Vea también

28.07.2025 09:56 AM

28.07.2025 09:56 AMThe annual inflation rate in Tokyo declined from 3.1% in June to 2.9% in July. The core index, excluding food and energy prices, also slowed from 3.1% to 2.9% year-over-year. Although inflation remains well above the Bank of Japan's target, the likelihood of a rate hike by the BoJ has decreased—if the Bank did not act earlier, why would it do so now, with inflation slightly slowing?

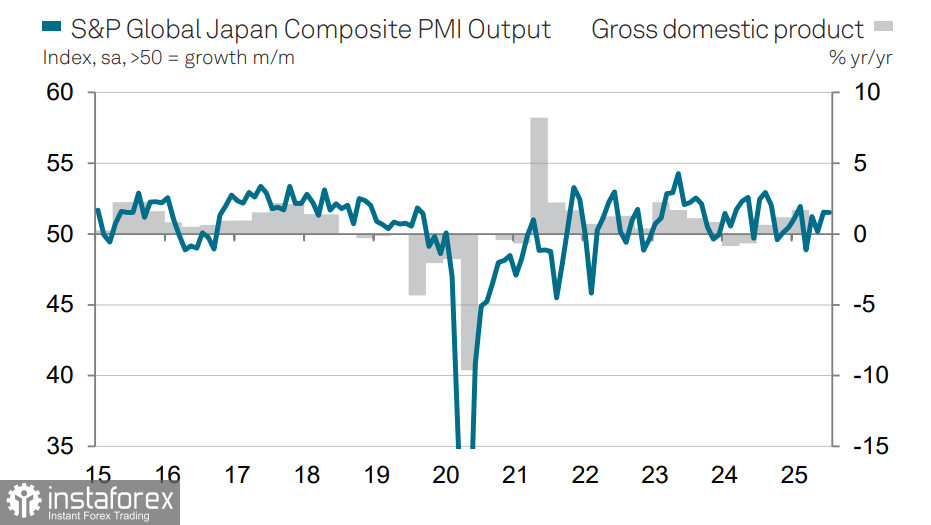

The next Bank of Japan meeting is scheduled for this week and will include the release of a quarterly forecast report. Mizuho Bank believes that despite the introduction of tariffs, the BoJ is likely to maintain its view that the economy and prices are "on the right track." The Bank is expected to revise its inflation forecast for the current year upward, but likely alongside a higher GDP projection, which would justify staying the course. Supporting the GDP outlook is the performance of the PMI: despite some weakness in the manufacturing sector, activity in services has increased significantly, reflecting continued strong consumer demand.

The Tokyo inflation data was published after the announcement of a large-scale trade agreement between Japan and the U.S., and the Bank will clearly need time to assess the effects of the 15% tariff on Japanese goods—its impact on corporate profits, the labor market, and the broader economy. BoJ Deputy Governor Uchida stated on Wednesday that real interest rates remain too low and that the Bank "will continue to raise interest rates." According to Uchida, overall developments are in line with the Bank's forecasts.

The consensus is that the rate will not be raised at next week's meeting and will remain at 0.5%, which would be a bearish signal for the yen. Market pricing suggests around an 80% probability of a rate hike before the end of the year, but this has long been priced in. As a result, the market reaction will likely manifest in a further weakening of the yen and an upward move in USD/JPY.

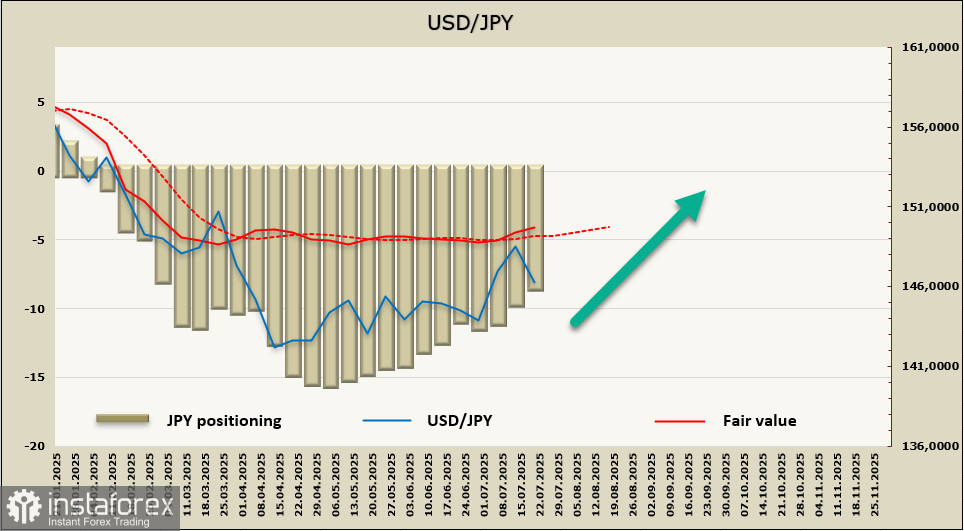

The net long position on the yen continues to shrink rapidly, down by 1.209 billion over the past reporting week, with the total bullish bias falling to 8.7 billion. The estimated fair value has finally broken away from the long-term average and is moving higher.

The probability of a downward move in USD/JPY continues to decrease, and even the persistence of core inflation—which would normally call for a policy response from the Bank of Japan—is not affecting market sentiment. We expect the yen to continue weakening, with a gradual move toward the 151.20–151.40 range.