یہ بھی دیکھیں

17.06.2025 10:45 AM

17.06.2025 10:45 AM

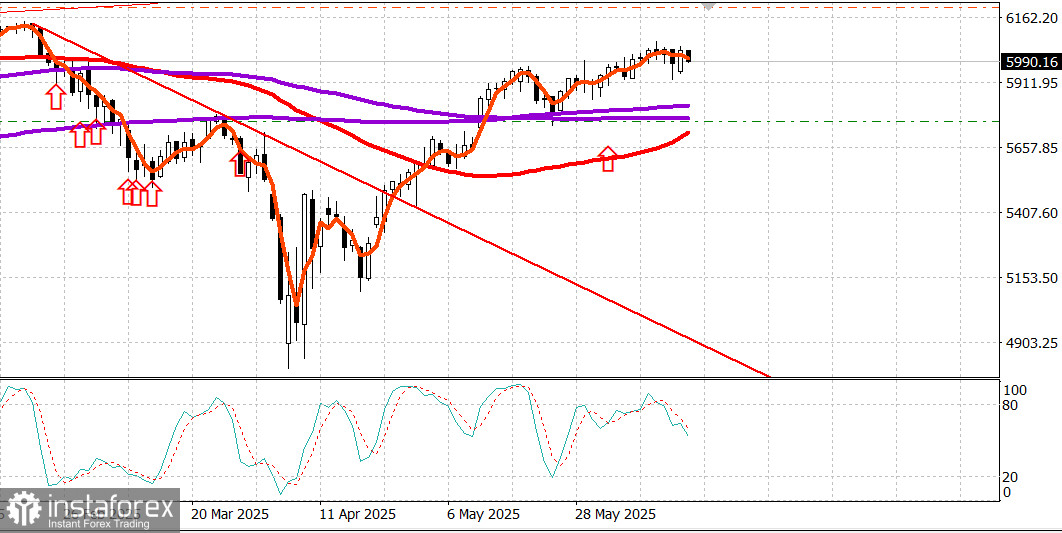

S&P500

Snapshot of major US stock indices on Monday: Dow +0.8%, NASDAQ +1.5%, S&P 500 +0.9%, S&P 500 at 6,033 in an intraday range of 5,600 to 6,200.

On Monday, the US stock market regrouped and recovered much of the losses sustained on Friday, buoyed by the understanding that the Israel-Iran conflict remains relatively contained and has not yet led to any significant disruptions in oil supplies. Reports suggested that Iran is engaging in diplomatic efforts to negotiate a potential ceasefire with Israel, although Israel has not expressed any such initiatives.

Despite this uncertainty, market sentiment was broadly positive, with the strongest momentum at the open, which pushed the S&P 500 as high as 6,050. However, buyers struggled to sustain that early confidence. The benchmark stock indices gradually retreated from these initial highs until the end of the session, but still closed comfortably above their opening levels.

The rally was supported by strong performance from large-cap stocks, which led gains in the information technology (+1.5%), communication services (+1.5%), and consumer discretionary (+1.2%) sectors.

The Vanguard Mega-Cap Growth ETF (MGK) rose 1.3%, outperforming the S&P 500's 0.9% gain.

Semiconductor stocks delivered standout performances, led by Advanced Micro Devices (AMD 126.40, +10.24, +8.82%), which surged following a CNBC report that the company may have secured a GPU deal with Amazon (AMZN 216.17, +4.07, +1.92%). The Philadelphia Semiconductor Index climbed 3.0%, bringing its quarterly gain to 23.3%.

On the downside, defense and energy stocks, which led on Friday amid geopolitical concerns, pulled back as fears over the Israel-Iran conflict ebbed away. The S&P 500 energy sector (-0.3%) traded lower alongside a decline in WTI crude futures (71.83, -1.33, -1.8%). Relative weakness was also observed in defensive sectors such as utilities (-0.5%), healthcare (-0.4%), and consumer basics (+0.02%).

Market breadth favored advancers over decliners by less than 2-to-1 on both the NYSE and Nasdaq, with this advantage narrowing as the session progressed.

Year-to-date performance:

Economic calendar The Empire State Manufacturing Survey for June was weaker than expected. The PMI plunged at -16.0 (consensus -6.6; previous -9.2), with declines in both new orders and shipments indices. This marked the fourth consecutive monthly contraction in New York State manufacturing activity; however, firms reported a more optimistic outlook for business conditions over the next six months.

Energy market Brent crude held at $74.40 as of Monday. Oil prices remain stable despite the ongoing Israel-Iran conflict for now, as Israel has not launched any major strikes against Iran's key oil infrastructure. However, this could change quickly.

Conclusion: The situation in Iran remains highly unstable and is likely to shift dramatically in the near term — either toward negotiations and some form of ceasefire or toward a collapse of authority in Iran, potentially leading to chaos.

The US stock market remains focused on the Federal Reserve's policy meeting but will react strongly to any major developments in the Middle East conflict.