Veja também

18.08.2025 09:47 AM

18.08.2025 09:47 AMDon't believe your eyes, believe your ears. At first glance, the market should react more strongly to robust retail sales data than to consumer confidence indices after all, what Americans do matters more than what they say. However, the 30% rally in the S&P 500 from the April lows has left the broad stock index extremely vulnerable to the "buy the rumor, sell the fact" principle.

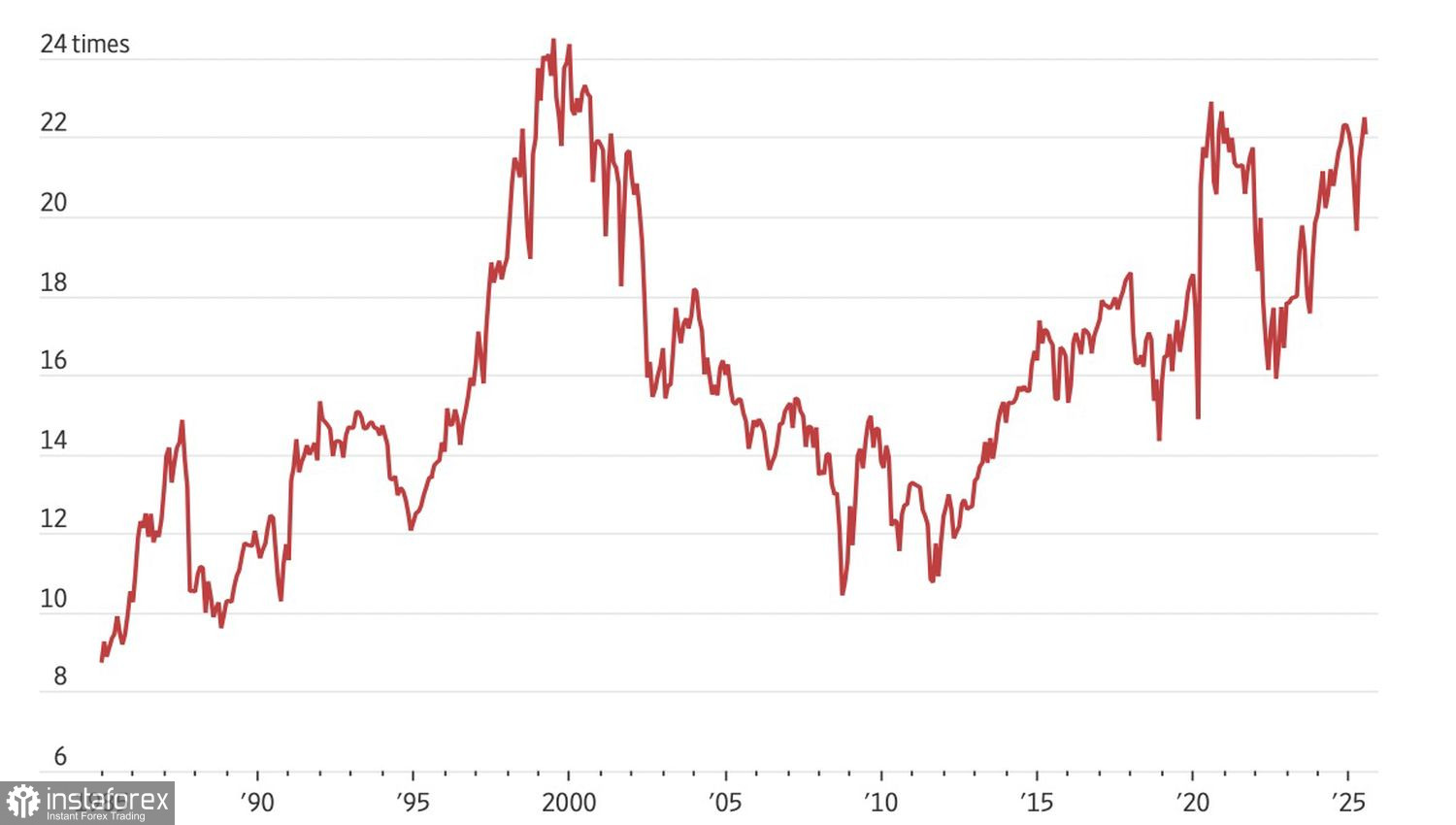

High fundamental valuations alone are not enough reason to take profits. The S&P 500 can still extend its rally even at a price-to-earnings ratio of 22.5. This is the highest P/E since 1985, except the dot-com bubble of 1999–2000 and the 2020–2021 surge.

Still, high valuations increase the risk of disappointment if artificial intelligence technologies or the U.S. economy fail to meet expectations. Both areas carry risks. As soon as the consumer sentiment index issued another signal of stagflation, the S&P 500 stepped back.

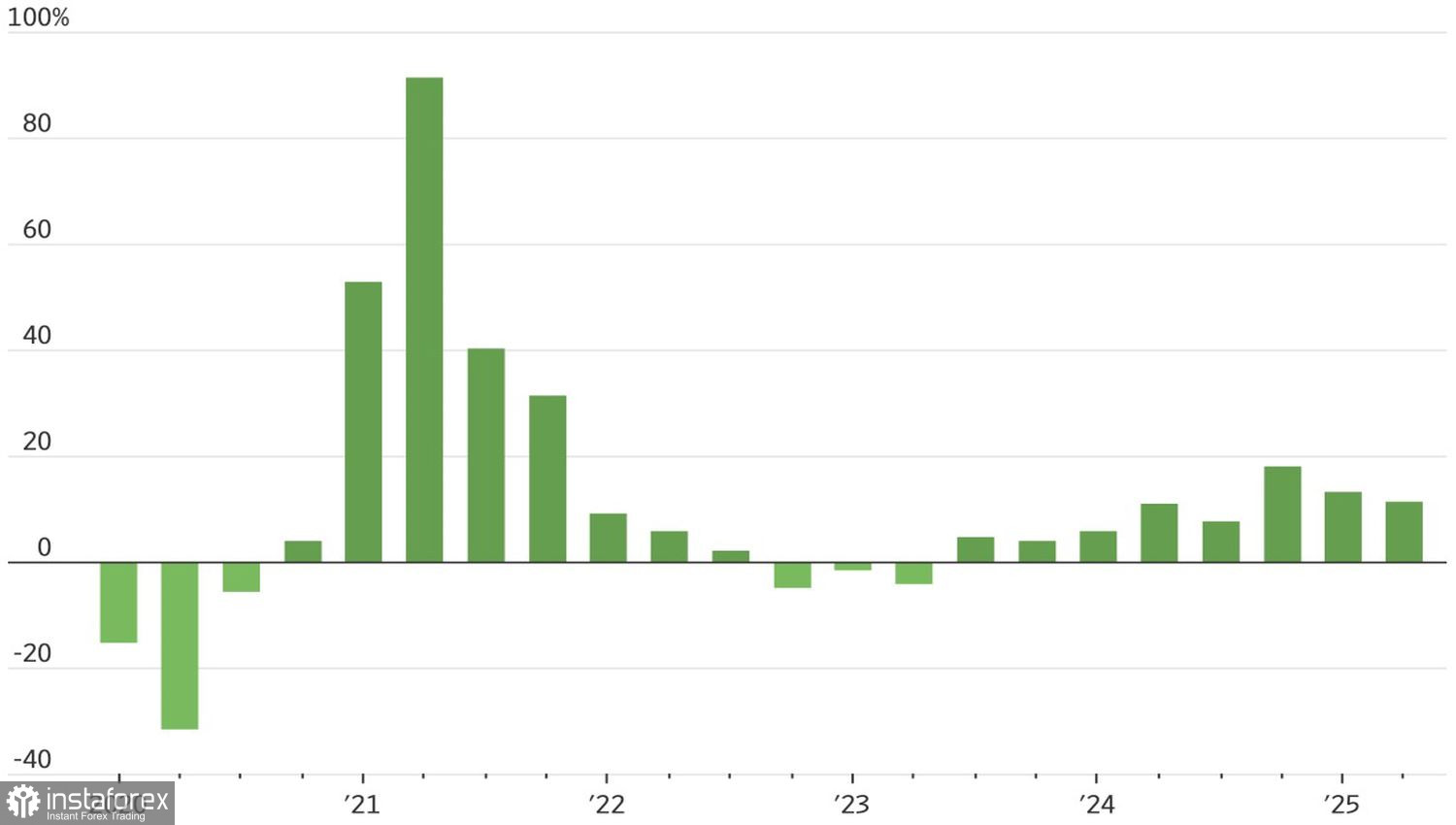

One reason for the impressive April–August rally in the broad stock index was strong corporate earnings. Profits are estimated to have risen 12% in the second quarter—more than double the 5% Wall Street analysts had forecast at the start of earnings season. However, this success was concentrated in just three S&P 500 sectors: technology, telecommunications services, and finance. Four out of eleven sectors ended in negative territory, and the rest barely stayed afloat.

With earnings season winding down, the U.S. economy sending mixed signals, and trade-related news no longer impressing investors, the S&P 500 is rising mainly on expectations of an imminent resumption of the Federal Reserve's monetary easing cycle. Remarks by Treasury Secretary Scott Bessent about cutting the federal funds rate by 50 bps in September and by 150–175 bps in the near future are adding fuel to the fire.

Unfortunately, in reality, investors may be in for a major disappointment. The slowdown in employment reflects not only weaker demand but also shrinking supply due to the White House's anti-immigration policy. As a result, unemployment is not rising. The labor market is not as weak as the U.S. administration tries to present it. If that is the case, expectations of three rounds of Fed monetary easing in 2025 are highly overstated.

If the S&P 500 loses its key driver, the broad index will head into a correction. According to Bank of America, it may be triggered by dovish rhetoric from Jerome Powell at Jackson Hole. Investors have been buying the rumor for too long. It is time to sell the fact.

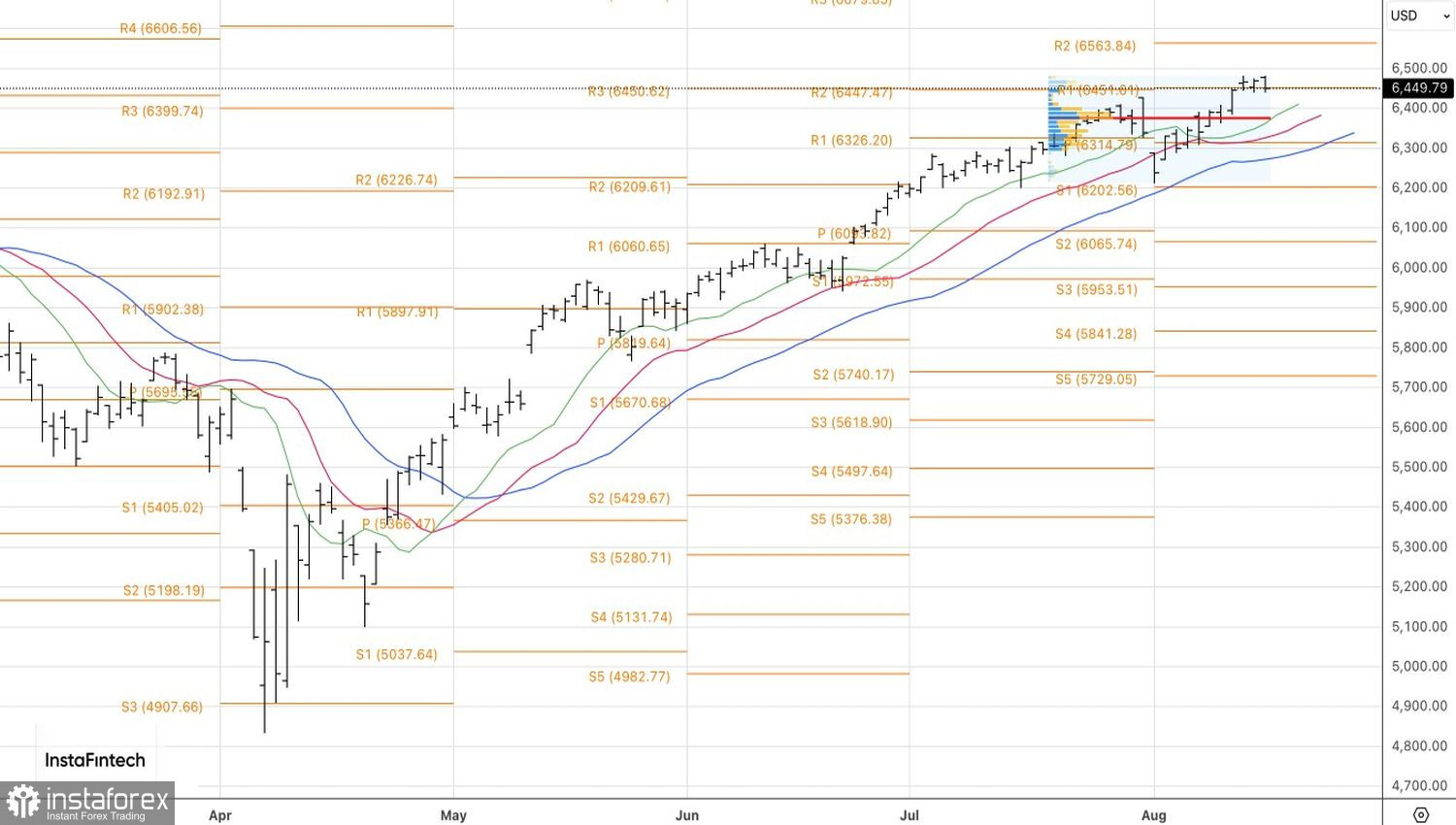

Technically, on the daily chart of the S&P 500, bears have managed to return to the game and are holding onto the pivot level at 6450. This serves as a kind of red line. A rise above it will be a reason to buy. Conversely, a decline will open the way for selling the broad stock index.