আরও দেখুন

21.08.2025 12:51 AM

21.08.2025 12:51 AM

The answer to this question is clear and straightforward. The higher the inflation rises, the lower the Bank of England's willingness to continue easing monetary policy. The less inclined the BoE is to cut interest rates, the higher the probability of further growth in the British pound. At present, the BoE's rate stands at 4%, while the Fed's is at 4.5%. The BoE has carried out three rounds of policy easing in 2025, while the Federal Reserve has done none. Multiple Fed rate cuts are on the horizon, while a BoE cut is now in serious doubt. Demand for the U.S. dollar fell in 2025 even when the rate differential between the two central banks was clearly in the dollar's favor. What should we expect if the picture begins to shift in the opposite direction?

The main advantage for the pound in the next year and a half will be the independence of the BoE. Yes, precisely the independence of the British central bank, not the size of its rate or the state of the economy. The BoE can make decisions independently, according to its mandates. The probability that the Fed will continue to act independently is decreasing with each month. Within the Fed, there are already several Trump supporters actively lobbying for rate cuts. In addition, some FOMC officials are gradually "packing their bags," realizing that from now on the Fed is "Trump's toy." One FOMC member (Adriana Kugler) has already left her post early. Jerome Powell will leave next year, while Donald Trump continues to press hard for rate cuts of several percentage points.

Therefore, the Fed's monetary policy outlook remains dovish. And for the first time in years, markets have solid grounds to expect a major rate cut based on one very concrete reason. Meanwhile, rising inflation in the UK makes further policy easing there virtually impossible—or at least impractical. Hence, I can assume that the British central bank will slow or halt its easing cycle, while the Fed will resume and accelerate it.

From this, it is easy to conclude that in the next year to year and a half, demand for the U.S. dollar will continue to decline. Of course, monetary policy is not the only factor influencing the FX market. But it is a significant one, and it cannot be ignored.

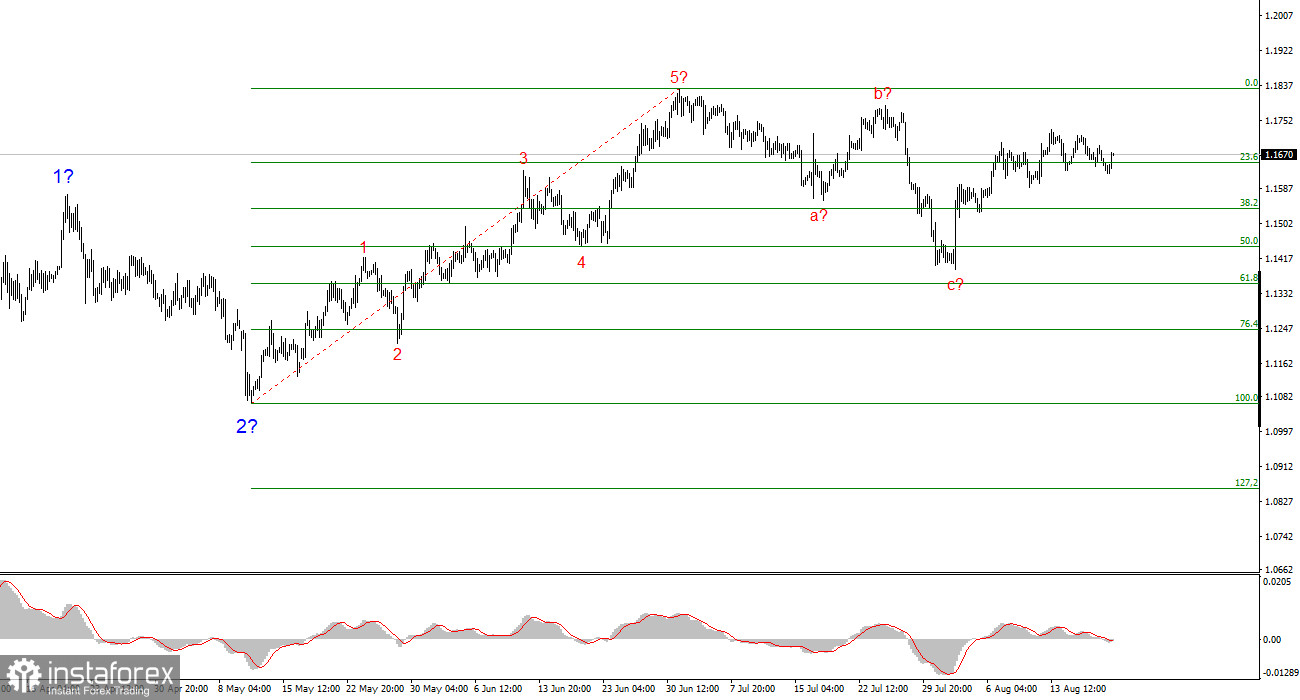

Based on the analysis of EUR/USD, I conclude that the instrument continues to form an upward section of the trend. The wave structure still entirely depends on the news background related to Trump's decisions and U.S. foreign policy. Targets for this trend section may extend up to the 1.25 area. Accordingly, I continue to consider buying positions with targets near 1.1875, which corresponds to the 161.8% Fibonacci level, and higher. I assume that the formation of wave 4 has been completed. Therefore, it is still a good time for buying.

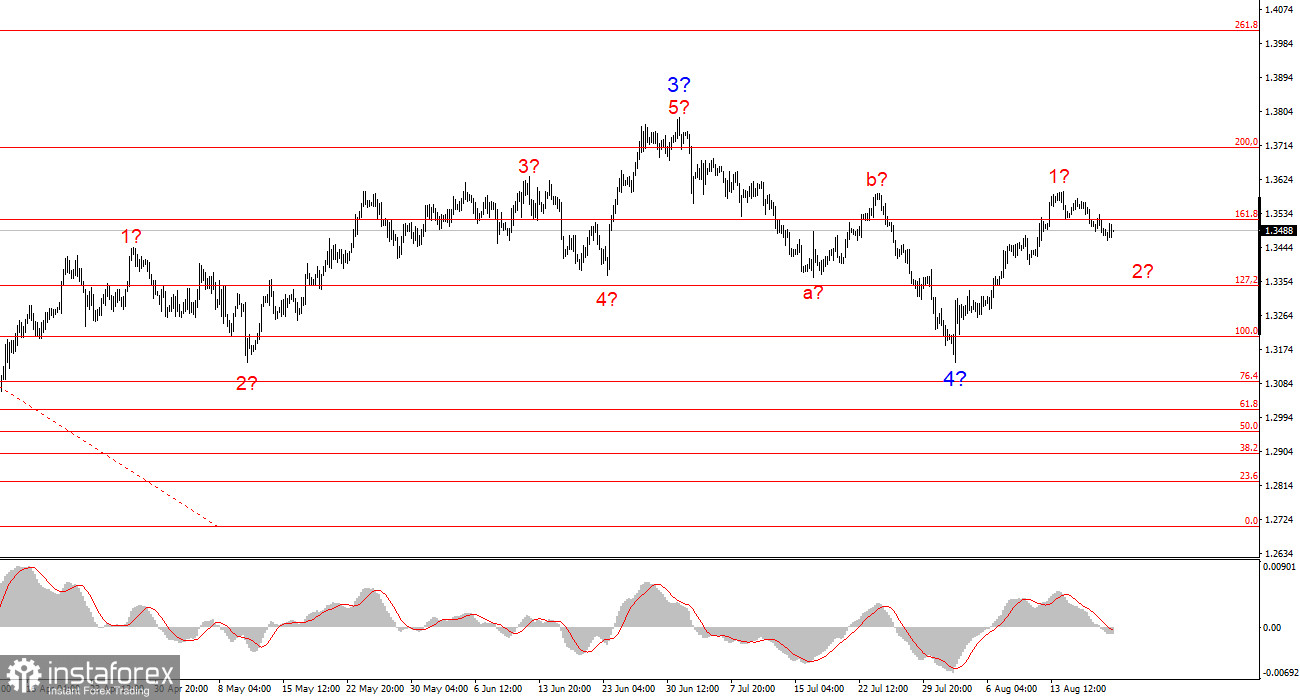

The wave structure of GBP/USD remains unchanged. We are dealing with an upward, impulsive section of the trend. Under Trump, the markets may face many more shocks and reversals, which could significantly affect the wave structure, but for now, the working scenario remains intact. Targets for the upward section of the trend are now located near 1.4017. At present, I assume that the formation of downward wave 4 has been completed. Therefore, I recommend buying with a target of 1.4017.