Veja também

12.08.2025 12:32 AM

12.08.2025 12:32 AMFollowing the release of the US employment report, the yen strengthened, and the Nikkei index fell by more than 900 points. Analysts at Mizuho note certain similarities with the strong risk-off episode that occurred exactly a year ago after the release of weak US employment data for July 2024. However, this comparison appears somewhat far-fetched — back then, USD/JPY collapsed from 160 to 140 in just a month, whereas the current reaction is much more moderate. The muted response is partly because after the disappointing report, secondary economic data were released, most of which suggested that nothing significant had happened and that the US economy was still growing.

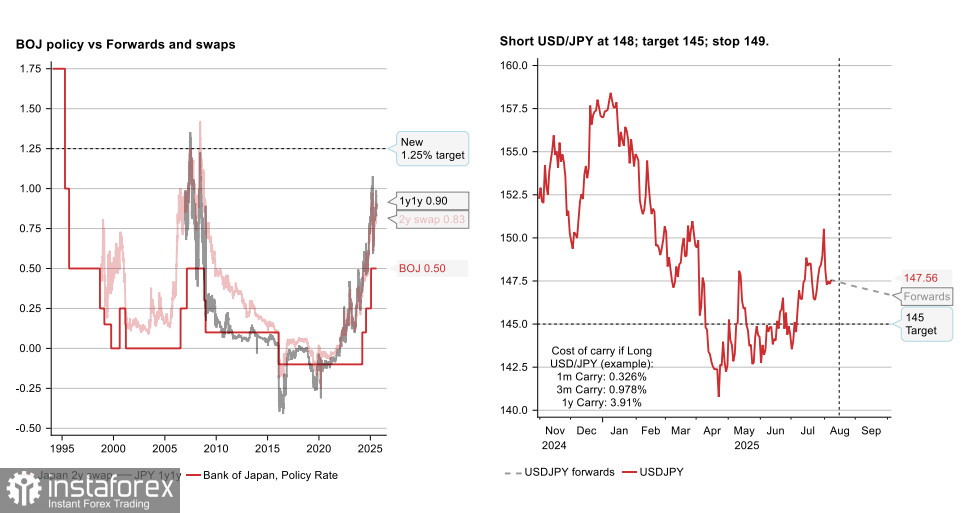

At present, Mizuho sees potential for two Bank of Japan rate hikes — one in October by 25 bps and another in January, bringing the rate to 1.0%, where it would remain for an indefinite period.

Mizuho also sees a fairly high probability of yen appreciation resuming, in particular expecting the currency to fall below 145 by the end of the year, with a move above 149 serving as the scenario cancellation level.

The Bank of Japan is taking a very cautious approach to rate adjustments. It is worth noting that markets have been expecting a hike since January — more than six months have passed, yet the situation remains highly uncertain. Japan is heavily dependent on external demand, primarily from the United States, and until there is complete clarity on that front, a rate increase will remain unlikely. In other words, the key question remains unchanged — will there be a recession in the US or not? The minutes of the July meeting directly refer to the state of the US economy, specifically highlighting rising uncertainty.

As for domestic factors, little has changed — inflationary pressures continue to trend higher, which provides grounds for another rate hike "in the coming months." This means the uncertainty level has not changed, as conditions for a rate hike could materialize either in September or December. Accordingly, the yen should not weaken too sharply, given the BOJ's shift toward a more hawkish stance, but there is also no strong basis for significant appreciation as long as uncertainty remains high.

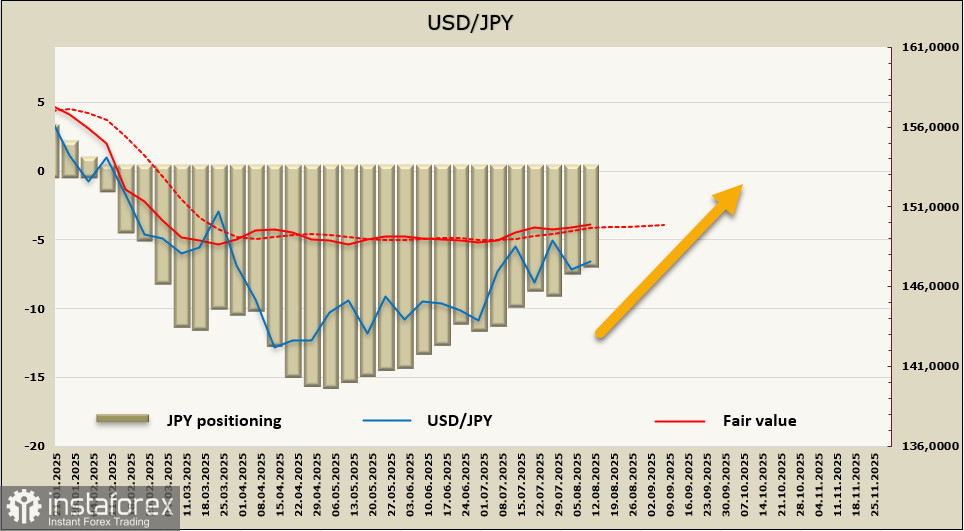

Net long positions in the yen decreased by 0.6 billion to 7.0 billion over the reporting week, marking the lowest level since January. The estimated price remains above the long-term average, but the momentum is weak.

The USD/JPY correction following the release of the disappointing US employment data was shallow — the yen did not reach the key support at 144.90/145.20 and is now forming a new upward impulse. We expect an attempt to once again test 151.20/40, with good chances of consolidating above it. A reversal of USD/JPY down toward 145 and lower is possible if demand for safe-haven assets increases, although this now appears less likely. In any case, after the Trump–Putin meeting on August 15, markets may experience a wave of euphoria and respond with a sharp increase in demand for risk assets.