আরও দেখুন

16.06.2025 12:14 PM

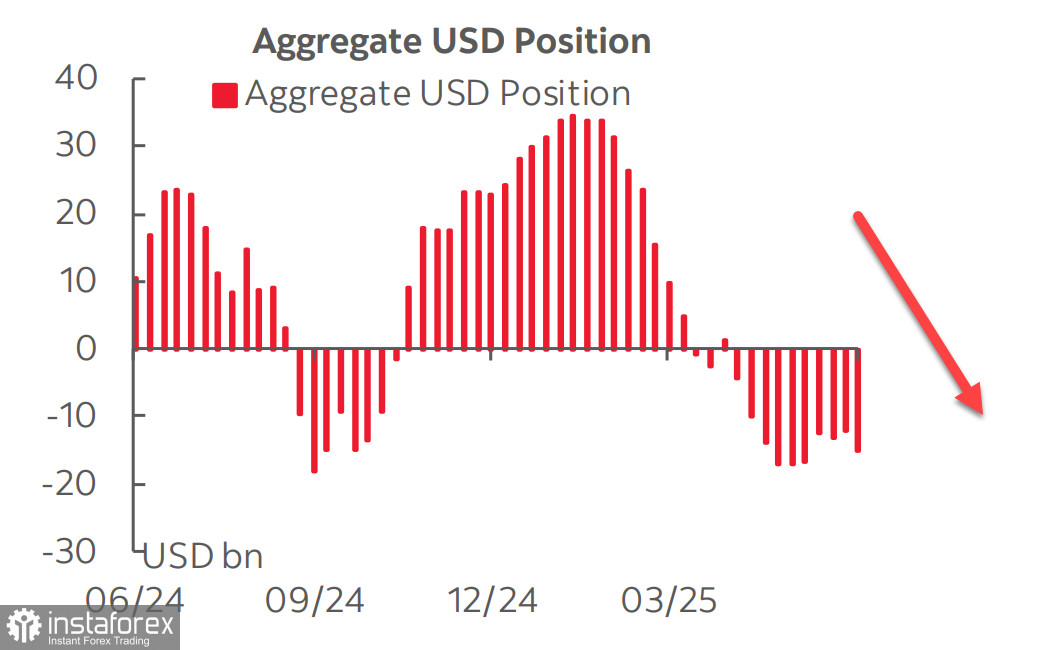

16.06.2025 12:14 PMFive weeks ago, the total short position on the U.S. dollar against major currencies stopped increasing, which gave reason to believe the dollar might begin an offensive in the currency market. However, the latest CFTC report showed this was merely a consolidation. Over the reporting week, the short position increased by $3.7 billion, led by growth in European currencies—primarily the pound and the euro—along with the Canadian dollar joining them. Changes in other currencies were minimal.

It should be noted that this report was outdated by the time it was published, as it does not account for recent developments. Some of those favor further dollar weakening and rising demand for risk assets. In particular, this includes easing tensions in trade relations with China, where both sides clearly want to reach a compromise, as well as the first signs of an agreement between Japan and the U.S. On Friday, it was announced that a long-term deal had been reached for U.S. LNG exports to Japan, totaling $200 billion. This agreement is clearly aimed at correcting the trade balance and is likely a concession from Japan, which may also commit to further investing in the U.S. economy or at least continue purchasing U.S. government bonds—something critically important in light of the impending increase in the U.S. budget deficit.

However, the threat of a full-scale war in the Middle East, initiated by Israel, demands a reassessment of risks in the opposite direction—namely, increased demand for safe-haven assets. August Brent crude futures opened the week above $78 per barrel, and if escalation continues, Iran's threat to block the Strait of Hormuz could become a reality. This hypothetical threat would primarily affect Europe. The U.S. would be forced to intervene, which could lead to completely unpredictable consequences.

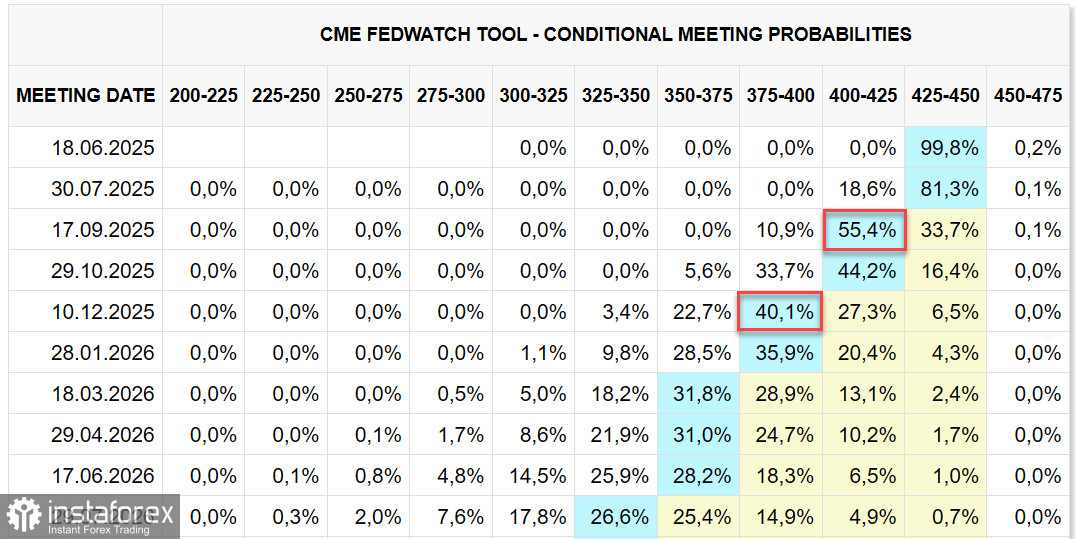

So far, markets have reacted relatively calmly, apart from rising oil and gold prices. The Fed rate outlook remains unchanged: markets expect two cuts this year, in September and December. This forecast implies that U.S. bond yields will remain elevated.

Recent U.S. data has looked quite optimistic. The preliminary June University of Michigan Consumer Sentiment Index, published on Friday, rose from 52.2 to 60.5, and the Expectations Index increased from 47.9 to 58.4—both well above expectations. Additionally, there was a notable decline in 1-year inflation expectations, which indirectly signals continued strong consumer demand and pushes the threat of recession further into the future.

The May consumer inflation report came in below forecasts. Core inflation remained at 2.8% year-over-year, still above the Fed's target, but the key point is that the price growth situation appears fully under control, allowing the Fed to maintain its pause. Investors had feared that new tariffs would lead to product shortages in the U.S., thereby triggering price increases. So far, that hasn't happened, and thus there's no catalyst for dollar growth from that angle.

The stock market reacted to the large-scale bombings in Iran with a drop—but a shallow one—and quickly recovered a significant portion of the losses. This calm response is due to the currently minimal risk of the U.S. being drawn into the conflict, something Trump has no interest in.

The S&P 500 index remains near last week's levels. Attempts to continue its upward movement look feeble.

We assume that the probability of a decline to 5500 is higher than that of an update to the 6150 high. While risks are low for now, the index has been recovering from the sharp drop in April. However, the threat has not been eliminated—only postponed until July. The next two weeks will provide much more clarity, but for now, we still expect a decline in the index.