আরও দেখুন

13.05.2025 12:24 AM

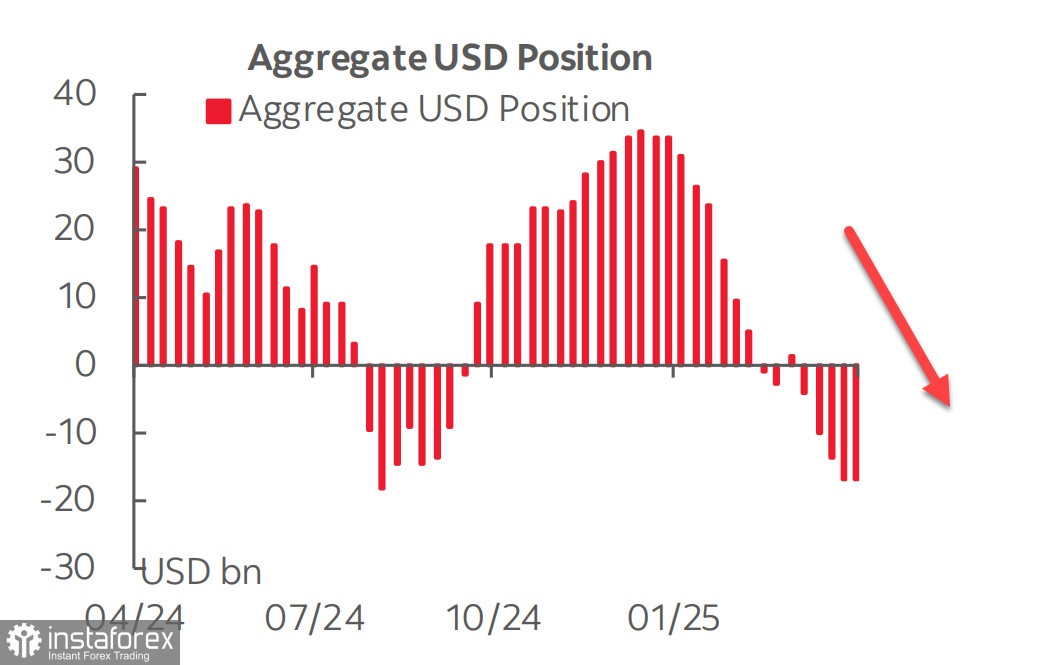

13.05.2025 12:24 AMThe CFTC report released on Friday showed minimal changes in overall currency positioning, with the net USD position against major currencies decreasing by a symbolic $0.1 billion to—$17.2 billion. Due to high overall uncertainty, investors remain in a wait-and-see mode, and the market is currently in a fragile balance awaiting new data.

The futures market anticipates three Federal Reserve rate cuts this year, with only minor adjustments. A slight increase in inflation expectations followed the release of secondary labor market data—unit labor costs rose by 5.7% in Q1, significantly above the previous 2% and the forecast of 5.3%. This led to an uptick in yields on 5-year TIPS (Treasury Inflation-Protected Securities).

The April consumer inflation report will be published on Tuesday. Forecasts are neutral, with headline and core readings expected to remain at the previous month's levels. However, this outlook carries considerable uncertainty, as the U.S. is currently experiencing opposing economic forces that could push inflation higher or lower.

One key factor is the tariff negotiations with China. Chinese exporters have sharply reduced shipments to the U.S.—for now, inventories are sufficient, but time is running out. Without a mutually acceptable resolution, a surge in inflation is inevitable. Meanwhile, reports suggest the U.S. and China are close to reaching a tariff agreement. The two sides have agreed to a 90-day delay in implementing reciprocal tariffs, during which they aim to formulate a balanced solution.

Markets responded instantly to this positive development. On Monday, the dollar strengthened significantly, particularly against the yen as a safe-haven currency. The U.S. Dollar Index reached a one-month high but remains below the level seen before April 2.

In recent months, the dollar has faced intense pressure due to Trump's unilateral actions, which threatened the global financial system's stability. The recent wave of optimism supports risk assets, and the dollar could also benefit.

The threat of a U.S. recession appears to be on hold for now. Recent data has not raised concerns, and the Atlanta Fed's GDPNow model currently forecasts 2.3% GDP growth in Q2, easing fears of a poor Q1. At the same time, it should be noted that markets are reacting to the potential easing of political tensions, which has triggered a wave of euphoria. However, this optimism is still based purely on rumors and speculation.

The S&P 500 made an impressive leap on Monday. If it stays above 5780, this may require a reassessment of the short-term outlook.

In any case, near-term expectations of a stock market correction should be put aside, as demand for risk rises and will likely continue to grow, barring any unexpected developments. Trump is likely to continue pursuing his plan to revise tariffs, meaning that any delays or preliminary agreements with China do not resolve the core issues. Once the current wave of optimism fades, markets could resume their downward movement.