See also

14.08.2025 10:47 AM

14.08.2025 10:47 AMThe market always finds a reason for optimism. At first, it was the de-escalation of trade conflicts, the so-called TACO effect, or Trump Always Chickens Out, the resilience of the US economy, and corporate earnings. Now, it is the anticipation of the Fed soon resuming its monetary easing cycle. July inflation data removed all concerns that the central bank might not cut interest rates in September. After Treasury Secretary Scott Bessent called for a 150-175 basis point reduction, the S&P 500 hit its all-time high for the 17th time in 2025.

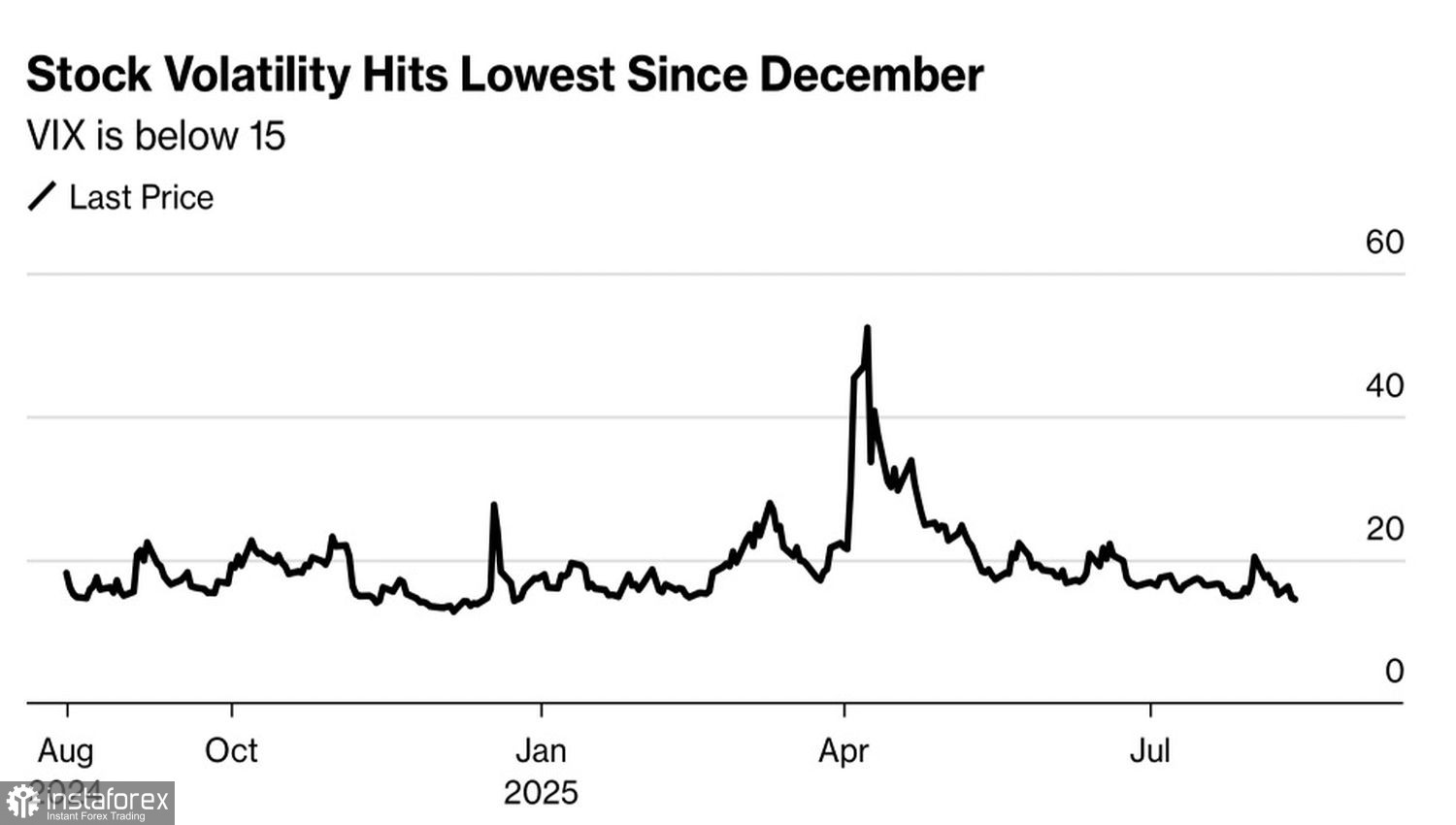

Markets have stopped reacting to trade-related news, such as the extension of current tariffs against China until October, or the increase in import duties on goods from India from 25% to 50% due to its purchases of Russian oil. Investors are confident that no significant changes are likely in the near term, that the US economy has proven resilient to tariffs, that the acceleration in inflation will be temporary, and that a recession will not occur. As a result, the S&P 500 continues to rise steadily, while equity market volatility declines.

US stock market volatility trends

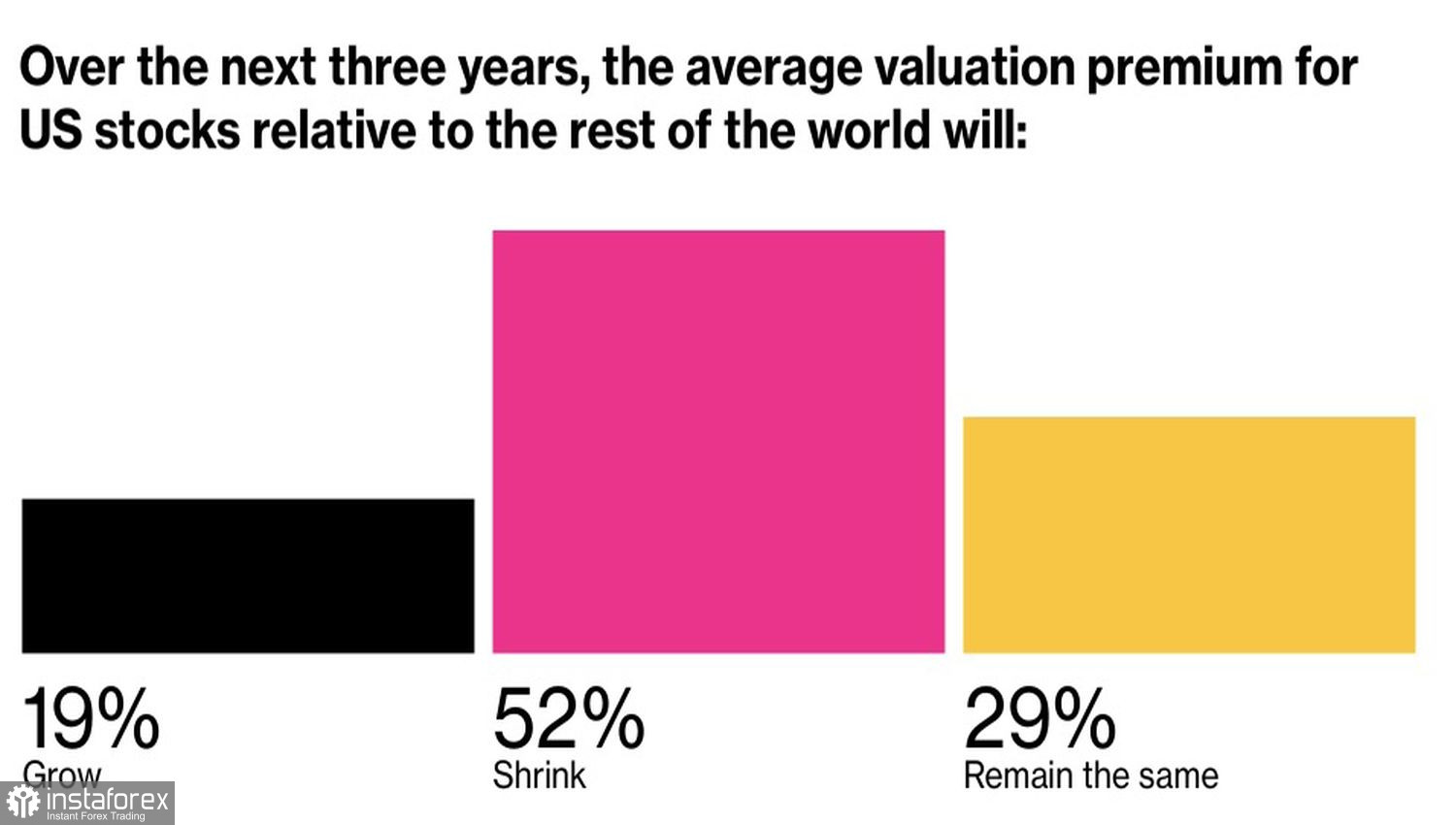

However, it is important to understand that the White House's protectionism will not manifest itself immediately — it takes time. According to 70% of investors surveyed by Bloomberg's MLIV Pulse, US equities will suffer from Donald Trump's tariffs by the end of his presidential term. At the same time, most believe that the valuation gap between US and European stocks will narrow.

Currently, the S&P 500 is trading at 22 times expected earnings, while the EuroStoxx 600 — at 15 times. Such a disparity encourages capital flows from the United States to Europe, putting pressure on the US dollar.

Forecasts for changes in US and European stock valuations

According to 52% of respondents, Europe could catch up with the United States in terms of valuations within three years only if the global economy slows down. The remaining 48% believe that this could happen against the backdrop of accelerating global GDP growth.

For now, however, the capital flow from the New World to the Old World does not particularly concern individual investors. They continue to buy the dips, putting major banks and investment firms in an awkward position. At the end of 2024, the consensus forecast expected the S&P 500 to rise by 13% to 6,614, but by May, this projection had dropped to just +2%. This marks the largest downward revision since the pandemic in 2020.

Only Wells Fargo and Morgan Stanley held on to their bullish views until the end; others shifted their forecasts and were left wrong-footed. The first bank pointed to the experience of Donald Trump's first presidential term, when he also backed down after threats. The second argued that other banks were changing their forecasts too quickly.

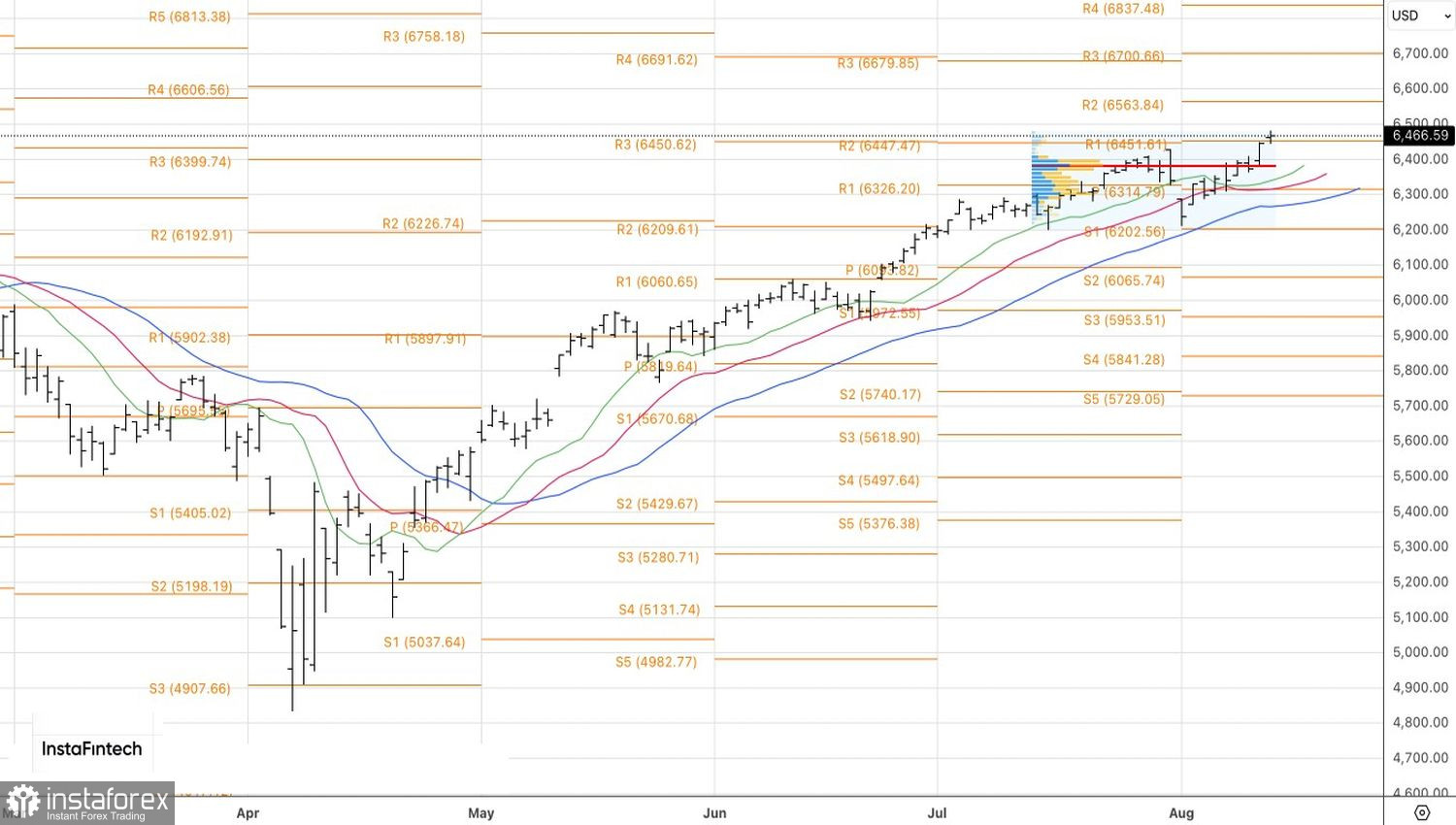

From a technical perspective, the daily chart of the S&P 500 shows a steady uptrend. Long positions opened on a breakout above 6,455 should be held. The next targets are seen at 6,565 and 6,675. Key support lies at the fair value level of 6,380.