یہ بھی دیکھیں

25.06.2025 11:52 AM

25.06.2025 11:52 AM

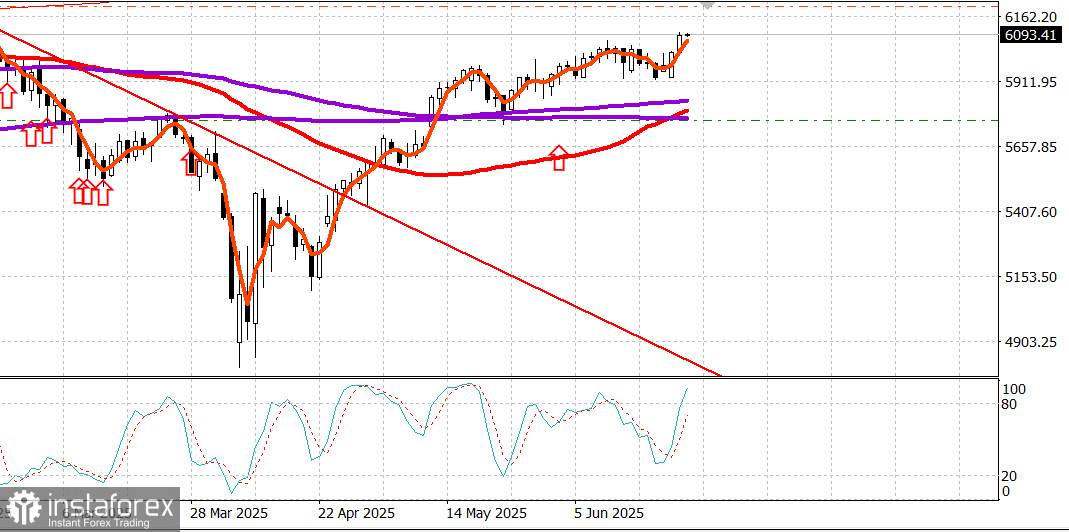

S&P500

Snapshot of the US major stock indexes on Tuesday: Dow +1.2%, NASDAQ +1.4%, S&P 500 +1.1% (closed at 6,092, within a 5,700–6,300 range).

The stock market traded with a positive bias throughout the session, supported by several catalysts:

WTI crude futures, which surpassed $78.00 per barrel on Monday, lost another 6.1% on Tuesday, closing at $64.46.

A decline in Treasury yields also aided the rally in equities, following a weaker-than-expected June Consumer Confidence report, which also showed a decline in 12-month inflation expectations.

The 2-year Treasury yield dropped 2 basis points to 3.81%. The 10-year yield fell 2 basis points to 4.30%.

An encouraging full-year outlook from cruise line operator Carnival (CCL 25.70, +1.66, +6.88%) also lifted investor sentiment.

Efforts continued in the Senate leadership to pass the reconciliation bill, aiming for the President's signature by July 4.

Separately, Fed Chairman Jerome Powell appeared before the House Financial Services Committee to deliver his semiannual monetary policy report. He expressed confidence that the tariff increases would likely drive prices higher this year and affect economic activity, while also showing openness to future policy shifts.

Powell acknowledged that multiple paths are possible — one being lower-than-expected inflation, which could justify earlier rate cuts. Though he had mentioned this possibility before, his measured tone and openness gave markets additional reassurance, especially following signs of de-escalation in the Iran-Israel conflict.

There was broad-based buying interest, lifting the S&P 500 to an intraday high of 6,101.76 shortly before the close.

Mega-cap and semiconductor stocks led the rally, but the bullish sentiment also showed in the outperformance of high-beta and small-cap stocks, often overlapping groups.

The Information Technology sector (+1.6%) set the pace, bolstered by strong gains in semiconductor components, including NVIDIA (NVDA 147.82, +3.65, +2.53%).

Other top-performing sectors included financials (+1.5%), communication services (+1.4%), and healthcare (+1.2%).

The Philadelphia Semiconductor Index rose 3.8%, now up 27.4% for the quarter.

The energy sector (-1.5%), which fell in line with oil prices, and Defensive Consumer Staples (-0.03%) were the only sectors to decline.

Advancers outpaced decliners by nearly 3-to-1 on the NYSE and more than 3-to-1 on the Nasdaq. Trading volume was above average on the NYSE and below average on the Nasdaq.

Year-to-date performance:

Economic calendar on Monday:

Q1 Current Account Deficit widened to $450.2B from a downwardly revised $312.0B (previous: -$303.9B).

FHFA House Price Index (April): -0.4% (consensus: 0.0%; previous revised to 0.0% from -0.1%).

S&P Case-Shiller House Price Index (April): +3.4% YoY (consensus: 4.1%; previous: 4.1%).

Conference Board Consumer Confidence (June): Fell to 93.0 (consensus: 99.0) from an upwardly revised 98.4 in May (previous: 98.0). A year ago, the index was at 97.8.

The key takeaway: consumers have become less optimistic about business conditions and job availability, potentially signaling weaker discretionary spending ahead.

Energy market Brent crude is now trading at $68.30 a barrel, having rebounded by almost $2 after steep losses on Monday and Tuesday.

Conclusion The market is overcoming anxiety after the Iran-Israel war tensions. It is poised to develop a bullish trend. We maintain already open positions, and consider new buys only after strong pullbacks.