See also

21.08.2025 09:37 AM

21.08.2025 09:37 AMMarkets are in a challenging position amid uncertainty over whether the Federal Reserve will cut interest rates in September or not. This is a truly important question, as the U.S. central bank's influence on global financial markets is significant.

The minutes of the latest Fed monetary policy meeting, released on Wednesday, brought nothing new. They confirmed the general decision to leave all monetary policy parameters unchanged, and that two members of the Federal Reserve Banks considered it necessary to cut rates at the meeting.

Investors, finding nothing noteworthy in the minutes, largely ignored them, focusing instead on the deflation of the artificial intelligence hype in U.S. equities and on Jerome Powell's upcoming speech tomorrow at the Jackson Hole symposium in Wyoming.

The absence of clear signals regarding the possibility of rate cuts is putting pressure on expectations of monetary easing, as seen in the dynamics of federal funds futures. The probability of a rate cut has declined smoothly from a recent high of 95% to 81.6% this morning. Despite this drop, expectations remain elevated, though they are far from a guarantee that rates will be lowered.

In this familiar dual stance, which the Fed has maintained for over six months, market participants are now trying to assess what Powell's speech will bring—especially since it is already known that he will leave his post in May next year.

Some believe that his speech will be broader in scope and may effectively serve as the Fed's programmatic statement for the next several years. He is unlikely to abandon his cautious stance toward uncertain economic prospects and the contradictory situation in which the central bank's mandate pulls in opposite directions. Weakness in the labor market calls for rate cuts, but inflation at 2.7%—still far from the 2% target—argues against it. How Powell will act under such circumstances is unclear, which only adds to uncertainty.

Of course, all of this is interesting, but what investors want to know is whether there is a real chance of monetary easing or not.

Although many believe that the debate over rate cuts has already taken on a political dimension, aiming to undermine the presidency of Donald Trump, unpopular with the "deep state," there is still a strong possibility that at the symposium, the Fed Chair may announce a new model for assessing an acceptable inflation level. Instead of 2% or lower, the benchmark could be raised to 2.5% or even higher. This would allow the Fed, without breaching its mandate, to cut rates in September by 0.25% or perhaps even 0.50%. If such a model is announced, demand for equities would soar, and the dollar would come under pressure.

To sum up, the scenario described above could materialize, but only if the Fed, through its leader, moves away from past monetary models and presents a new framework suited to current conditions.

The pair is trading above 1.1620. If Powell signals a shift in monetary policy from hawkish to dovish, demand for risk assets is likely to rise, and the dollar may weaken. In this case, the pair could climb toward 1.1715. A buying level could be set at 1.1640.

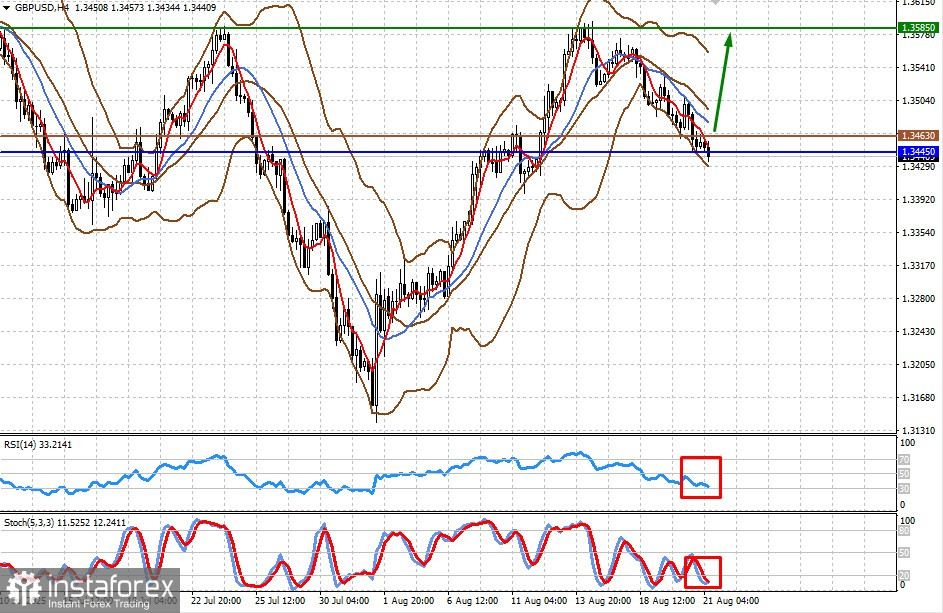

The pair is trading below 1.3445. If Powell signals a shift in monetary policy from hawkish to dovish, demand for risk assets should increase, putting further pressure on the dollar. In this case, the pair could climb toward 1.3585. A buying level could be set at 1.3463.