यह भी देखें

04.07.2025 12:47 PM

04.07.2025 12:47 PM

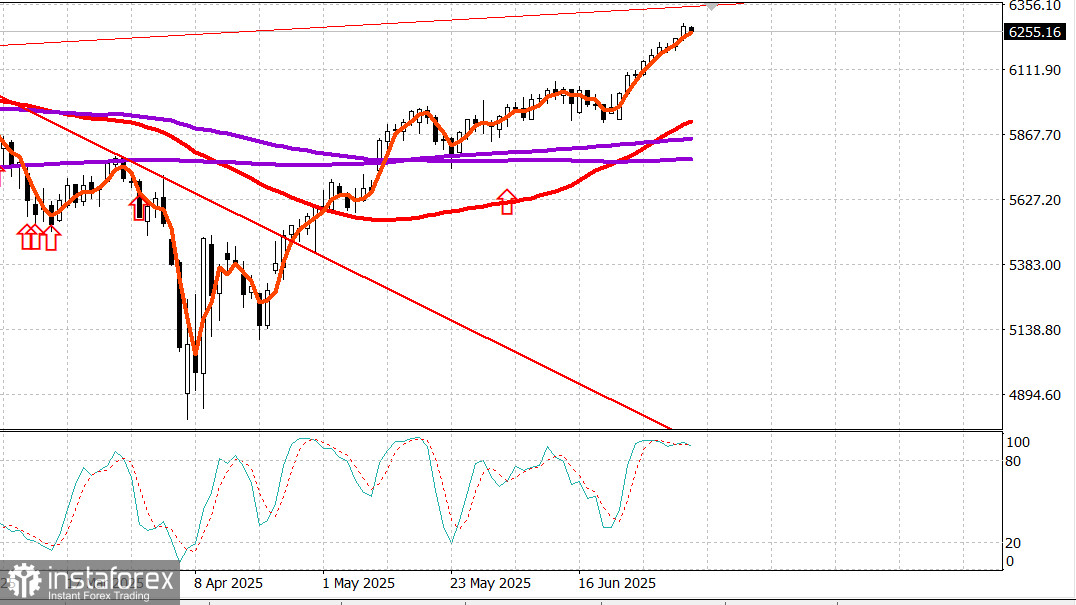

S&P500

Snapshot of major US stock indices on Thursday:

US financial markets are closed on Friday for the Independence Day holiday.

The stock market opened higher Thursday after a better-than-expected June NFPs report was released just before the open, and maintained that momentum throughout the session. Both the S&P 500 (+0.8%) and the NASDAQ Composite (+1.0%) closed at fresh record highs.

Stock futures had been relatively steady in anticipation of the report, but surged after data showed a decline in unemployment, fewer initial jobless claims, and a rise in employment.

The US nonfarm payrolls showed some weaknesses, including:

However, markets largely ignored the negative details and rallied to new highs during the session.

Stronger-than-expected labor data dampened hopes for a July rate cut. According to the CME FedWatch Tool, the market now sees just a 4.7% probability of a 25 basis point rate cut at the July FOMC meeting, down from 23.8% the day before.

Atlanta Fed President Raphael Bostic (a non-voting FOMC member) told CNBC the U.S. economy could still face prolonged inflation pressures due to tariffs. He supports the Fed's "wait and see" approach and noted that while the labor market remains strong, hiring has slowed.

Bond yields remained elevated, reflecting solid economic data and reduced expectations for rate cuts:

10-year Treasury yield: +5 bps to 4.35%

2-year yield: +10 bps to 3.89%

The stock market showed resilience, with all 10 sectors finishing higher. Advancers outpaced decliners by more than 2 to 1 across both exchanges.

Tech led the gains (+1.1%) following news that the Trump administration lifted restrictions on exporting chip design software to China. This boosted chip design firms:

Synopsys (SNPS): +4.6% to $547.00

Cadence Design (CDNS): +5.2% to $327.00

Strong tech performance supported large-cap strength overall, with the Vanguard Mega Cap Index (+1.1%) outperforming the S&P 500 for a second straight day.

Year-to-date performance:

Economic calendar

June Nonfarm Payrolls: +147K (consensus: 120K) Previous revised from 139K to 144K

Private Sector Payrolls: +74K (consensus: 123K) Previous revised from 140K to 137K

Unemployment Rate: 4.1% (consensus: 4.2%)

Average Hourly Earnings: +0.2% (consensus: +0.3%) Previous: +0.4%

Average Workweek: 34.2 hours (consensus: 34.3) Previous: 34.3

Bottom line The report was not weak enough to convince the market that a July rate cut is likely. On the contrary, it now seems highly unlikely, with rate cut odds falling to 4.7%.

Other key economic data

May Trade Deficit: -$71.5B (consensus: -$70.5B) Prior revised from -$61.6B to -$60.3B Negative contribution expected to Q2 GDP from net exports

Weekly Initial Jobless Claims: 233K (consensus: 240K) Prior revised from 236K to 237K

Weekly Continuing Claims: 1.964M (unchanged after revision) Companies are not laying off workers rapidly, but rehiring is becoming more difficult.

S&P Global US Services PMI (Final, June): 52.9 (previous: 53.7)

May Factory Orders: +8.2% (consensus: +7.9%) Previous revised down to -3.9% Business spending rebounded sharply, reflecting post-tariff pause recovery

ISM Services PMI (June): 50.8% (consensus: 50.3%) Previous: 49.9% Indicates a modest return to growth in services; input prices slightly declined, a modest but positive shift.

Energy market

Brent crude is now trading at $68.40 a barrel, unchanged on the day. Oil faces strong resistance near $70.

Conclusion

The US stock market entered the long Independence Day weekend at new all-time highs. The rally is likely to continue, though possibly after a normal pullback or consolidation phase.