Vea también

04.07.2025 12:48 AM

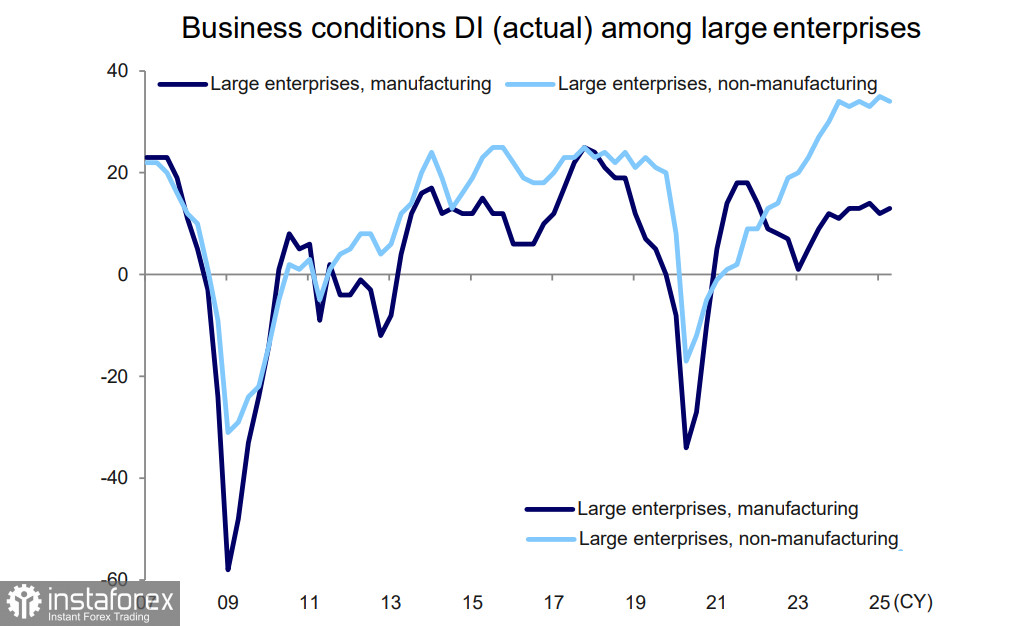

04.07.2025 12:48 AMThe Bank of Japan's quarterly Tankan report showed that the impact of new US tariffs has not yet had a significant effect on corporate sentiment, and business conditions for large manufacturers unexpectedly improved compared to the March survey.

Business conditions for large enterprises rose by 1 point to +13. The forecast for the next quarter showed a 1-point decline to +12. In the automotive sector, the outlook also declined by just 1 point, suggesting that the impact of Donald Trump's tariffs is not yet expected to be particularly problematic.

Japan and the US have already held seven rounds of trade talks aimed at resolving all bilateral disagreements, but no progress has been made. In its July 1 report, the Mainichi newspaper described the negotiations as "deadlocked," and the prospects of reaching an agreement before the tariff suspension expires on July 9 look grim.

On June 20, Trump stressed that he had no intention of lowering the tariff rate on vehicles, calling it "unfair" that "Japan doesn't accept our cars, but we import millions and millions of their cars into the United States." The next day, he stated that "Japan doesn't take our rice, and they have a massive rice deficit," hinting that on July 9, he may unilaterally impose higher tariffs on Japan. Then, on July 1, Trump told reporters that he was "not sure we will make a deal" and suggested tariffs on Japanese imports could rise to 30% or 35% (i.e., beyond the general 24% mutual tariff rate).

Currently, Japan is expected to extend the tariff suspension until September 1, but the risks are high given Trump's clear dissatisfaction.

All of this is certainly interesting, but the key question is: how do the negotiations influence the BoJ's stance on interest rates? The BoJ minutes from the June 17 meeting suggest that the Bank intends to maintain a wait-and-see approach until the tariff issue is resolved. Since automobiles are the foundation of Japan's exports to the US, the BoJ will not rush to hike rates without a deal — the issue is too important and leaves no room for error.

Conclusion: The longer the negotiations drag on, the longer the BoJ's pause will last. And the longer the pause, the greater the uncertainty, as there is no driver for yen appreciation. Market forecasts currently assign just over a 50% chance of one rate hike by year-end, which is insufficient for the yen to resume its previously halted rally.

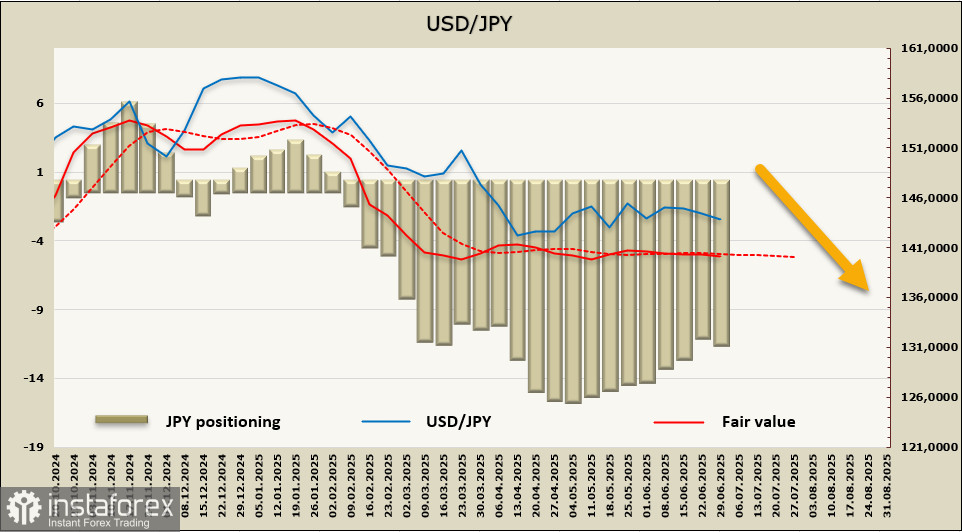

After seven consecutive weeks of decline, the net long position on the yen increased by $148 million to $11.4 billion — a clear bullish bias — but the lack of movement in the fair value suggests a lack of direction for USD/JPY.

The yen remains in a trading range, with no clear direction. If the negotiations result in an outcome more favorable to Japan than the unilateral US-imposed tariff rate, the likelihood of a BoJ rate hike will increase, and the USD/JPY exchange rate will likely break downward out of the range, targeting the 127–129 area. If there is no resolution, risks will rise, and in that case, range-bound trading will likely continue, with a slow upward drift toward 149–150.