Vea también

22.07.2025 10:14 AM

22.07.2025 10:14 AMAs August 1 approaches—the date previously announced by Donald Trump for the imposition of tariffs against U.S. trading partners—market participants are becoming increasingly focused on this issue, exercising caution.

The topic of the consequences of the actual trade restrictions imposed by the U.S. President on partner countries is once again in the spotlight and remains a key factor influencing asset price movements. An additional and significant factor is the controversy stirred up by the Trump administration surrounding Federal Reserve Chair Jerome Powell. He is being accused of misallocating funds, but this appears to be merely a pretext to replace him with someone more personally loyal to Trump at the helm of the central bank. It's worth recalling that throughout his six-month presidency, Trump repeatedly urged Powell to lower interest rates to stimulate economic growth. However, Powell consistently rejected these appeals, citing high inflation and the unpredictable consequences of Trump's trade wars.

This creates a fairly tense environment for financial markets—regardless of asset class or geographic location. The only apparent beneficiary of this situation is the stock market, which continues to receive support amid the still-balanced state of the U.S. economy, which has so far avoided slipping into a full-scale recession. Support may also come from the prospect of replacing Powell with a pro-Trump candidate who would pursue rate cuts even though consumer inflation is still far from the 2% target—currently standing at 2.7%.

What can be expected in the markets by the end of this month?

The ongoing tension created by Trump's actions is likely to cause sharp moves in asset prices. The uncertainty surrounding how U.S. trading partners might respond, or whether they will respond at all, remains high. Leaked rumors or headlines related to this issue may trigger strong local price swings, possibly followed by equally sharp corrections.

For market participants, what matters is not only whether agreements are reached, but also the broader implications of those agreements. Based on this, I believe the markets will remain consolidated within narrow ranges for the remainder of the month. Only real insider information—rather than rumors—can trigger a decisive market move and end the consolidation phase.

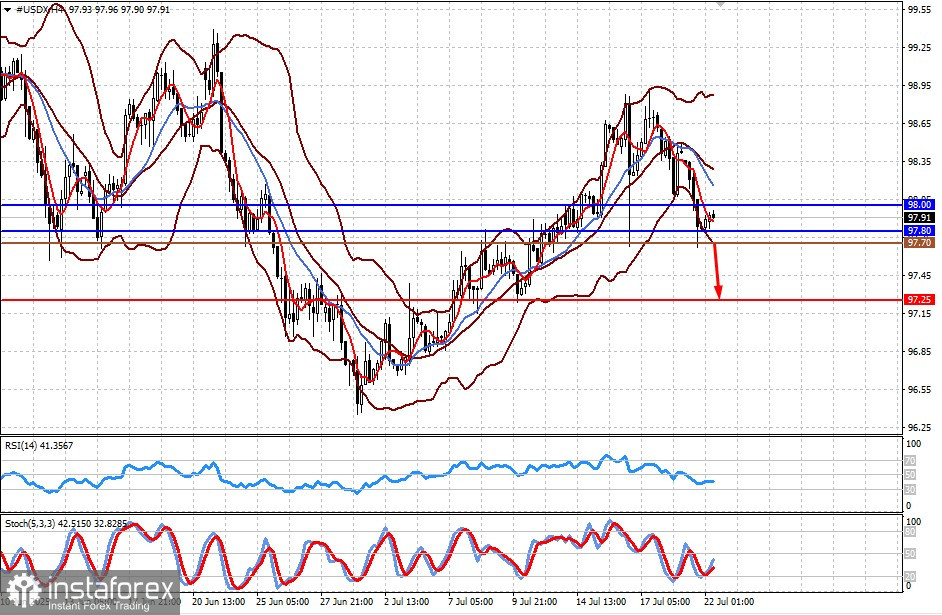

The U.S. Dollar Index remains stuck between two strong levels: resistance at 98.00 and support at 97.80. The continued pressure on the dollar, stemming from uncertainty over the upcoming U.S. tariff implementation on August 1, is likely to weigh further on the currency. A drop below 97.80 could lead to a decline toward 97.25. A possible sell level is 97.70.

The pair is showing a local reversal due to dollar weakness, which could lead to further downside toward the 38% Fibonacci retracement level. If the pair fails to rise above 148.00, a decline toward 146.70 is expected. A potential sell level is 147.54.