See also

02.05.2025 09:43 AM

02.05.2025 09:43 AMTrading on the last day of the week is unfolding positively. News that China is ready to begin negotiations has inspired investors to buy risk assets and weakened the U.S. dollar.

Previously, I pointed out that behind the scenes, Washington and Beijing have been in talks regarding trade and its terms. The Chinese publicly denied the matter, but today's announcement from China's Ministry of Commerce has brought the issue to light. The seriousness of the situation is also confirmed by the news that Elon Musk—a close ally and advisor to Donald Trump—is heading to Beijing. It's hard to say what the outcome of the negotiations will be, but one thing is clear: the stalemated confrontation between Beijing and Washington is beginning toward resolution. That's why today, and even yesterday, the most forward-thinking investors began actively buying company stocks, cryptocurrencies, crude oil futures—and selling gold and the dollar.

Given the emerging picture, I believe that the mere fact of an official start to negotiations will be a significant reason for a continued rally in stock markets, especially in the U.S. Economic statistics will also play an important role—particularly inflation data, the PCE index report, ADP jobs numbers, and potentially the U.S. Department of Labor's report due today. These could support expectations that the Federal Reserve may resume interest rate cuts at meetings this month or in June. With such expectations, demand for stocks and tokens will likely grow, while the dollar will most likely remain under pressure.

So today, the U.S. employment report will be released. It is expected that nonfarm payrolls in April increased by only 138,000 versus 228,000 in the previous month. The unemployment rate is anticipated to remain at 4.2%, with average hourly earnings at 0.3%, while average annual earnings are expected to rise from 3.8% to 3.9%.

How will this report affect the dollar?

A traditionally negative trend in the labor market will exert pressure on the dollar, and the decline in inflation, along with the official launch of tariff talks between the U.S. and China, will only reinforce this. However, the dollar's decline will likely be limited, as today's release of fresh consumer inflation data from the eurozone—projected to decrease annually from 2.2% to 2.1%—may justify further rate cuts by the European Central Bank. This would also prompt the Bank of England and other global central banks to consider similar actions. Ultimately, this may help the dollar index stay above the 99.00 mark.

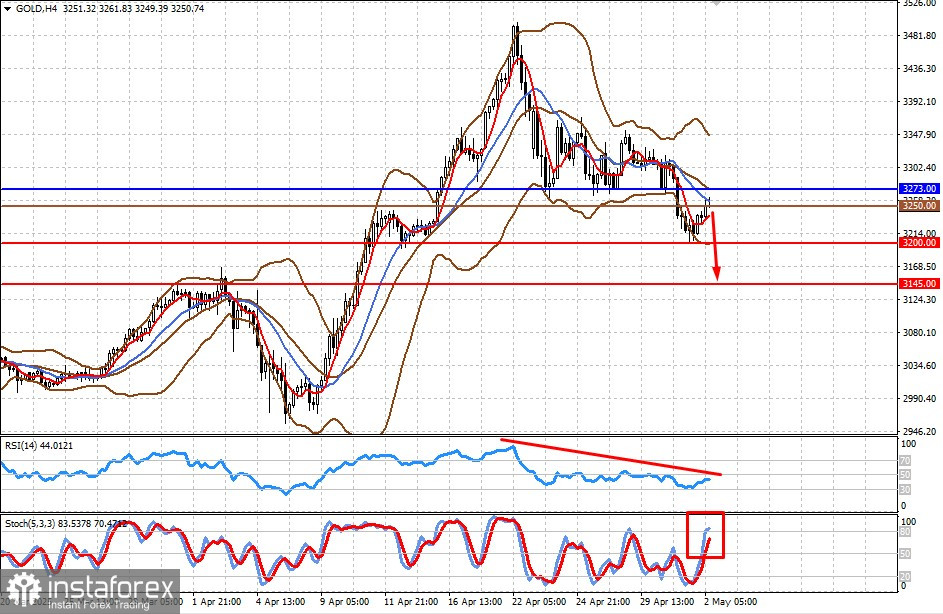

Against the backdrop of the start of trade talks between China and the U.S., gold is likely to decline due to reduced demand stemming from optimism over a possible agreement. In this case, the price may fall to $3200.00, then to $3145.00. A suitable level to sell from could be $3250.00.

The pair is rebounding on increased demand for risk assets, but the decline in eurozone inflation opens the door for a potential ECB rate cut at the upcoming meeting. As a result, the pair could reverse and fall toward 1.1200. A level for selling on a rally could be 1.1329.