See also

03.06.2025 11:41 AM

03.06.2025 11:41 AM

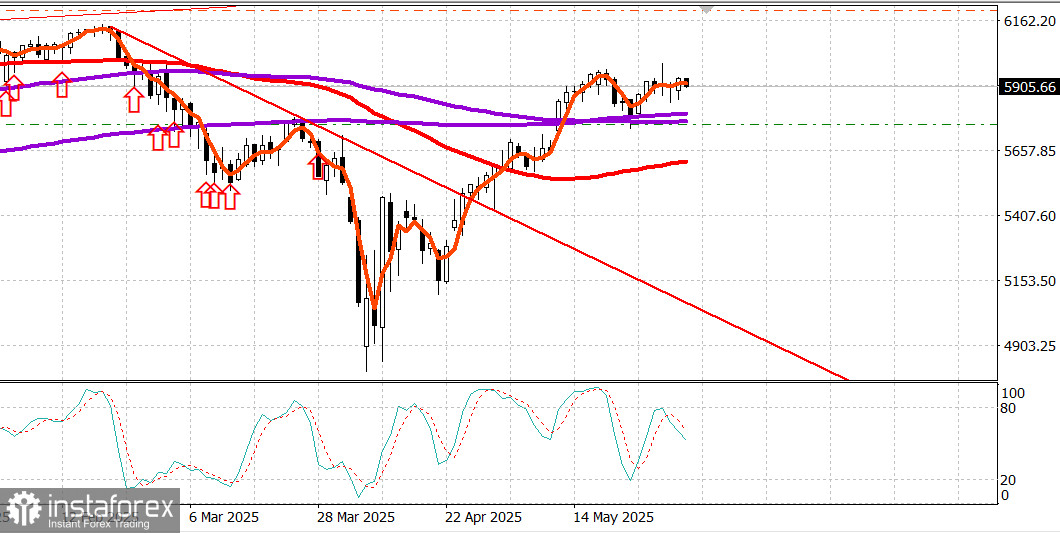

S&P500

Snapshot of major US stock indices on Monday: Dow +0.1%, NASDAQ +0.7%, S&P 500 +0.4%, S&P 500 at 5,936, within the range of 5,400 to 6,200

The stock market took a few hits in the morning but once again demonstrated resilience, with large-cap stocks acting as a stabilizing force.

Meta Platforms (META 670.90, +23.41, +3.6%) reportedly plans to launch fully AI-generated ads by 2026, according to The Wall Street Journal. Meanwhile, NVIDIA (NVDA 137.38, +2.25, +1.7%), a consistent leader in AI, was another top performer.

The Vanguard Mega-Cap Growth ETF (MGK) rose 0.9%, outperforming the Invesco S&P 500 Equal-Weighted ETF (RSP), which gained 0.1% on the day.

The market's initial drop was driven by weekend news that the US would double tariffs on steel and aluminum imports to 50% starting Wednesday, alongside China's aggressive stance accusing the US of breaching a prior trade agreement reached in Geneva.

This combination raised market concerns about potentially higher inflation, stemming not only from the tariff hike but also from possible supply chain disruptions.

The market-cap-weighted S&P 500 fell 0.9% shortly after the open but quickly rebounded following a stronger-than-expected May ISM Manufacturing PMI at 10:00 a.m. ET, as well as a CNBC report suggesting Presidents Trump and Xi may make statements later this week. Later, Reuters, citing a draft letter from the US Trade Representative, reported that Trump's administration would consider the best offers from countries by Wednesday for trade talks.

From the release of the ISM report onward, trading tilted clearly to the upside, with the S&P 500 and Nasdaq Composite both sequentially reaching session highs and largely closing at those levels.

What's notable about this move, besides its occurring on relatively low volume, is that it happened even as Treasury yields were climbing due to selling pressure. This implies the stock market rally may have been partly driven by a shift of capital from bonds to equities.

We might also speculate that short covering and pressure on cash-heavy investors who feared missing out on further upside played a role, as the market's persistent strength compelled them to re-enter.

10 out of 11 S&P 500 sectors finished higher. The Energy sector (+1.2%) was the top performer, buoyed by a 3.0% increase in oil prices ($62.57, +1.81) after OPEC+ agreed to raise output by only 411,000 barrels per day in July—less than what traders had feared.

The Information Technology sector (+0.9%) was the second-strongest, contributing significantly to the market's broader gains, alongside Communication Services (+0.6%). The only sector to close slightly lower was Industrials (-0.2%).

Market breadth revealed the narrow scope of Monday's rally. Declining issues outpaced advancers by about 5 to 4 on the NYSE, while advancers slightly outnumbered decliners on the Nasdaq.

Year-to-date performance:

Economic calendar on Monday

ISM Manufacturing Index (May) slipped to 48.5% (consensus: 49.0%) from 48.7% in April.

A reading below 50.0% signals contraction, indicating that manufacturing activity declined at a slightly faster pace than the previous month.

Key takeaway: Tariff-related uncertainty weighed on manufacturing activity.

Construction Spending (April) declined 0.4% month-over-month (consensus: +0.1%) after a downward revision to March (-0.8% vs. prior -0.5%).

Private construction: -0.7% MoM

Public construction: +0.4% MoM

Year-over-year: -0.5%

Key takeaway: Residential spending fell notably due to a slowdown in new single-family home construction.

Energy market

Brent crude rose to $64.90 a barrel, a notable increase driven by the realization that OPEC's production boost was smaller than the market had anticipated.

Conclusion The US stock market demonstrated strength on Monday, reinforcing the case for a potential breakout to new yearly highs.