See also

12.06.2025 04:53 PM

12.06.2025 04:53 PMMarkets rise on rumors and fall on facts. For a long time, the S&P 500 had been rising due to investors' confidence in a US-China trade agreement. Once the deal was signed, investors rushed to lock profits on long positions. Donald Trump announced that the deal had been eventually signed, under which US tariffs on imports from China would be 55%, while Chinese tariffs on US exports would be 10%.

Commerce Secretary Howard Lutnick claims that the issue is now settled, and tariffs on imports from China will no longer rise. Treasury Secretary Scott Bassett announced that the 90-day tariff delay could be extended for countries that are negotiating in good faith with the US. These remarks by White House officials were a continuation of the previous tactic aimed at supporting the S&P 500 rally through bold statements. The market, however, preferred to sell the facts.

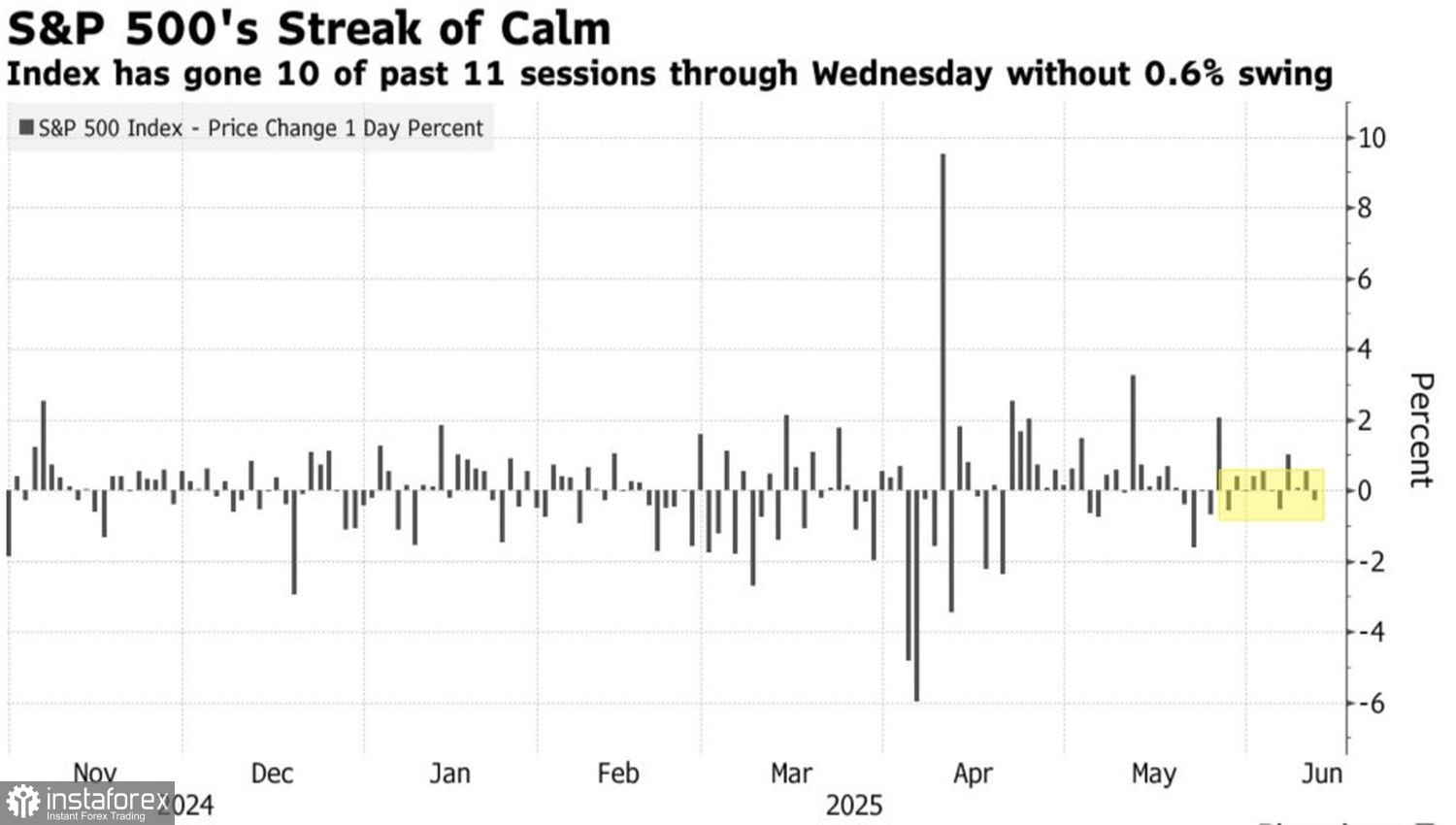

Daily dynamics of the S&P 500

The broad stock index has not been this calm since December. Over the past 11 out of the last 12 trading sessions, it has moved by no more than 0.6% in either direction. Sooner or later, the calm in the stock market will be replaced by a storm.

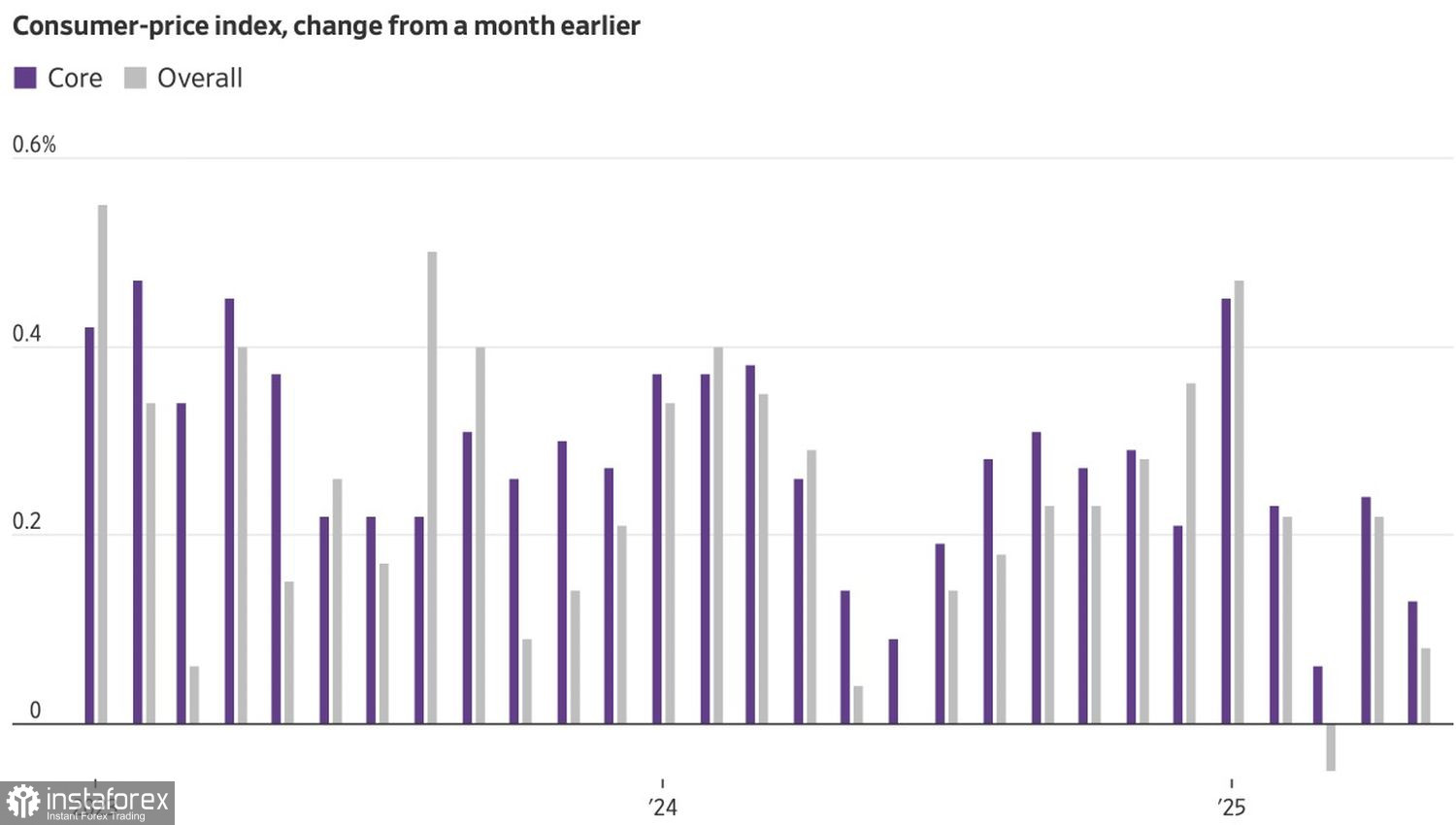

Along with the desire of investors to lock in profits on long positions following the conclusion of the US-China trade deal, the decline of the S&P 500 was also driven by disappointment. A series of positive reports on the health of the US economy, including strong May nonfarm payrolls, led people to believe that everything was fine. However, doubts resurfaced among investors due to the weak momentum in inflation.

US inflation dynamics

The persistent disinflationary trend may be linked to two reasons: either domestic demand has tanked so much that it no longer supports price increases, or companies, which accumulated significant inventories during the front-loading of US imports, are artificially keeping prices down. This is to observe how consumers react.

Most likely, the S&P 500 took the first reason at face value. Signs of weakness in the US economy spooked the "bulls" and forced the broad stock index to retreat. The benchmark index didn't find support from the likelihood of monetary expansion in the US. Meanwhile, the odds of one act of monetary tightening by the Federal Reserve in 2025 dropped from 39% to 32%, while the chances of three or more steps by the central bank to ease monetary policy rose from 22% to 28%.

The 21% rally in the S&P 500 from the April lows allowed traders to ignore the underlying issues. However, once the broad stock index retreated, these issues came into focus. As the US economy is cooling, tariffs have been reduced but they are still in place. The reaction of inflation to these tariffs is unknown. Uncertainty breeds fear.

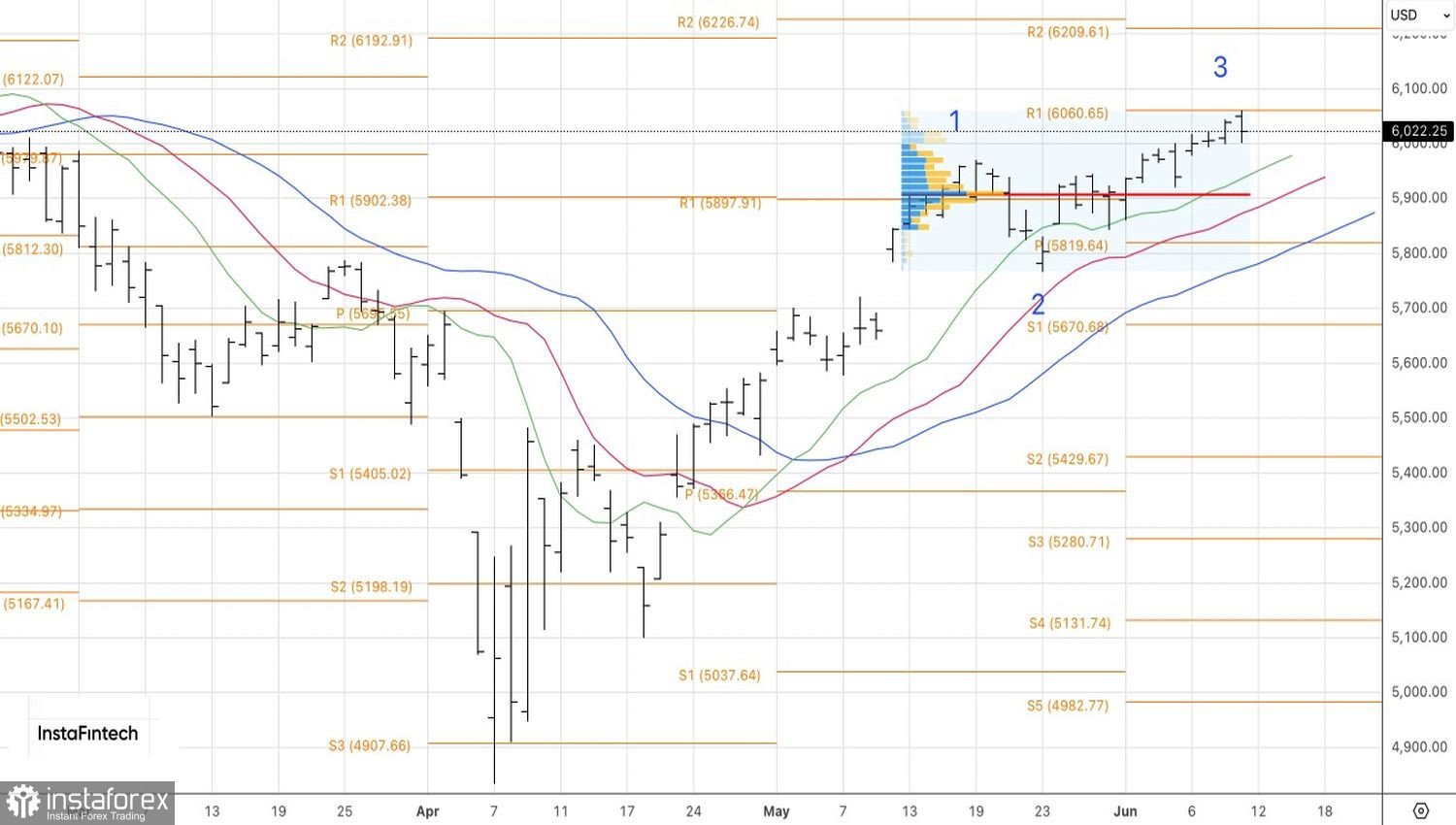

Technical outlook on the S&P 500

On the daily chart of the S&P 500, the inability of the bulls to break above 6,060 became a sign of their weakness and led to the formation of short positions. The reason to increase these positions would be a further drop in the broad stock index below 5,995.