Vea también

23.07.2025 12:13 AM

23.07.2025 12:13 AMThe more the U.S. dollar falls, the more its decline resembles a bubble. This view, shared by HSBC, is hard to disagree with. There is a prevailing consensus in the market that after a more than 10% drop in the first half of the year, the USD Index will continue to decline in the second half. However, if the crowd were always right, the Sun would still be revolving around the Earth.

HSBC believes it's still too early for the dollar bubble to burst. But eventually, it will happen. EUR/USD will undergo a deep correction. This is entirely possible. However, such a correction would run counter to the White House's interest in weakening the greenback. A weaker dollar boosts the competitiveness of American companies and contributes to profit growth. To achieve its goals, Washington uses a carrot-and-stick approach—first escalating tension with threats, then backing off.

This is exactly what happens with tariffs. This is also how the situation with Jerome Powell's potential dismissal has unfolded. Donald Trump has made it clear that removing the Federal Reserve Chair would be acceptable to the president. However, Treasury Secretary Scott Bessent stated that there is currently no indication of an imminent dismissal. If the head of the central bank wants to step down—so be it. If not—he can serve out his term until May 2026.

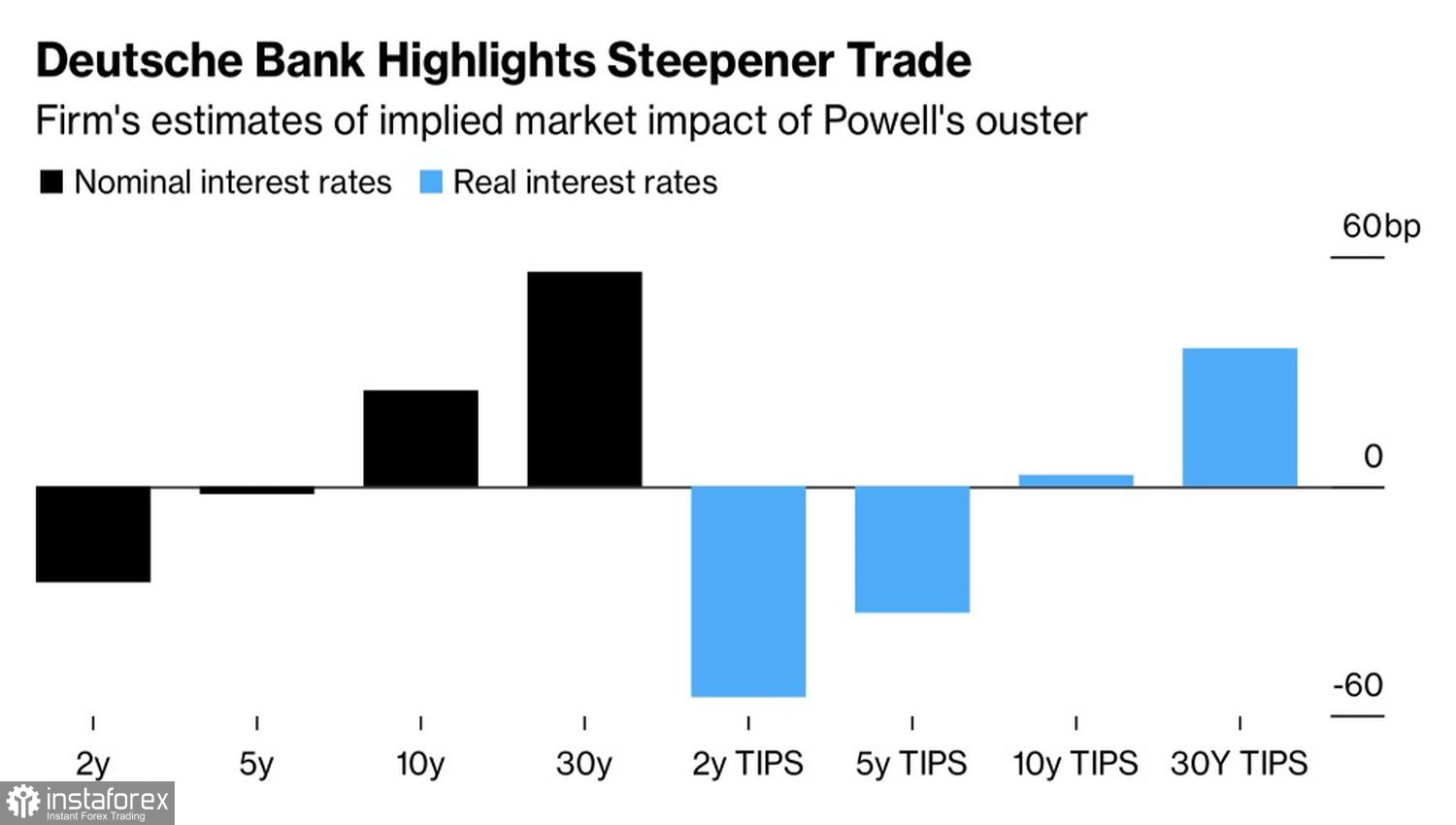

According to Deutsche Bank, Powell's departure would aim to simplify monetary policy. Investors would likely demand a higher risk premium, which would push up U.S. Treasury yields. At the same time, a return to the "sell America" strategy could sink the dollar.

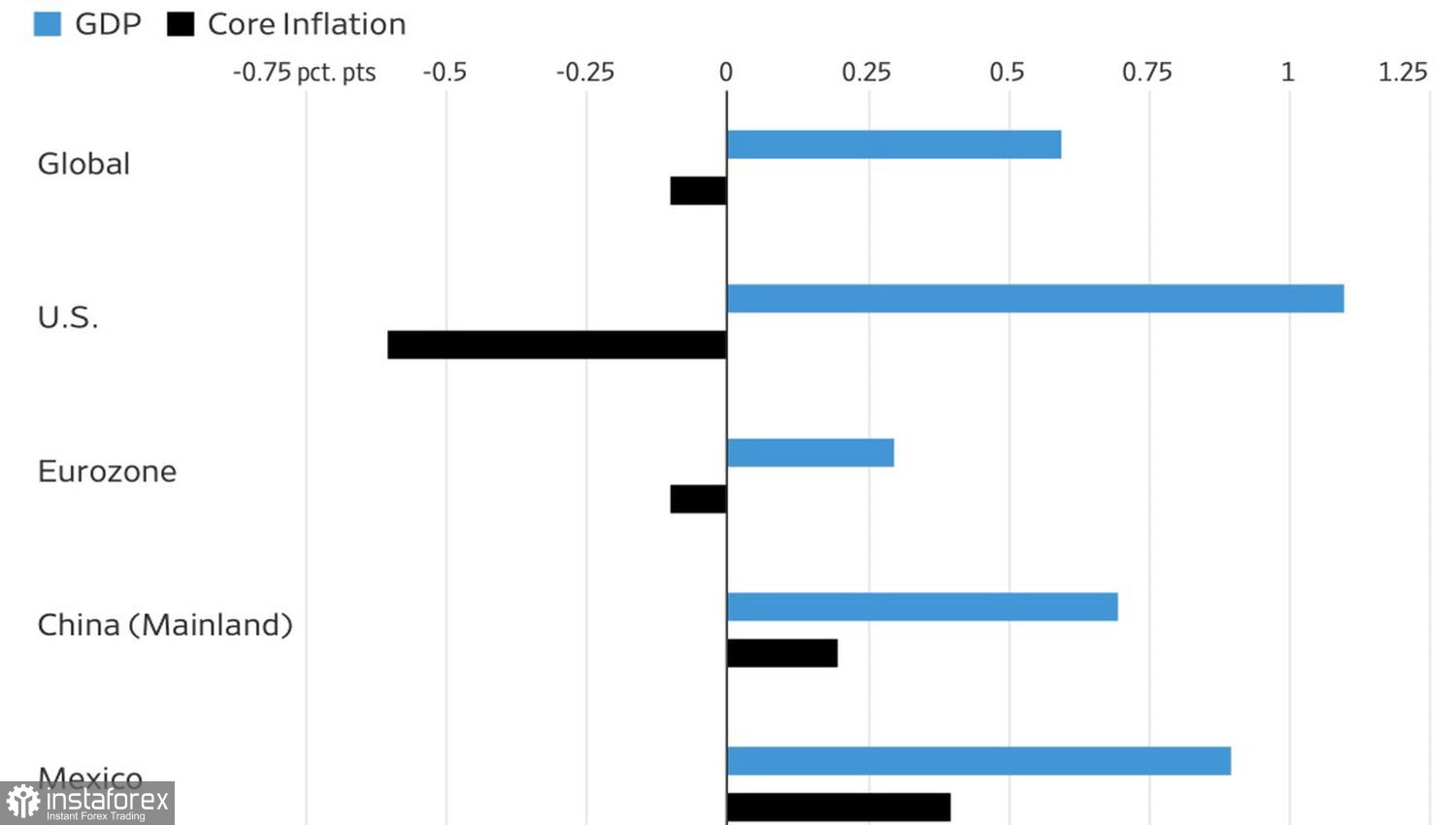

The problem is that White House pressure on the Fed Chair is virtually the only effective tool for weakening the greenback. In the first half of the year, the USD Index fell not due to monetary policy, but because of accelerating global economic growth. According to JP Morgan, global GDP picked up to 2.4%, driven by a front-loaded surge in U.S. imports. The 90-day tariff delay helped stimulate international trade.

Significant changes are looming in the remainder of the year. Tariffs generate revenue for the U.S. government, and Trump has no intention of abandoning them. Starting August 1, import duties will increase. First, international trade will slow down, followed by global GDP. The U.S. dollar is the currency of pessimists—it rises when things go wrong. In the first half of the year, things were going well, and the USD Index declined.

In my view, a narrative shift on financial markets is imminent. Instead of buying the dip on the S&P 500, traders will start selling the index on rallies. And EUR/USD risks going down with it.

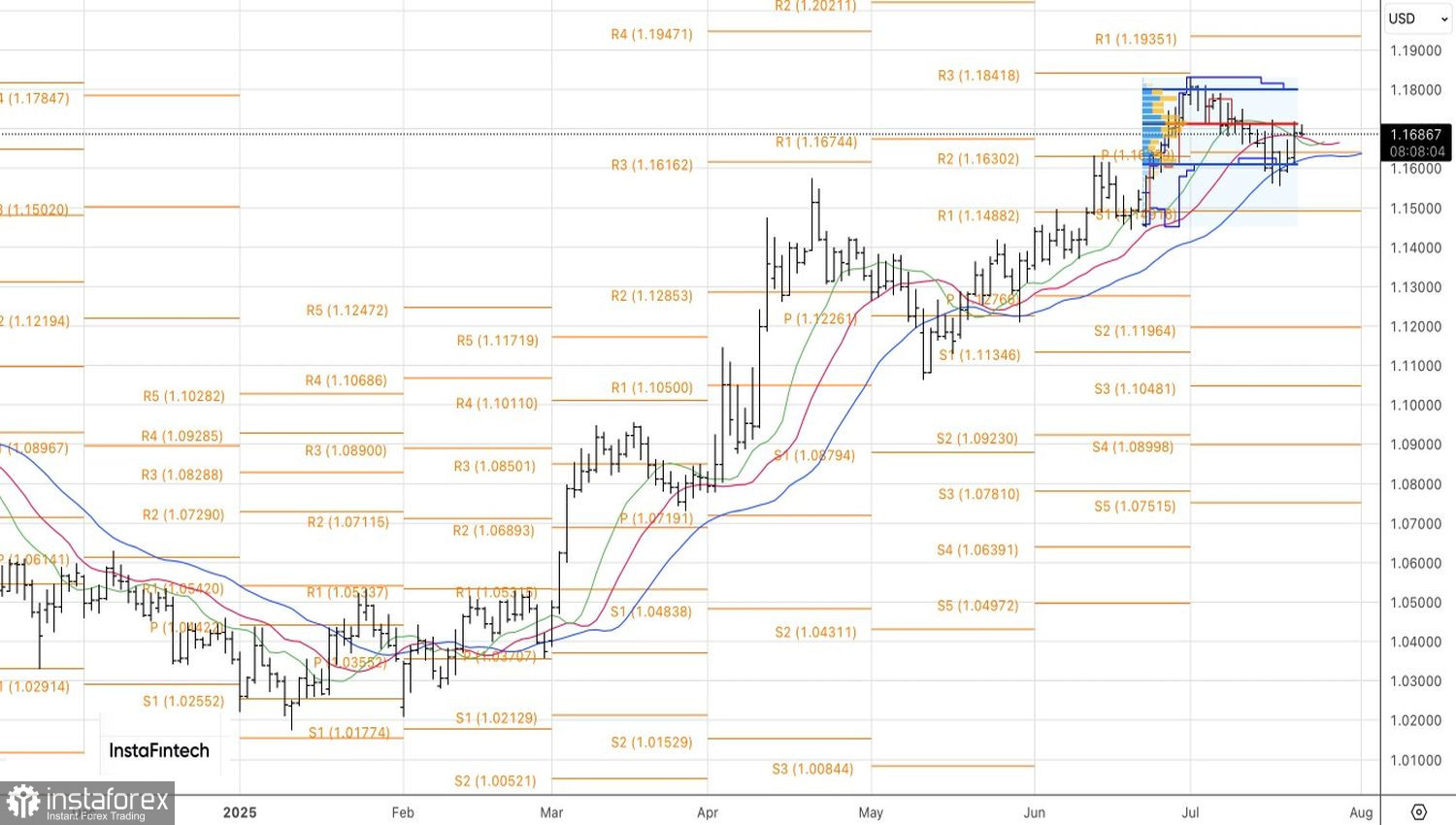

Technically, the daily chart of the main currency pair shows a retest of fair value at 1.1715. A breakout above this level would increase the likelihood of a renewed uptrend and provide justification for adding to long positions opened at 1.1640. Conversely, a rejection at this level would allow traders to reverse and switch to selling EUR/USD.