See also

21.05.2025 09:46 AM

21.05.2025 09:46 AMAmong the economically developed nations—those that belong to the Western wing of the global economy—there is an important rule: a target of 2% inflation, specifically consumer inflation. Achieving this target is not just a goal but a rule set in stone. Every central bank—be it the Federal Reserve, the European Central Bank, or the Reserve Bank of Australia—is expected to follow it.

In the last quarter of the 20th century, inflation in the U.S. reached remarkable levels by today's standards—over 14%, peaking in 1980 at 14.8%. Back then, America lived within its means, and the Fed was not yet the global emission center. The economy was still industrial and suffered occasional crises. However, with the implementation of the large-scale Reaganomics program under President Ronald Reagan, the U.S. shifted to a "life on credit" model—any American earning at least something could take out a loan and buy everything at once instead of gradually over a lifetime. Around this time, the idea of a 2% inflation target emerged—somewhat randomly. Why consumer inflation? Because the U.S. transitioned from an industrial economy to a post-industrial one, relying on the rest of the world for production while it printed dollars. This is a simplified picture, of course, but broadly accurate.

So why exactly 2%? The Fed lent money to the entire world through sales of its Treasuries and was strongly interested in keeping yields on those instruments low to avoid destabilizing the American financial system through high interest payments. That economic model still largely holds today, despite Donald Trump's attempts to reform it and return the U.S. to industrial development.

Now, the key question is: Why do Western central banks, except for Japan's, continue to follow this model? Not just because they're tied into dollar-based credit, which is largely unbacked except by trust in the Fed and the U.S. Rather, Western countries are directly dependent on U.S. interest rates—or more precisely, on U.S. monetary policy. This includes the ECB, Bank of Canada, and others. There are specific proportional relationships between U.S. and eurozone rates that depend on trade and current account balances. Inflation shocks may occasionally disrupt these proportions, but they tend to realign.

Right now, the Fed is weighing whether to continue cutting rates. Meanwhile, the ECB and Bank of England have paused, even though inflation nears the 2% target. They're maintaining parity by watching the Fed.

Will global central banks continue to cut rates? Yes, but only those that can do so without disrupting the rate equilibrium with the Fed, such as the Reserve Bank of Australia and the Reserve Bank of New Zealand. Others will follow only if the U.S. resumes rate cuts. This implies that the U.S. dollar will remain under pressure against major currencies, not only because of expected rate cuts but also due to current rate proportion dynamics that don't favor the dollar. With this in mind, we can expect the dollar index to decline toward the 98.00 mark soon.

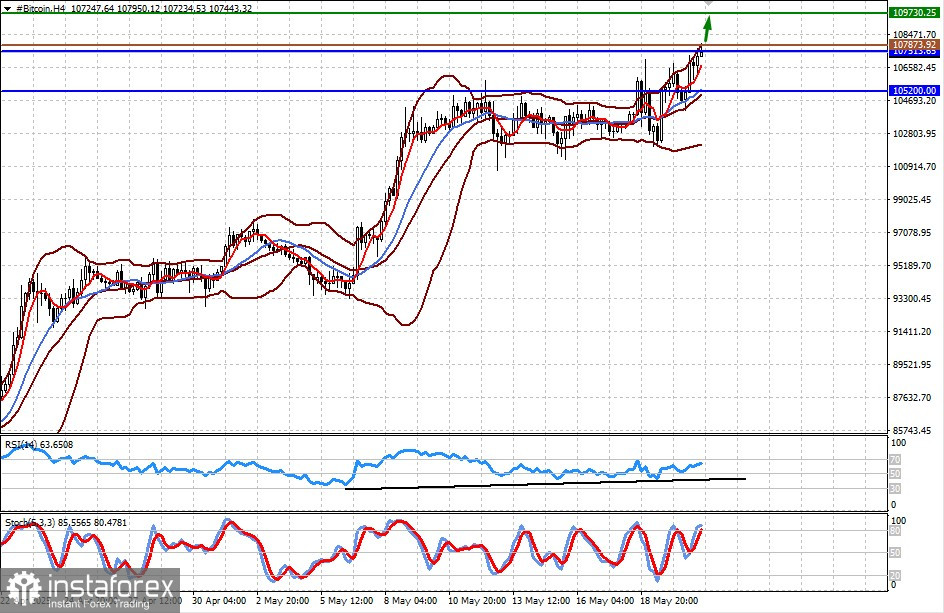

A significant decline in the dollar's value is contributing to Bitcoin's rise. It has broken out of the range above the resistance level of 105,200.00 and is heading toward its recent high, likely testing it. Breaking and holding above 107,513.65 could lead to a move toward 109,730.25. A potential buy entry could be at 107,873.92.

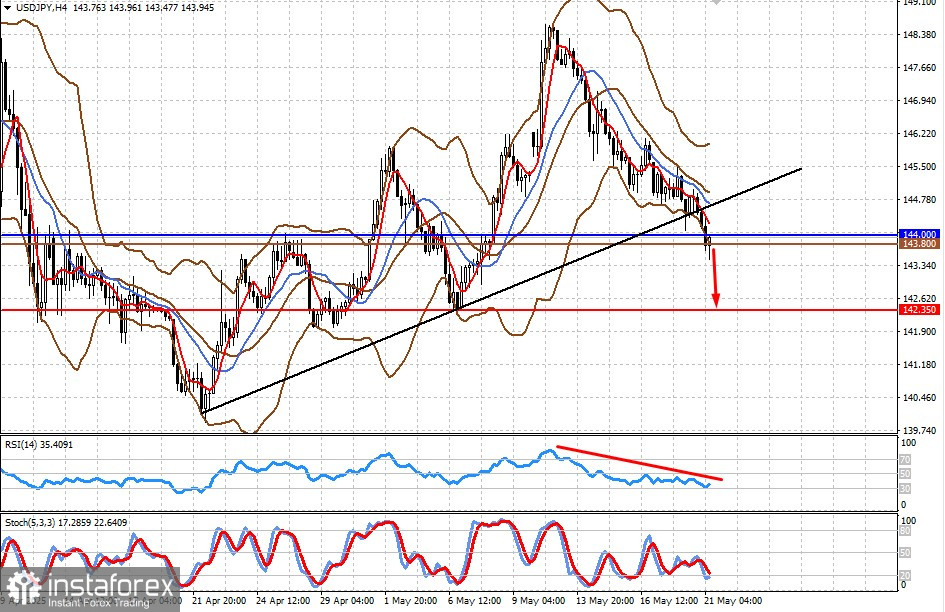

The pair is trading below the 144.00 level. After a local upward retracement, it will likely resume a downward movement, and on dollar weakness, it could fall toward 142.35. A potential sell entry could be around 143.80.