یہ بھی دیکھیں

14.07.2025 02:53 PM

14.07.2025 02:53 PM

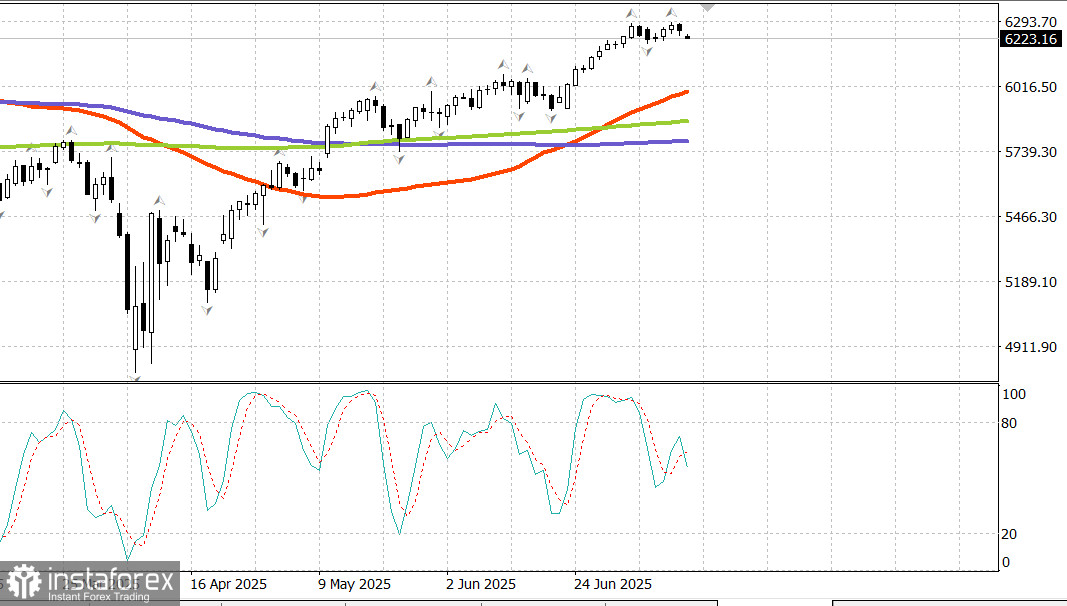

S&P500

Snapshot of US major stock indices on Friday

The announcement of a 35% tariff on Canadian imports, a hint at a 30% tariff for the EU, and the President's statement that most trade partners will face tariffs of 15%–20% triggered the worst market opening on Friday.

However, the initial wave of selling didn't continue. Large-cap stocks led a rebound from the morning lows, helping the indices settle into a sideways trend that lasted most of the session.

Overall, the market remained relatively unfazed by the tariff headlines over the past week. Yes, there were sessions with early profit-taking, but they often came after strong closes.

The weak start reflected the recognition that Canada and the EU are more economically significant trade partners than many of the countries recently targeted with tariff notices. Still, the market maintained resilience, consistent with the week's broader trend.

The recovery from early lows was largely driven by large-cap names overcoming a poor start, including NVIDIA, which saw an intraday gain of +1.3% (NVDA 164.88, +0.78, +0.5%).

Support also came from Amazon (AMZN 225.02, +2.76, +1.2%) and Tesla (TSLA 313.51, +3.64, +1.2%), helping the consumer discretionary sector (+0.3%) close in positive territory — one of only two sectors to finish in the green.

That said, large caps didn't dominate across the board: the Vanguard Mega Cap Growth ETF (-0.2%) only slightly outperformed the S&P 500 (-0.3%). Losses were broad-based across company sizes and most sectors, with energy (+0.4%) being the only sector where the majority of components rose.

Tariff headlines ultimately led to broad profit-taking, as markets looked ahead to key economic data scheduled for next week, including June CPI, PPI, and retail sales reports, as well as earnings from many major US banks.

Treasury market US Treasury bonds were under pressure all day Friday as tariff concerns weighed on sentiment from the open. The long end of the yield curve, which is more sensitive to inflation expectations, performed the worst, resulting in a steeper curve by week's end. The front end was also affected, as some began speculating that the August 1 tariff hikes could complicate the Federal Reserve's policy decisions.

Economic calendar on Friday The June Treasury budget posted a surprising surplus of $27.0 billion (consensus: -$257.5 billion), compared to a $71.0 billion deficit in the same month last year. The surplus came from revenues ($526 billion) exceeding spending ($499 billion).Note: Treasury budget data is not seasonally adjusted, so the June surplus shouldn't be directly compared to May's $315.7 billion deficit.

Key takeaway: The report showed an actual surplus, with income exceeding expenditures.

Good news: The 12-month deficit shrank from $1.994 trillion in May to $1.896 trillion in June.

Bad news: It's still $1.896 trillion over the past 12 months.

Energy market Brent crude is now trading at $70.50. Crude oil is once again testing the $70 threshold as the new week opening.

Conclusion The US stock market is bracing for key inflation data this week. Both a correction and a renewed rally are on the table.