یہ بھی دیکھیں

27.06.2025 11:16 AM

27.06.2025 11:16 AMInflation in Canada remains too high to expect a rate cut by the Bank of Canada at its upcoming meeting.

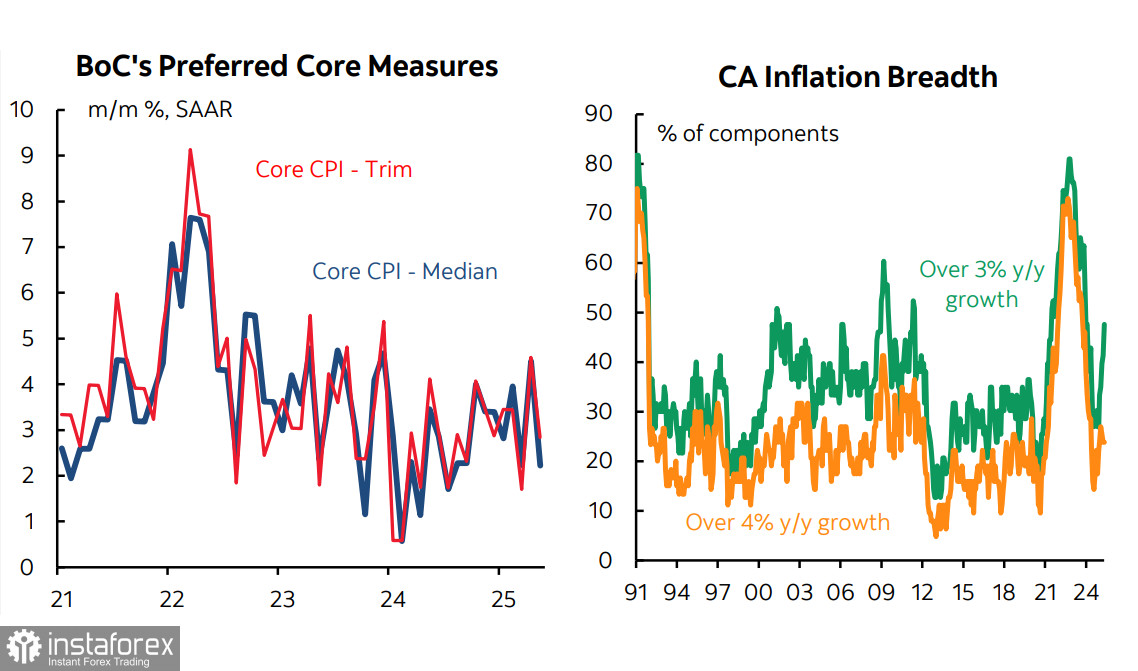

In April, inflation sharply slowed to 1.7% y/y, and most analysts believed it would drop further to 1.5% in May. However, that did not happen—both the headline and core indices remained at April levels. Core inflation is still holding above 2.5% y/y, which is too high to support a rate cut.

The Bank of Canada began its easing cycle in June last year and lowered the rate to 2.75%. However, it held the rate unchanged at its last two meetings. It is now likely that it will be forced to do so again in July, which is clearly a bullish signal for the Canadian dollar. After two consecutive pauses, markets had leaned toward a rate cut and anticipated a slowdown in inflation, which had already been priced in. Now, the inflation factor will continue to push USD/CAD lower.

Bank of Canada Governor Tiff Macklem, in his speech to the St. John's Chamber of Commerce on Wednesday, described the current inflation picture as "complicated." According to him, the recent "persistence" of core inflation may be an early sign of the impact of the trade war with the U.S. on price levels. The logic is straightforward—higher tariffs eventually affect the end consumer, leading to price increases for food and essential goods, particularly since Canada imposed retaliatory tariffs on these categories.

Macklem also noted that tax-adjusted inflation in April was 2.3%, which is above the central bank's expectations. All of this points to the likelihood that the BoC will refrain from cutting rates, and the inflation factor will continue to pressure USD/CAD downward.

As for news from the U.S., it remains mixed. Durable goods orders rose 16.6% in May after a 6.6% drop in April, significantly exceeding forecasts and generally favoring a stronger dollar, as it signals robust consumer demand. However, the revised U.S. GDP data for Q1 showed a decline from -0.2% to -0.5%. The U.S. Commerce Department attributes this drop to a sharp rise in imports, as consumers rushed to buy goods before tariffs pushed prices higher. Imports surged by 37.9%—the fastest pace since 2020—reducing GDP by nearly 4.7 percentage points.

The term "stagflation"—a recession accompanied by rising inflation—is increasingly used in assessments of the current state of the U.S. economy. While Fed Chair Jerome Powell insists this is not the baseline scenario, the mere fact that it is being discussed suggests the Fed is considering this possibility. Such an outcome would be among the worst-case scenarios for the U.S. economy and would inevitably exert strong downward pressure on the dollar.

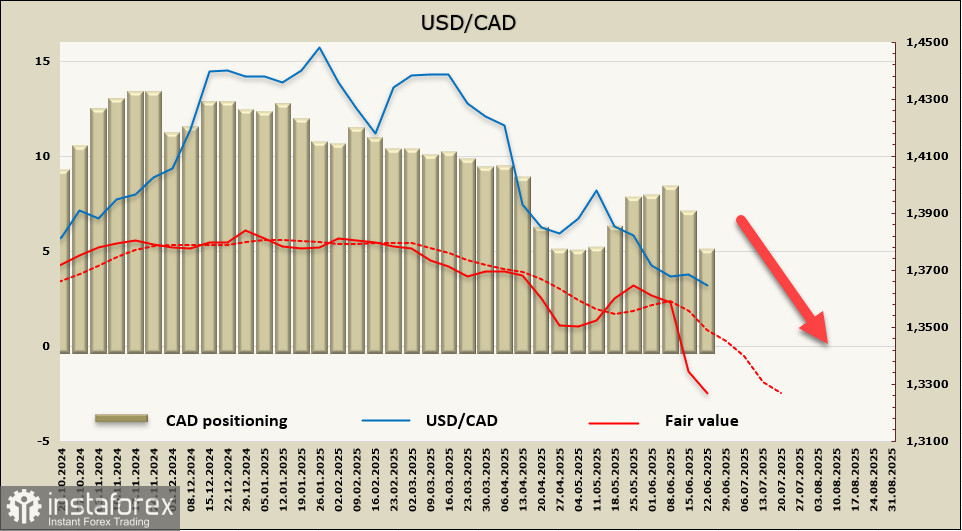

The net short position in CAD shrank significantly over the past reporting week—by 1.964 billion to -4.85 billion. Speculative positioning remains bearish, but the trend toward reduced short exposure is clear and has yet to slow. The fair value is below the long-term average and continues to trend confidently lower.

The Canadian dollar made a minor correction last week and resumed strengthening on Monday. We expect USD/CAD to continue its decline, with the next target being a firm break below 1.3539, followed by support in the 1.3410–1.3430 level. On the daily chart, the pair has not yet entered oversold territory, so there is still downside potential. The fundamental weakness of the U.S. dollar, coupled with the threat of renewed inflationary pressures in Canada, will support further USD/CAD weakening.