Vea también

16.06.2025 10:51 AM

16.06.2025 10:51 AMIsrael and Iran are exchanging missile strikes, but it seems markets are trying to play their own game, assuming that this conflict will not cross the nuclear threshold. In the meantime, investors are shifting their focus to key events this week.

The main highlights will be the consumer inflation reports from the UK and the eurozone. In the EU, inflation is expected to stabilize at 1.9%, while in the UK, it is forecast to decrease from 3.5% to 3.3% year over year.

This week will also bring central bank meetings in Switzerland, the UK, and, of course, the U.S. Federal Reserve—which will likely take center stage and divert attention from the two European central banks.

Other events worth focusing on include the release of the Philadelphia Fed Manufacturing Index and U.S. retail sales figures.

But let's return to the week's main event—the Fed's final monetary policy decision, which will be made over two days, Tuesday and Wednesday. According to the consensus forecast, the central bank is expected to leave the key interest rate unchanged at 4.50%. The main reasons for this are persistently high consumer inflation figures, which showed an annual increase last week (albeit smaller than expected), and uncertainty about the consequences of Donald Trump's presidency. Fed Chair Jerome Powell has previously cited both as reasons to pause the rate-cutting cycle.

So, what might come of the Fed holding rates steady?

Frankly, not much. Ongoing uncertainty will continue to be the primary driving force in the markets. Traders are starting to anticipate rate cuts in the second half of the year. However, I believe there is a strong chance that rates will remain unchanged until next year. This is due not only to the risk of inflation returning to 3% and the murky geoeconomic policies of the U.S. president but also to the unresolved U.S.–China trade war and its unclear outcome.

Given this combination of negative factors—each of which obstructs rate cuts—and the fact that the market has already priced these into its expectations, we can anticipate a continuation of existing trends:

Under such circumstances, token prices are unlikely to break above their recent highs. They are more likely to remain within broad trading ranges.

Geopolitical developments and events in the Middle East will continue to affect gold, the dollar, and stock markets.

Overall, based on the broader market picture, I believe that the outcome of the Fed meeting will not bring any significant changes.

The geopolitical conflict in the Middle East supports gold prices. If support at 3408.20 is broken, a downward correction toward 3382.00 is possible before an attempt to resume growth toward the recent high of 3450.70. A potential sell level could be around 3404.12.

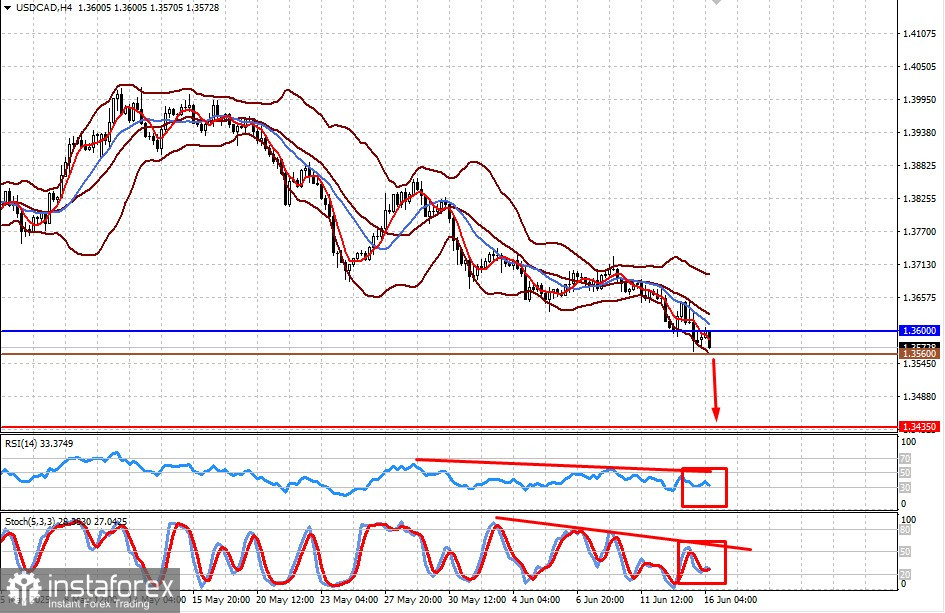

The pair is declining amid rising crude oil prices, which support the Canadian dollar, a commodity-linked currency. If oil prices resume upward momentum, USD/CAD will face pressure again. If the pair fails to rise above 1.3600, a decline toward 1.3435 is likely. A potential sell level is 1.3560.