Lihat juga

03.07.2025 01:15 PM

03.07.2025 01:15 PM

S&P500

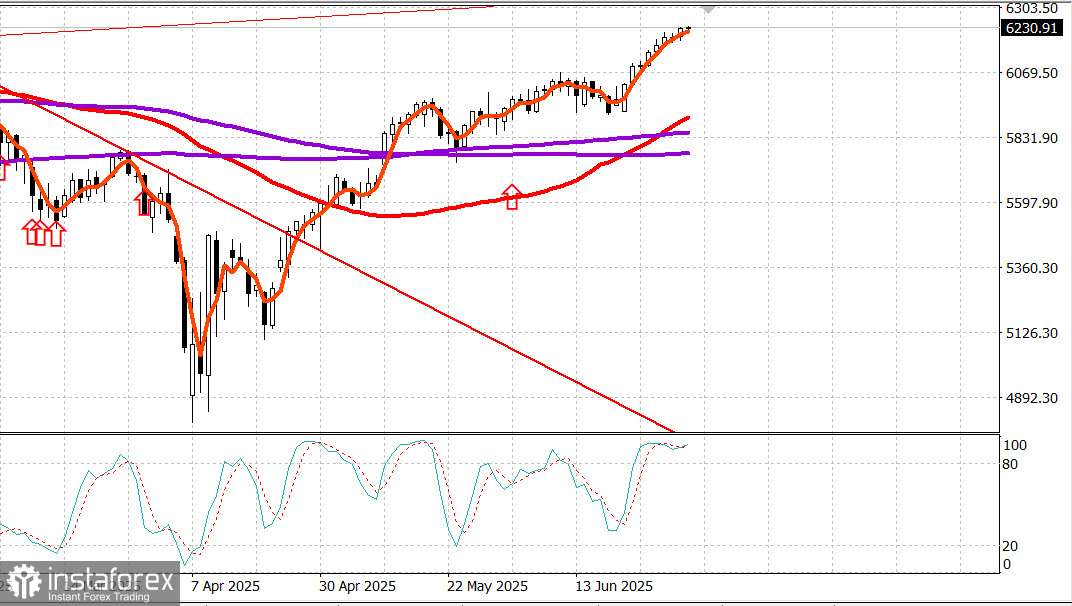

Snapshot of major US stock indices on Wednesday: * Dow: +0.0% * NASDAQ: +0.9% * S&P 500: +0.5% * S&P 500 closed at 6,227, trading within a range of 5,700 – 6,300.

The S&P 500 closed at a new all-time high yesterday, showing steady gains throughout the session despite a disappointing ADP employment report, which showed a loss of 33,000 private sector jobs in June.

This negative news was overshadowed by President Trump's announcement of a trade deal with Vietnam, which includes zero tariffs for U.S. access to Vietnamese markets, strong performance by several large-cap stocks, and continued leadership from small- and mid-cap equities.

Tesla (TSLA 315.65, +14.94, +4.97%) reported better-than-expected Q2 sales figures. Apple's rating (AAPL 212.44, +4.62, +2.22%) was upgraded by Jefferies from "underperform" to "hold." NVIDIA (NVDA 157.25, +3.95, +2.58%) and Alphabet (GOOG 179.76, +2.85, +1.61%), both benefiting from AI-driven momentum, were among the top mega-cap performers.

Their influence boosted the market-cap weighted S&P 500 (+0.5%), which posted solid growth, though it once again underperformed the Russell 2000 (+1.3%) and the S&P MidCap 400 (+1.0%), both of which continued to benefit from rotation into smaller-cap names.

As with the previous day, buying interest was broad-based.

Advancing stocks outpaced decliners by more than 2-to-1 on both the NYSE and Nasdaq.

Notably missing from the gainers was health insurer Centene (CNC 33.78, -22.86, -40.37%), which plummeted after withdrawing its guidance following an initial market analysis for 2025 from Wakely. Other health insurance stocks also traded lower, driving the healthcare sector down by 1.0%.

The financial sector (-0.1%) also lagged the broader market, despite several major US banks announcing plans to increase dividends and/or initiate share buybacks following the Fed's annual stress test results.

Top-performing sectors of the day were:

Returning to the ADP report, while disappointing, investors refrained from overreacting, recognizing that a more comprehensive view of the labor market would come with the official June employment report, due before Thursday's open. Additionally, ADP data often does not align closely with government figures.

On the political front, the "One Big, Beautiful Bill" remains in the House of Representatives, with reports suggesting internal disagreements within the Republican party over the bill's cost, potentially delaying its passage. However, the general expectation is that it will eventually pass, even if not by President Trump's desired July 4 deadline.

Reminder: The stock market will close early at 1:00 PM ET on Thursday in observance of Independence Day on Friday.

Year-to-date performance:

Energy market Brent crude is now trading at $68.60, up around $1 over the past day, hot on the trail of the US stock.

Conclusion The US market has shown strong growth from April lows. We've locked in solid profits and are now waiting for a healthy correction to open up new buying opportunities.