See also

02.05.2025 09:24 AM

02.05.2025 09:24 AMThe market is confident that tariffs won't materialize or that companies can pass them on to customers. The S&P 500's eight-day rally—its longest since August—strongly hints at this. So does the deeper decline in the price-to-earnings ratio compared to the price-to-sales ratio. Issuers have delivered strong financial results and intend to continue doing so despite import tariffs. But isn't there a bit too much optimism in the market?

Strong corporate earnings from giants like Microsoft and Meta Platforms fueled the S&P 500 rally. Moreover, China has finally expressed readiness to negotiate with the U.S. However, let's not be misled. Beijing plans to fight and sees dialogue as possible only on one condition: if Washington lifts the draconian 145% tariffs it imposed. The U.S. has no intention of doing so—access to the "big beautiful store," as Donald Trump calls the American market, comes at a price.

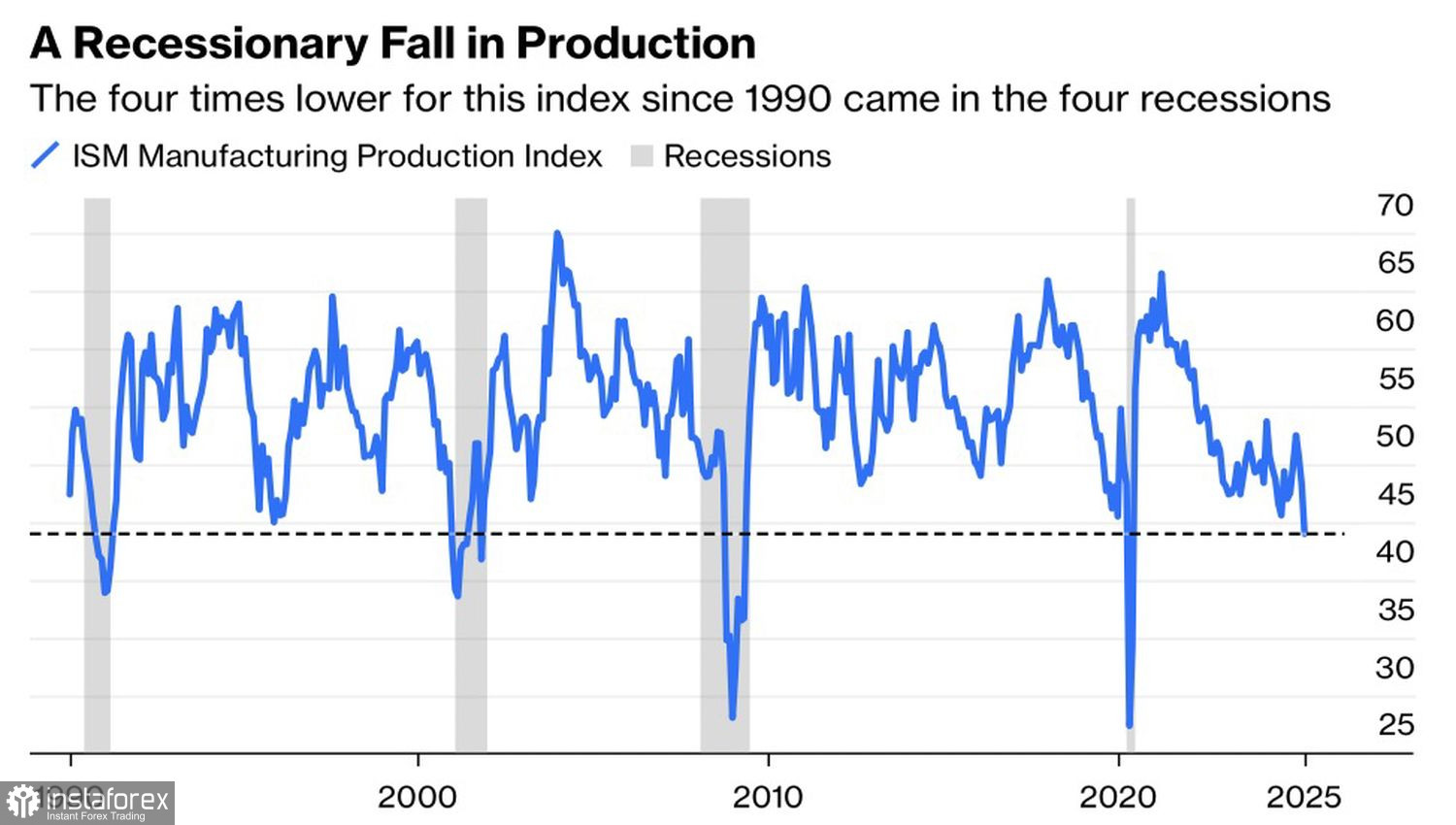

Equity investors seem to have forgotten about the risk of recession despite recent macroeconomic data pointing to a looming downturn in the U.S. economy. This includes the labor market, where job openings, ADP private employment, and jobless claims data have disappointed and raised red flags—as has business activity. Its decline in the manufacturing sector is especially alarming. During past recessions, the PMI fell to 40 and below.

S&P 500 bulls have another reason to worry: seasonality. The century-old tradition of "sell in May and go away" is again in play. According to Bespoke Investment Group, from 1993, the S&P 500 returned 171% from May to October versus 731% from November to April.

The stock market is entering turbulent waters. There is no clear sign of de-escalation in the U.S.-China trade conflict, a cooling U.S. economy is becoming more evident, and tensions between the White House and the Federal Reserve could flare up at any moment. Following Donald Trump, even the Treasury Secretary is now giving advice to Jerome Powell. Scott Bessent has called the Fed's attention to the bond market, which is signaling the need for at least three rate cuts in 2025.

The S&P 500 has long ignored macroeconomic data, preferring to listen to White House officials—but that can't last forever. Weak April nonfarm payrolls data could trigger a wave of selling in the U.S. stock market.

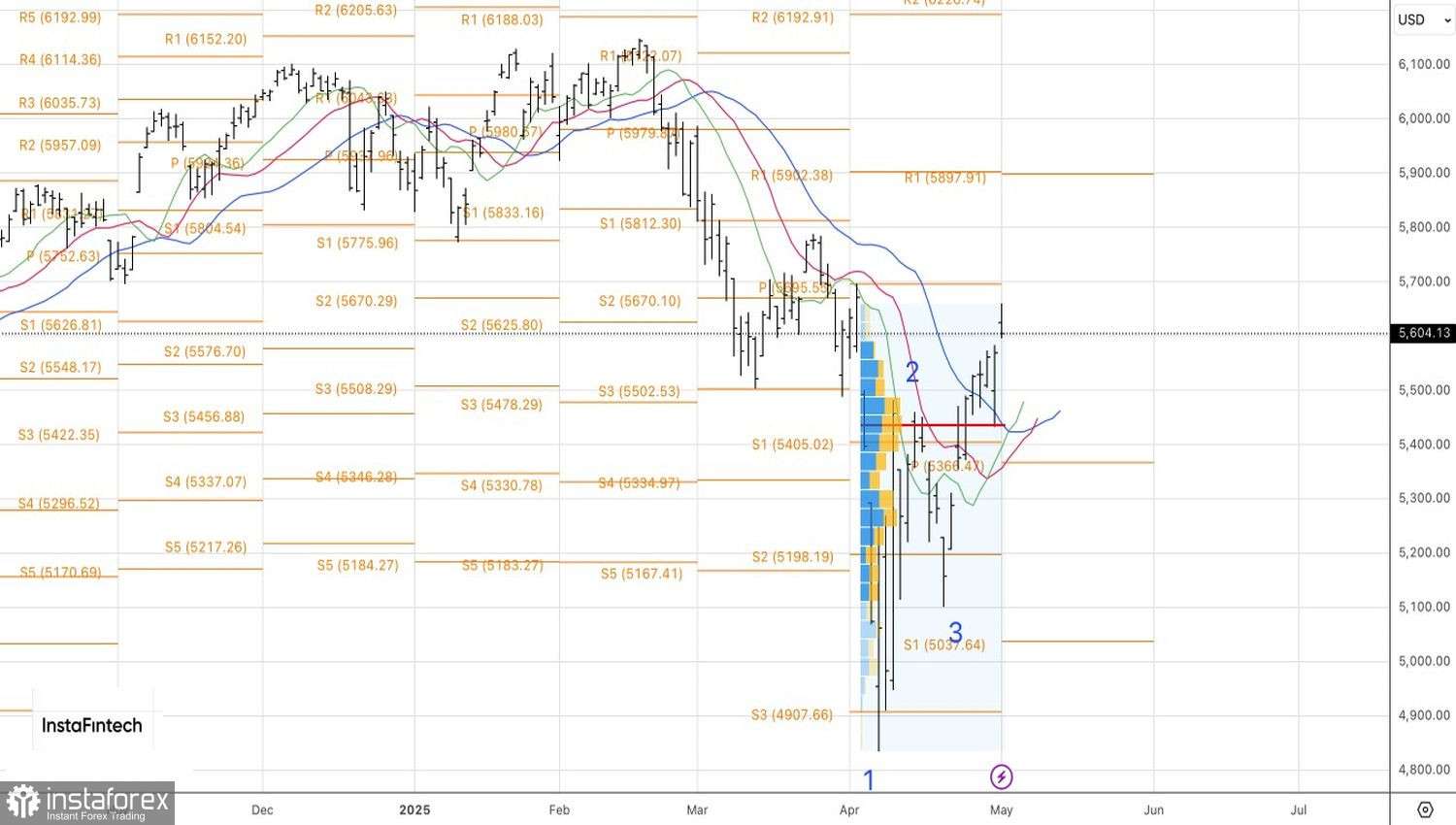

On the daily chart of the broad stock index, the resistance level at 5625 held up well. Those holding longs from 5400 could take profits or hedge their positions. Increasing short positions makes sense if the S&P 500 falls below 5515 and 5435.