See also

16.06.2025 07:36 PM

16.06.2025 07:36 PMThe macroeconomic data from the UK published last week looks frankly weak—everything is in the red zone, meaning worse than expected. Nevertheless, the pound continues to climb upward regardless.

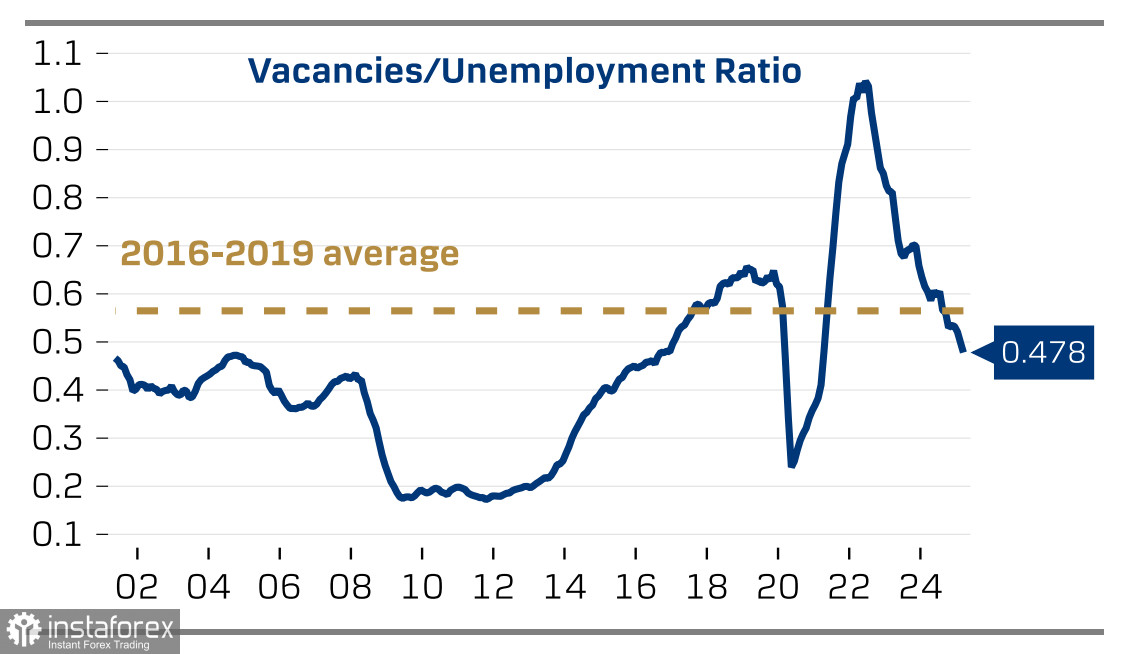

The labor market report came in noticeably worse than expected—the number of jobless claims surged sharply (+33.1K in May versus -21.2K in April), and the ratio of vacancies to the unemployment rate is rapidly declining, now worse than pre-COVID levels. Average wage growth fell short of forecasts, which typically leads to a weaker currency since it indirectly signals a potential slowdown in inflation. But not this time—the pound seemed to ignore the weak data and continued its determined upward move.

The trade balance worsened in April, monthly GDP growth came in at -0.3% (i.e., negative), service sector activity slowed, and industrial production data for April was also in the red. The market may not be interpreting these indicators as a sign of economic weakness, perhaps viewing them as a temporary response to the new trade policy introduced by Trump. The chance that the UK will be able to "strike a deal" appears higher than for China, Mexico, or the EU, and thus the situation might normalize soon. Whether that's the case or not, as usual, time will tell. For now, the main focus remains on high inflation. The market needs to see signs of its slowdown before revising interest rate forecasts.

The Bank of England will hold its monetary policy meeting on Thursday, June 19. Market expectations are neutral, with the rate projected to remain unchanged at 4.25%. This meeting is considered uneventful, as no updated forecasts will be presented and no press conference will follow the statement.

The main risk lies in the vote distribution. The current forecast is 7 votes for no change and 2 votes for a rate cut. However, if more members vote for a cut—3 or 4—the market will interpret this as dovish, and the pound will likely react with a decline. Otherwise, the reaction will be neutral or even slightly positive.

If anything has changed since the last meeting in May, it has been for the worse—the labor market appears weaker, wage growth is below expectations, and GDP growth is also slower. At this point, the market expects a 50 basis point rate cut by the end of the year, with the December rate projected at 3.7%, and this forecast is already priced in.

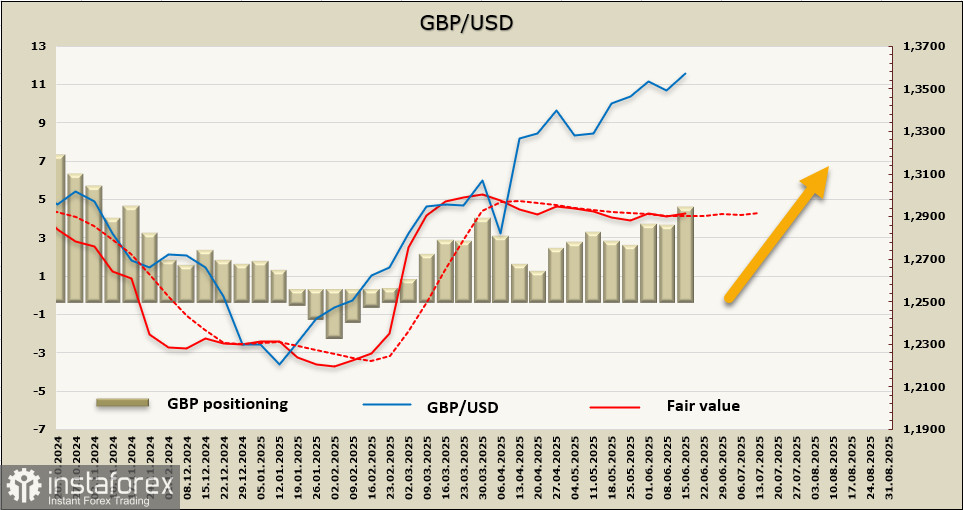

The net long position on GBP increased by 1.4 billion over the reporting week, reaching 4.4 billion. At the same time, the estimated price has not been able to break away from the long-term average. This is mainly due to the underperformance of the UK government bond yield curve compared to US Treasuries.

The week before, we noted that the chances of a bullish impulse had increased and set a target at 1.3650. Over the past period, the pound has approached that level closely. We assume there will be an attempt to break above the resistance, but the chances of a continued move look unconvincing for now, and a correction is more likely. We see support at 1.3443, and there is a good chance the pound will remain above it, but there is currently no strong basis for a major upward surge—unless, of course, the Bank of England provides one on Thursday.