Vea también

29.08.2025 03:34 AM

29.08.2025 03:34 AM

The GBP/USD currency pair also traded higher on Thursday; however, overall volatility this week has been quite low, and the market is clearly waiting for more significant events than the second GDP estimate or jobless claims. Let me remind you that a new month begins next week, which means that labor market, unemployment, and business activity data will be published. Thus, next week could be not just more interesting than the current one—it may give us an answer to what decision the Federal Reserve will make at its September 16–17 meeting.

From our perspective, the answer to that question remains unclear at this stage. Even though futures markets estimate the probability of a rate cut at about 90%, what justifies such high odds? If you listen closely to Jerome Powell and his colleagues, you can draw the opposite conclusion. For example, Powell at Jackson Hole didn't deny that monetary policy easing could resume in the future, but he never mentioned September. Many of his colleagues, who are not Trump's proteges, are also sticking to a cautious tone. Just yesterday, New York Fed President John Williams said the Fed's September decision would depend on macroeconomic data. Many market participants and analysts interpreted this as a hint of a rate cut.

In other words, the market continues to perceive things that aren't really there. As the saying goes, "I see what I want to see." Recall that traders were expecting seven rate cuts last year and four this year. In reality, the rate was cut three times last year and not once this year. So traders always await the most dovish scenario, and nearly always get it wrong. It's the same now—Christopher Waller and Michelle Bowman are, for well-known reasons, ready to vote for easing at every meeting. Fine, but who else is ready?

Maybe on September 17, the entire Committee will unanimously vote for a rate cut—but to say that, we would need to see at least the next inflation and Nonfarm reports. Until then, we're not making that kind of prediction.

Now, some good news: The dollar doesn't really care if the Fed cuts rates in September or not. Suppose the Fed does cut rates—then what? For the dollar, it is just another bearish factor, adding to a growing collection. What if it doesn't cut? That just means monetary policy stays unchanged. On what basis, then, should the dollar strengthen? In the best-case scenario, the dollar may see modest local strengthening due to unchanged policy, but the overall fundamental background will continue to pull it down. And once the Fed does start cutting, it's just the next nail in the dollar's coffin.

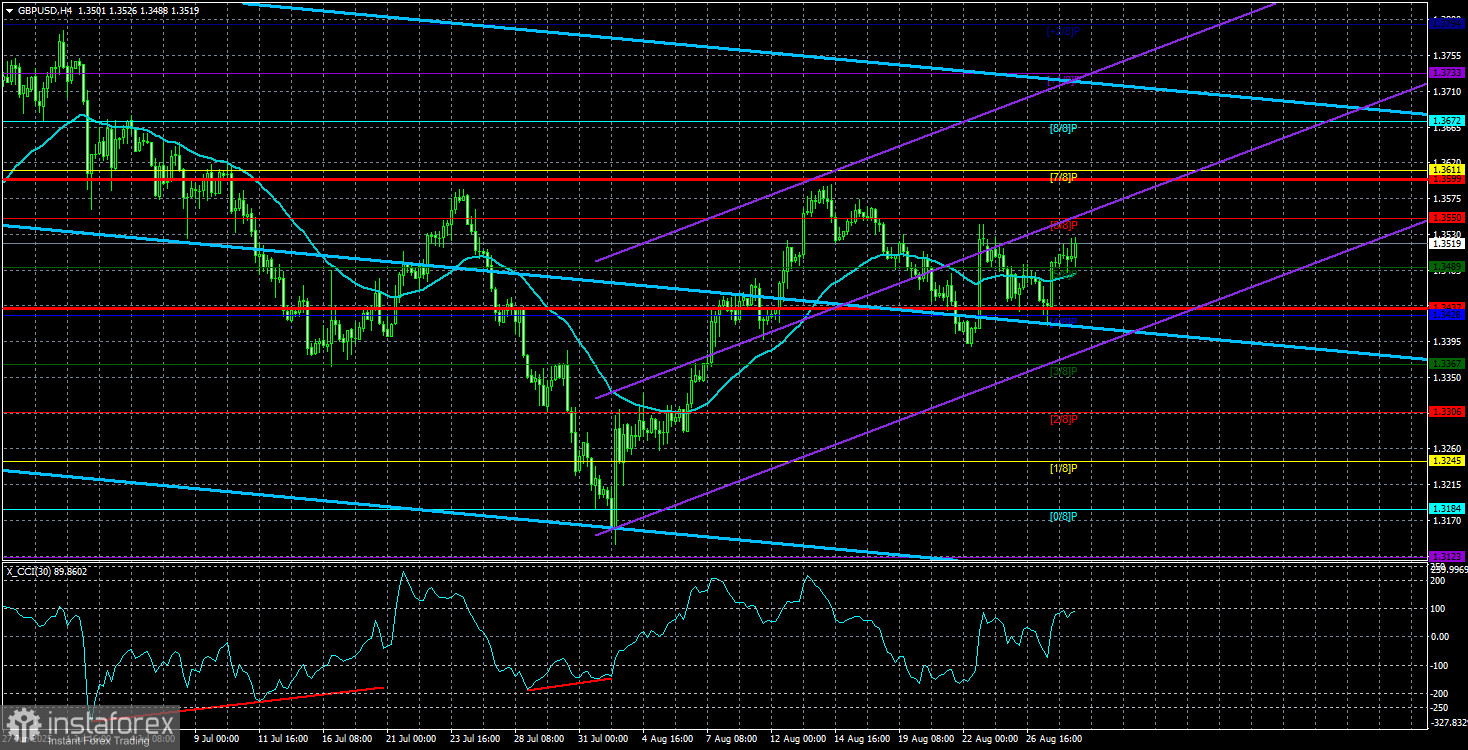

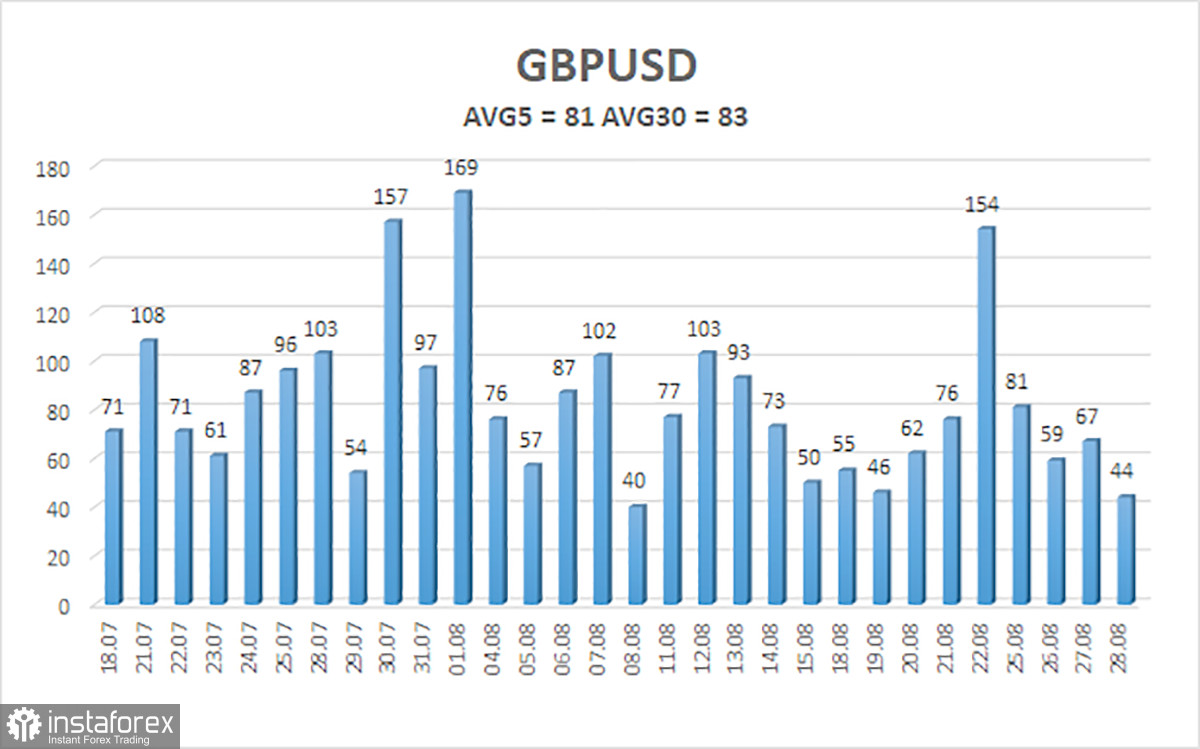

The average volatility for GBP/USD over the last five trading days is 81 pips, which for the pound/dollar pair is considered "average." On Friday, August 29, we thus expect the pair to trade within the range defined by 1.3437 and 1.3599. The upper channel of linear regression is pointing upward, indicating a clear uptrend. The CCI indicator entered oversold territory twice, signaling the resumption of an upward trend. Also, before the new growth phase started, several bullish divergences formed.

S1 – 1.3489

S2 – 1.3428

S3 – 1.3367

R1 – 1.3550

R2 – 1.3611

R3 – 1.3672

The GBP/USD pair has completed another downward correction. In the medium term, Donald Trump's policies will likely continue putting pressure on the dollar. Thus, long positions with targets at 1.3611 and 1.3672 remain much more relevant if the price is above the moving average. If the price is below the moving average line, small shorts can be considered, with a target at 1.3392 on a purely technical basis. From time to time, the US currency exhibits corrections, but for a sustained trend reversal, it requires genuine signs that the World Trade War has ended.