See also

27.06.2025 12:21 PM

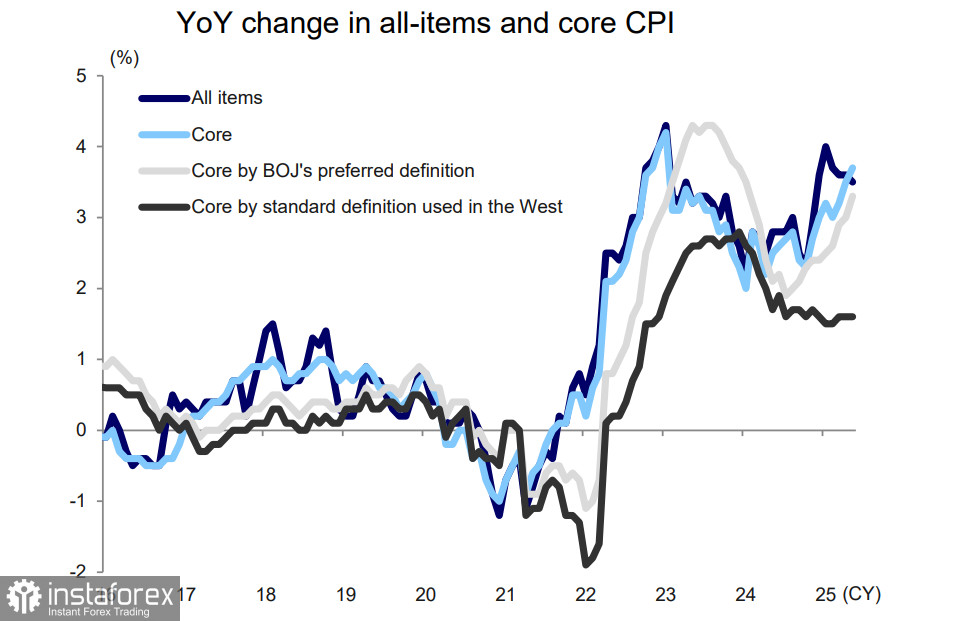

27.06.2025 12:21 PMThe Consumer Price Index (CPI) in the Tokyo region declined in June from 3.4% to 3.1% year-over-year, marking the first signal so far that may indicate a slowdown in price growth. Nevertheless, the Bank of Japan is unlikely to take it into account and will instead wait for the nationwide CPI, which still remains uncomfortably high for a country that had hovered on the edge of deflation for decades.

A week earlier, inflation data for May was released, and it showed no signs of a slowdown. The overall index dropped slightly from 3.6% to 3.5% y/y, while the core index—excluding food and used by the Bank of Japan as the main gauge of price dynamics—rose from 3.5% to 3.7% y/y.

All key inflation indicators in Japan have been above the BoJ's target for over three years, yet the central bank only abandoned negative interest rates in April last year and has raised the rate by just 60 basis points since then. At its most recent meeting in June, the BoJ once again kept the rate unchanged, suggesting that core inflation would "remain subdued" due to the economic slowdown.

As we can see, inflation is far from subdued and is instead continuing to grow steadily. Half of this growth stems from a single product—rice—which is a staple for Japanese households. Rice prices surged by 101% in May, marking the biggest price jump in over half a century. The BoJ may consider this spike temporary and expect prices to come down, which would ease inflationary pressure. However, one thing is clear: the BoJ is not meeting the expectations of investors who had counted on a more aggressive rate hike trajectory and a stronger yen. At the beginning of the year, there were numerous forecasts that USD/JPY could fall to 130 or even 120—but now, that confidence has largely vanished.

Another source of disappointment stems from the tariff dispute with the United States. Japan previously agreed to increase LNG purchases from the U.S. as part of efforts to reduce its trade deficit, expecting in return that the U.S. would make concessions on a key issue—automobile tariffs. However, Japan's attempts to reach an agreement with the U.S. during the G7 summit yielded no results. U.S. Trade Representative Lutnik took a tougher stance, stating that automobiles are the main reason for the U.S. trade deficit with Japan, and therefore no concessions would be made.

The inevitable worsening of Japan's trade balance, the likely increase in its budget deficit, and the economic slowdown due to reduced exports will put pressure on the Bank of Japan. The central bank will be forced to look for unconventional solutions to stimulate the economy while avoiding further inflation. This outlook is clearly dampening the bullish sentiment toward the yen.

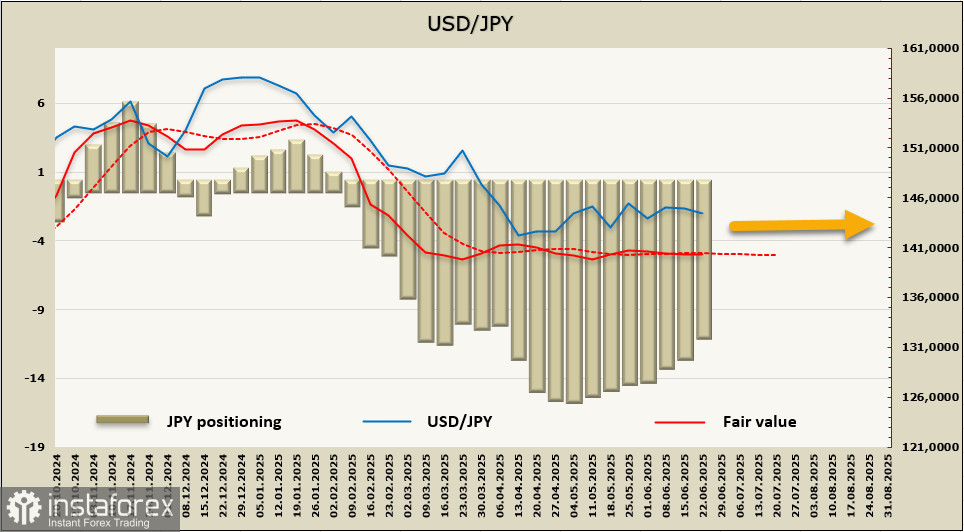

The net long position on the yen continues to shrink. The reporting week brought another -1.216 billion, reducing the overall bullish balance to +11.26 billion. The accumulated speculative long position remains substantial—second only to the euro among major currencies—but the trend over the past seven weeks signals investor disappointment, as they appear to no longer expect decisive action from the Bank of Japan.

USD/JPY continues to trade within a sideways range, with the daily chart increasingly resembling a narrowing triangle. A breakout is inevitable, but the previously assumed direction—downward toward the 127–129 level—is now far less certain. Even the weakness of the U.S. dollar isn't helping the yen, as the BoJ's pause drags on. At this point, all that remains is to wait for a catalyst that could give the yen a clear direction. For now, the pair remains range-bound with no evident trend.