یہ بھی دیکھیں

25.08.2025 01:32 PM

25.08.2025 01:32 PMFederal Reserve Chair Jerome Powell's testimony at the Jackson Hole Symposium was interpreted by the markets as dovish, with stock indices rising and the dollar declining across the forex market.

This perception was based on the Fed's confirmed shift in focus: instead of relying solely on inflation when making policy decisions, the central bank will now give equal attention to the labor market. Markets concluded that Powell thereby signaled an intent to cut interest rates in September, as the latest official ,employment report could hardly be described as anything but disappointing.

However, beneath the soft tone of Powell's speech lies a distinctly hawkish core. Markets overlooked fundamental changes in the Fed chair's rhetoric. Notably, Powell abandoned the framework of Flexible Average Inflation Targeting (FAIT), which allowed inflation to exceed the target for a period to compensate for lower averages over 3–5 years. In other words, if average inflation was low over the medium term but spiked temporarily, the Fed could previously refrain from intervening, smoothing out the average. Now, that limitation is gone, so the Fed will react significantly faster to a pickup in inflation.

In essence, if inflation rises by the end of the year—due to tariff changes, as many expect—the Fed may respond with a sudden rate hike, and any plans for rate cuts over the next year or two could become irrelevant. This is an explicit hawkish signal, and markets have yet to fully grasp its significance.

Let us also note the change in priorities regarding employment. Previously, we have often highlighted that the Fed faces two conflicting tasks: to curb rising inflation while simultaneously avoiding an economic downturn. Here, employment is the key criterion. Powell also indicated a stance change on this front, now putting inflation first and diminishing the importance of employment.

This signifies the Fed's willingness—plain and simple—to sacrifice the economy to support a stable dollar. It is possible that preserving the dollar's status as a global currency, against the backdrop of growing de-dollarization accelerated by new tariffs, is so crucial that the threat of recession is relegated to second place.

In our view, Powell's speech should be interpreted as clearly hawkish, not dovish. Over the long term, the Fed's policy will strengthen, not weaken, the dollar.

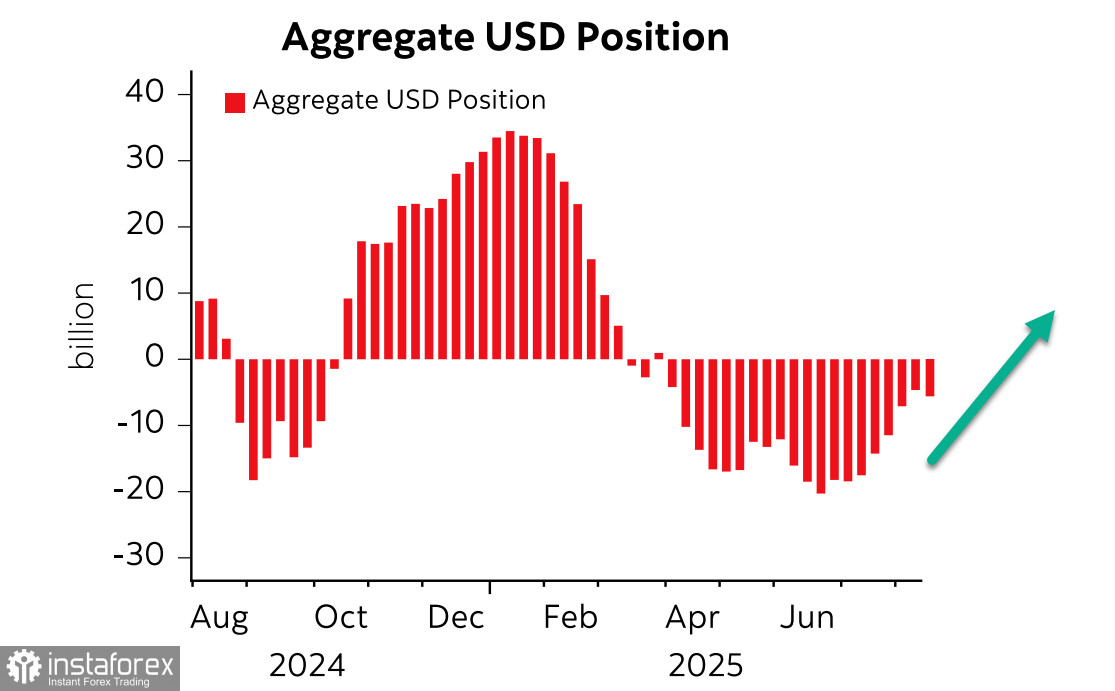

The latest CFTC report showed that after seven weeks of reducing net short positions on the dollar, speculators reversed some losses, with a weekly change of -$1.6 billion and a net bearish position of -$6.2 billion.

Nonetheless, we believe the trend for a stronger dollar remains. The dollar will react with gains across the currency spectrum as soon as the Fed's strategy becomes specific. On Monday morning, the probability of a Fed rate cut on September 17 stood at 87%, unchanged, but the likelihood of further cuts is in serious doubt. Importantly, forecasts for further rate reductions have barely shifted—certainly not toward a faster pace. For now, we must assume the Fed is prepared for two cuts, in September and December, and only if inflation does not accelerate while the labor market remains weak. In reality, stripped of emotion, Powell's speech was anything but dovish, and the market has yet to realize this.

We expect that the market will reevaluate this probability at the first signs of rising inflation. The Fed will not ignore these signals and is more likely to sacrifice the labor market and increase recession risks than compromise dollar stability. Accordingly, we believe the dollar will resume its rally even in the short term.

The S&P 500 index reacted to Powell's speech with a strong rally, but was unable to reach the 6,481 high. The market perceived the prospect of a weaker dollar, which would normally be expected to drive equity prices higher, but this reaction looks premature.

We dare to suggest that the reaction to Powell's initial messaging has already played out, and as the market comes to recognize that inflation—not the labor market—will be the Fed's true priority, we will see the opposite reaction: a strengthening dollar and falling equity indices. We anticipate that the S&P 500 has started a downward move, with a target of 6,180 now more likely than 6,840.