Vea también

26.09.2025 12:01 PM

26.09.2025 12:01 PMAs of yesterday's close, major US stock indices ended lower. The S&P 500 fell by 0.50%, while the Nasdaq 100 lost 0.50%. The industrial Dow Jones retreated by 0.38%.

Global equities continue to slide for the fourth straight day, as concerns over high valuations and mixed signals from Federal Reserve officials regarding interest rates have dampened investor sentiment. Traders are digesting the latest economic data and Fed commentary as they try to gauge the future course of monetary policy. Uncertainty is mounting due to diverging opinions within the Fed about the timing and scope of future rate cuts. Some officials emphasize the importance of further data analysis before making decisions, while others hint at the possibility of more rapid policy easing.

The MSCI All Country World index declined by 0.1%, marking its longest losing streak in a month. Asian indices dropped by 0.8%, the sharpest fall in September. Shares of pharmaceutical companies plunged after President Donald Trump announced a 100% tax on branded or patented pharmaceuticals. The S&P 500 futures were little changed, while Nasdaq 100 futures fell by 0.1%. European contracts rose by 0.4%. The dollar index held near a three-week high, and Treasury yields traded in a narrow range, focusing investors' attention on the Fed's preferred inflation measure, which is due out today.

After a $15 trillion rebound in global equities from the April lows, traders are now faced with a wall of uncertainty as renewed tariff headlines again unsettle markets. Upcoming Fed actions, corporate earnings season, and the threat of a US government shutdown are also weighing on sentiment. Focus now shifts to Friday's inflation report after strong US GDP data have complicated the outlook for further rate cuts.

Curerncy markets have slightly pared back expectations for Fed rate cuts following the GDP release, now projecting a decrease of around 40 basis points by year-end. Disagreements within the Fed about rate dynamics are adding to the uncertainty.

Fed Governor Steven Miran stated yesterday that the US central bank risks harming the economy if it fails to act quickly to cut interest rates. He disagreed with last week's decision to cut by a quarter percentage point, favoring a half-point reduction.

His colleague Michelle Bowman also said yesterday that inflation is sufficiently close to the central bank's target, justifying further easing as the labor market weakens. Meanwhile, Chicago Federal Reserve President Austan Goolsbee voiced ongoing concerns about tariff-driven inflation and dismissed any calls for "front-loading" or multiple rate cuts.

In other markets, oil posted its largest weekly gain in over three months amid renewed Trump pressure on buyers of Russian energy. Gold traded just below its all-time high, marking a sixth week of gains.

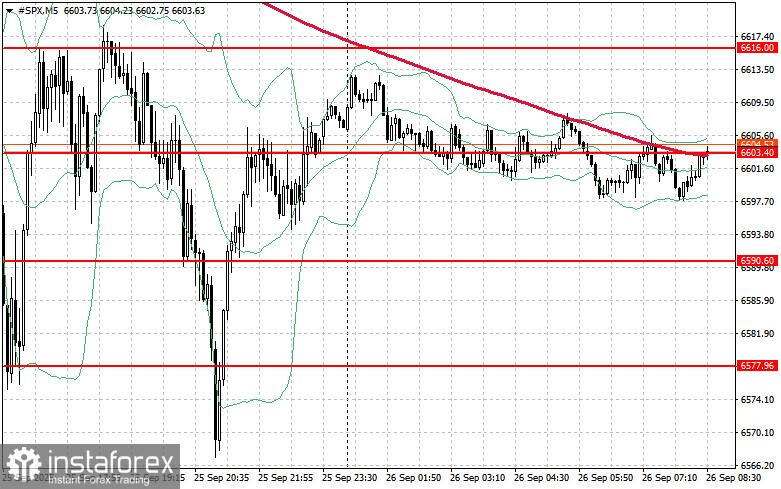

Technical outlook for S&P 500:

Today, the main objective for buyers will be to break through the nearest resistance at $6,616. This would pave the way for further growth and a possible move to $6,630. Additionally, holding above $6,648 would help strengthen the bulls' position. On the downside, if risk appetite decreases, buyers must defend the $6,603 level. A break below would quickly push the instrument down to $6,590 and open the path to $6,577.