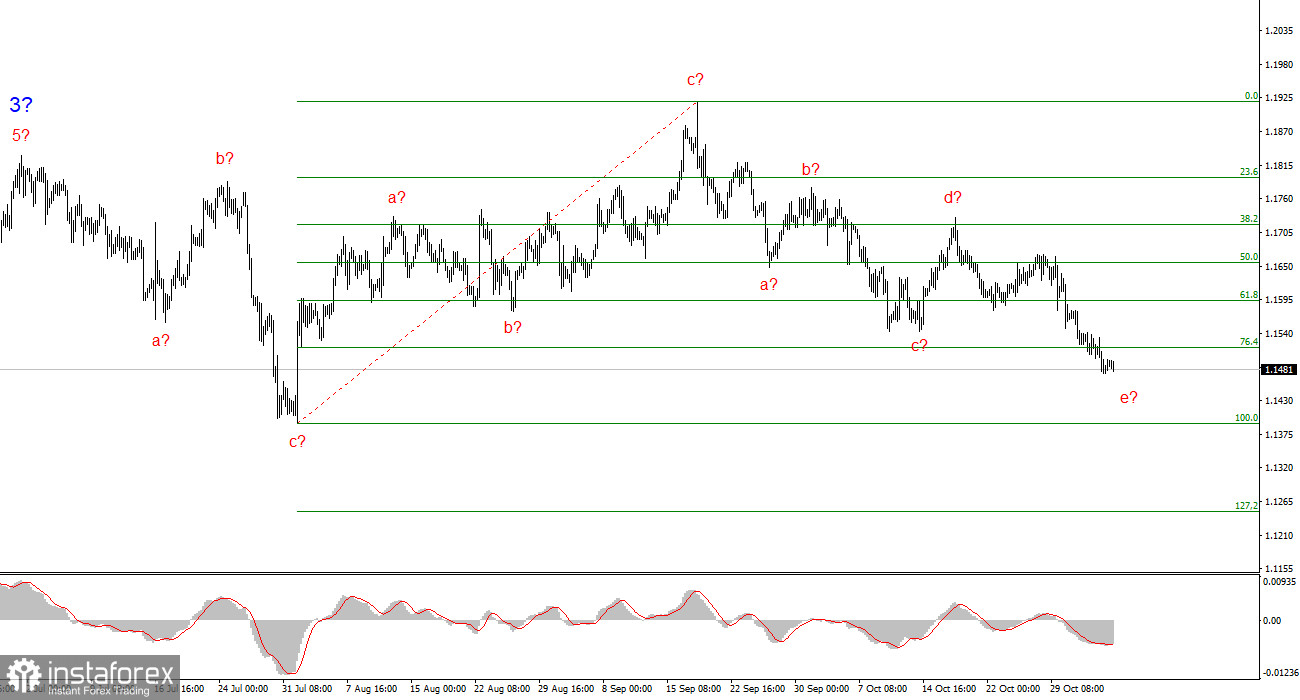

Based on the analysis of EUR/USD, the instrument continues to build an upward trend segment. Currently, the market is in a pause, but Donald Trump's policies and the Fed's remain significant factors in the future decline of the U.S. dollar. The goals of the current trend segment may reach the 25-figure mark. At this time, we can observe the formation of corrective wave 4, which is taking a highly complex, elongated form. Therefore, in the near future, I will still consider only buying, as any downward structures appear to be corrective. The latest structure, a-b-c-d-e, might be nearing its completion.

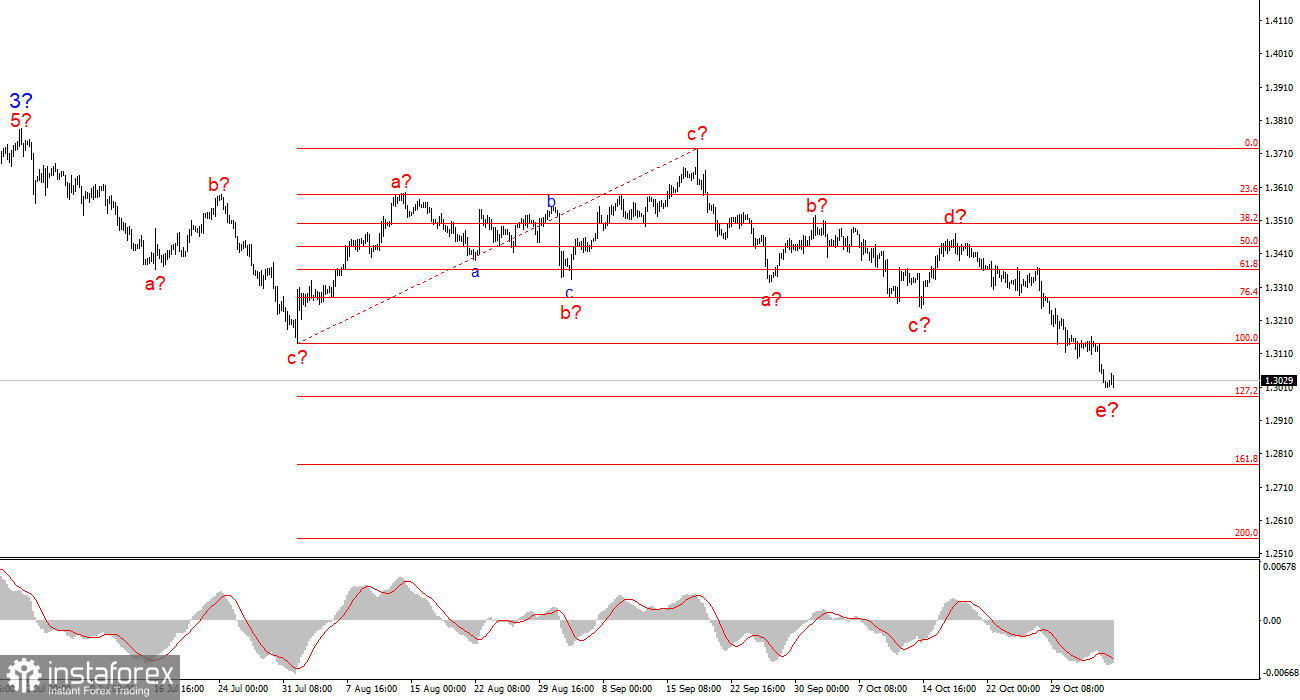

The wave picture for the GBP/USD instrument has changed. We still deal with an upward, impulsive segment of the trend, but its internal wave structure is becoming more complex. Wave 4 is taking on a three-wave form, and its structure is significantly longer than that of wave 2. Another downward corrective structure is approaching completion. I continue to anticipate when the main wave structure will resume its formation with initial targets around the 38 and 40-figure levels, and I believe this could happen as early as the beginning of November.