See also

10.06.2025 06:45 PM

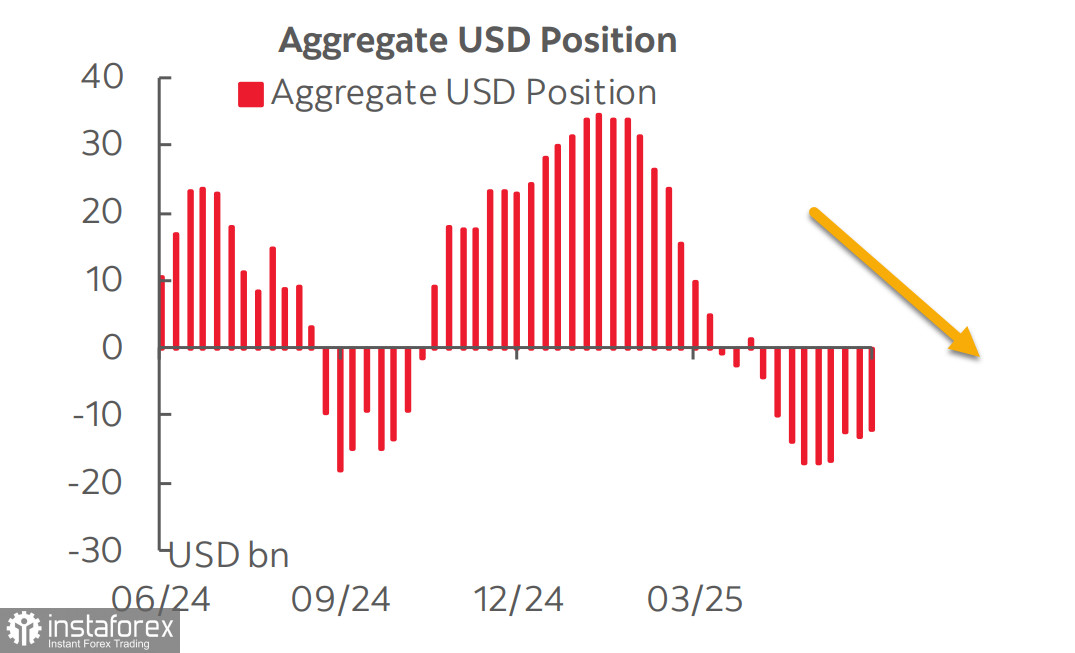

10.06.2025 06:45 PMThe latest CFTC report indicates that the sell-off of the U.S. dollar has either ended or is close to ending. The net short position against major currencies decreased by $1.094 billion over the reporting week, down to -$12.18 billion. While the bearish bias remains significant, this is the fifth consecutive week without an increase.

One of the main reasons behind the stabilization in dollar demand is the decline in expectations regarding Fed rate cuts. Just over a month ago, markets anticipated three rate cuts this year. Later, the third cut was postponed to January of next year, and now CME futures see the third cut only in March, with the earliest one pushed from July to September. The yield on 10-year U.S. Treasuries fell below 4% in April but has since rebounded and is now back in a range that has remained relatively stable for a year and a half. The market no longer sees a major risk of a weakening dollar, but it also hasn't decided whether the dollar has room to strengthen.

The U.S. economy is nearing recession, and the latest data tends to support that forecast. The ISM manufacturing index declined in May instead of the expected rise and is now in contraction territory, holding below the 50-point threshold. The services sector is showing a similar picture—rather than the expected rise to 52.2, the index fell to 49.9, signaling contraction. The jobs report, at first glance, appeared solid with 139,000 new jobs added (vs. 130,000 forecast), but downward revisions of 95,000 to the previous two months fully offset that positive surprise.

Of note is the continued wage growth, which is intensifying inflation expectations. The inflation report for May is due Wednesday, and forecasts call for an increase in both headline and core inflation—mainly due to the effects of Trump's tariff policy. Goods inflation is accelerating as the costs of high tariffs are being passed on to consumers. This process is just beginning but is already noticeable—alongside rising goods prices, there's a cooling in the services sector, which ultimately heightens rather than eases the risk of a recession.

Markets remain relatively stable at the start of the new week, awaiting concrete results from the resumed U.S.–China trade negotiations. Customs data showed that China's export growth slowed to a three-month low in May, as U.S. tariffs battered shipments, and factory deflation hit a two-year high. Chinese exports to the U.S. fell by 34.5% year-over-year in May—the steepest drop since February 2020, during the COVID-19 crisis. Until tangible negotiation outcomes emerge, markets will remain relatively calm without major price movements.

We don't currently see strong reasons for the U.S. dollar to resume growth against major world currencies, unless Fed rate expectations shift dramatically—resulting in a yield rebound. A potential U.S. recession might remind markets that the dollar is a safe-haven currency. But for now, with the U.S. economy shielded from global producers by trade barriers, the dollar is likely to struggle to regain upward momentum, even amid rising yields.

The S&P 500 index has finished its recent volatility—after plunging on the heels of Trump's first tariff war moves and quickly rebounding after the announcement of new talks, the index has nearly returned to early February levels. However, further growth remains highly uncertain.

If U.S.–China negotiations fail and new tariff escalations appear likely, the index may decline again, with losses exacerbated by continued signals of U.S. economic slowdown. In such a case, a drop toward 5500 would not be excessive. If, however, reason prevails and a resolution is found before the threat of recession becomes pronounced, the index could resume growth toward 6150. We maintain our view that downward movement is more probable, as the fundamental factors continue to favor a decline.